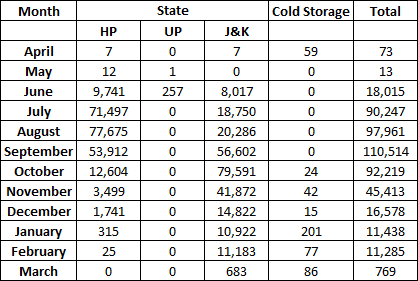

What was the maximum percentage of apples supplied by any state in any of the months?

Sign in

Please select an account to continue using cracku.in

↓ →

The following table gives the quantities of apples (in tonnes) arriving at New Delhi market from various states in a particular year. The month in which demand was more than supply, the additional demand was met by the stock from cold storage.

What was the maximum percentage of apples supplied by any state in any of the months?

This percentage is maximum in February in J&K; where the percentage is $$\frac{11183}{11285}=99.09$$%

Which state supplied the maximum number of apples?

From the table it is clear that the state which supplied the most number of apples is either HP or J&K.; UP and Cold Storage supplied less than a thousand apples in total.

The total number of apples supplied by HP is 231,028

The total number of apples supplied by J&K; is 262,735

Hence, the correct answer is J&K;

Which state supplied the highest percentage of apples from the total apples supplied?

The answer to this question is the same as the state which supplied the maximum number of apples.

We can rule out UP and Cold Storage as they supplied significantly less than the other two.

Among the other two states,

The total number of apples supplied by HP is 231,028

The total number of apples supplied by J&K; is 262,735

Hence, the correct answer is J&K;

In which of the following periods was the supply greater than or equal to the demand?

The supply is greater than or equal to demand if the cold storage number is zero.

This is the case between the months May-September.

Hence, the correct option is option (c)

If the yield per tree was 40 kg, then from how many trees were the apples supplied to New Delhi (in millions) during the year?

To calculate the number of trees required, let us calculate the total number of tonnes supplied.

The total number of tonnes supplied equals 494,525.

One tree supplies 40 kilograms.

Hence, the number of trees required is $$\frac{494525*1000}{40} \approx 12.5$$ million trees

Using the data in the earlier question, if there were 250 trees per hectare, then how many hectares of land was used?

In the earlier question, we determined that we needed 12.36 million trees per year.

Each hectare has 250 trees.

So, number of hectares of land used is $$\frac{12.36*1000000}{250} \approx 49450$$

Answer the questions based on the following information. The following bar chart gives the growth percentage in the number of households in the middle, upper-middle and high-income categories in the four regions for the period between 1987-88 and 1994-95.

(Number of households in thousands)

Which region showed the highest percentage growth in number of households in all the income categories for the period?

Percentage growth of all households South region showed the maximum increase in all households in the given period. (100% + 340%+ 425% = 865%)

What was the total household income in northern region for upper-middle class?

We don't know the number of households in the upper-middle income class for Northern region and hence can't calculate the total household income for the same.

What is the percentage increase in total number of households for the northern region (upper-middle class) over the given period?

The answer is provided by the bar chart.

Look at the graph named North and the bar colored Orange.

This shows the percentage increase in the upper middle class households from the year 1987-88 to 1994-95 and it equals 200%

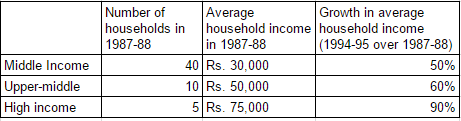

What was the average income of the high-income group in 1987-88?

The answer to this question is provided in the table.

The average income of middle income category is 30,000

The average income of upper-middle income category is 50,000 and

The average income of high income category is 75,000

Hence, the correct answer is 75,000

The ratio of total income for the high-income category to the upper-middle class increased by how much percentage in the given period (approximately) ?

Since we do not know the region-wise population of 1987-1988, we cannot find the increase in the number of households.

Hence, we cannot find the total income for the year 1995-96.

So the ratio cannot be determined.

The average income for the northern region in 1987-88 was

Since we do not know the distribution of households in each region, we cannot determine the average income.

Answer the questions based on the following information.

Krishna distributed 10-acre land to Gopal and Ram who paid him the total amount in the ratio 2 : 3. Gopal invested a further Rs. 2 lakh in the land and planted coconut and lemon trees in the ratio 5 : 1 on equal areas of land. There were a total of 100 lemon trees. The cost of one coconut was Rs. 5. The crop took 7 years to mature and when the crop was reaped in 1997, the total revenue generated was 25% of the total amount put in by Gopal and Ram together. The revenue generated from the coconut and lemon trees was in the ratio 3 : 2 and it was shared equally by Gopal and Ram as the initial amount spent by them were equal.

What was the total output of coconuts?

Let the amounts paid by Gopal and Ram to Krishna be 2X and 3X.

Gopal invested 2 lakhs additionally.

So, the total amount spent by him is 2X+2.

As the total amounts spent by the two of them are equal, it implies that 2X+2 = 3X or X = 2

Hence, the cost of the land is 2X+3X = 5X = 10 lakhs.

Total investment by the two of them is 10+2 = 12 lakhs

Hence, the total revenue generated is 12*25% = 3 lakhs.

The revenue generated by coconuts is $$3*\frac{3}{3+2} = 3*\frac{3}{5} = 1.8$$ lakhs

Cost of a coconut is Rs. 5

Hence, the total output of coconuts is $$\frac{180000}{5} = 36,000$$

What was the value of output per acre of lemon trees planted?

Let the amounts paid by Gopal and Ram to Krishna be 2X and 3X.

Gopal invested 2 lakhs additionally.

So, the total amount spent by him is 2X+2.

As the total amounts spent by the two of them are equal, it implies that 2X+2 = 3X or X = 2

Hence, the cost of the land is 2X+3X = 5X = 10 lakhs.

Total investment by the two of them is 10+2 = 12 lakhs

Hence, the total revenue generated is 12*25% = 3 lakhs.

The revenue generated by lemons is $$3*\frac{2}{3+2} = 3*\frac{2}{5} = 1.2$$ lakhs

Total land used to cultivate lemons is 5 acres.

So, revenue generated by the lemons per acre is $$\frac{1.2}{5} = 0.24$$ lakhs per acre

What was the amount received by Gopal in 1997?

Let the amounts paid by Gopal and Ram to Krishna be 2X and 3X.

Gopal invested 2 lakhs additionally.

So, the total amount spent by him is 2X+2.

As the total amounts spent by the two of them are equal, it implies that 2X+2 = 3X or X = 2

Hence, the cost of the land is 2X+3X = 5X = 10 lakhs.

Total investment by the two of them is 10+2 = 12 lakhs

Hence, the total revenue generated is 12*25% = 3 lakhs.

As the revenue is split equally, Gopal's share in the revenue is $$3*\frac{1}{2} = 1.5$$ lakhs

What was the value of output per tree for coconuts?

Let the amounts paid by Gopal and Ram to Krishna be 2X and 3X.

Gopal invested 2 lakhs additionally.

So, the total amount spent by him is 2X+2.

As the total amounts spent by the two of them are equal, it implies that 2X+2 = 3X or X = 2

Hence, the cost of the land is 2X+3X = 5X = 10 lakhs.

Total investment by the two of them is 10+2 = 12 lakhs

Hence, the total revenue generated is 12*25% = 3 lakhs.

The revenue generated by coconuts is $$3*\frac{3}{3+2} = 3*\frac{3}{5} = 1.8$$ lakhs

The number of coconut trees is 5 times the number of lemon trees = 100*5 = 500

So, the value of output per trees for coconuts is $$\frac{180000}{500} = 360$$

What was the ratio of yields per acre of land for coconuts and lemons (in terms of number of lemons and coconuts)?

We know the total revenue generated by coconuts and lemons respectively.

We also know the price of a coconut and can thus calculate the total number of coconuts produced per acre.

We don't know the price of a lemon and thus can't calculate the total number of lemons produced per acre.

So, the answer can't be determined.

Answer the questions based on the following information.

Ghosh Babu has a manufacturing unit. The following graph gives the cost for the various number of units. Given: Profit = Revenue - Variable cost - Fixed cost. The fixed cost remains constant up to 34 units after which additional investment is to be done in fixed assets. In any case, production cannot exceed 50 units.

Note: The fixed cost for upto 34 units is 50 and the the fixed cost for more is 100.

The revenue from 50 units is 1000 and the variable cost from 50 units is 700

What is the minimum number of units that need to be produced to make sure that there was no loss?

The revenue of 50 units is 1000. So, the revenue per unit is 20.

The variable cost of 50 units is 700. So, the variable cost per unit is 14.

Let the minimum number of units that are needed to be produced to ensure that there is no loss be X.

So, 20X > 14X + 50

Or X > 8

So, the least possible number of units to be produced is 9.

What is the least number of units that should be manufactured such that the profit was at least Rs. 50?

The revenue of 50 units is 1000. So, the revenue per unit is 20.

The variable cost of 50 units is 700. So, the variable cost per unit is 14.

Let the minimum number of units that are needed to be produced to ensure that there is a profit of at least 50.

So, total revenue is 20X and total cost is 14X+50.

So, Profit is 20X - (14X+50) = 6X-50 > 50

Hence, 6X > 100

Or X > 16

So, the least possible number of units to be produced is 17.

If at the most 40 units can be manufactured, then what is the number of units that can be manufactured to maximise profit per unit?

Till 34 units, the fixed cost is constant and the revenue increasing per every unit made.

So, to calculate the number of units that need to be produced to maximize the profit, we have to check only at two points: 34 units and 40 units.

The revenue of 50 units is 1000. So, the revenue per unit is 20.

The variable cost of 50 units is 700. So, the variable cost per unit is 14.

If number of units produced is 34,

Fixed cost is 50

Variable cost is 14*34 = 476

Revenue is 20*34 = 680.

So, profit is 680-476-50 = 154

If number of units produced is 40,

Fixed cost is 100

Variable cost is 14*40 = 560

Revenue is 20*40 = 800.

So, profit is 800-560-100 = 140

So, the profit is maximized when the number of units produced is 34

If the production cannot exceed 45 units, then what is the number of units that can maximise profit per unit?

Till 34 units, the fixed cost is constant and the revenue increasing per every unit made.

So, to calculate the number of units that need to be produced to maximize the profit, we have to check only at two points: 34 units and 45 units.

The revenue of 50 units is 1000. So, the revenue per unit is 20.

The variable cost of 50 units is 700. So, the variable cost per unit is 14.

If number of units produced is 34,

Fixed cost is 50

Variable cost is 14*34 = 476

Revenue is 20*34 = 680.

So, profit is 680-476-50 = 154

If number of units produced is 45,

Fixed cost is 100

Variable cost is 14*45 = 630

Revenue is 20*45 = 900.

So, profit is 900-630-100 = 170

So, the profit per unit is maximized when the number of units produced is 34

If the fixed cost of production goes up by Rs. 40, then what is the minimum number of units that need to be manufactured to make sure that there is no loss?

The revenue of 50 units is 1000. So, the revenue per unit is 20.

The variable cost of 50 units is 700. So, the variable cost per unit is 14.

As fixed cost went up by 40 units, the total fixed cost (when number of units is less than 34) is 50+40 = 90

Let the minimum number of units that are needed to be produced to ensure that there is no loss be X.

So, 20X $$\leq$$ 14X + 90

Or X $$\leq$$ 15

So, the least possible number of units to be produced to ensure no loss is 15.

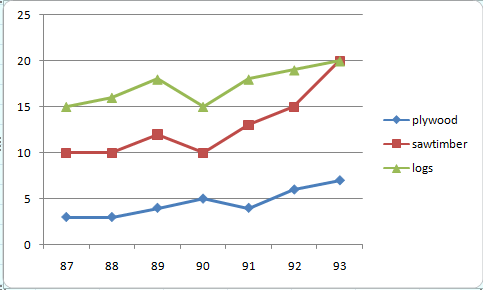

Answer the questions based on the following information. In the following chart, the price of logs shown is per cubic metre that of plywood and saw timber is per tonne.

What is the maximum percentage increase in price per cubic metre or per tonne over the previous year?

The maximum percentage increase in price of logs happened in the year 1991 (compared to 1990) and equaled 18/15 - 1 = 20%

The maximum percentage increase in price of plywood happened in the year 1992 (compared to 1991) and equaled 6/4 - 1 = 50%

The maximum percentage increase in price of sawtimber happened in the year 1993 (compared to 1992) and equaled 20/15 - 1 = 33.33%

Hence, the correct answer is 50%

Which product shows the maximum percentage increase in price over the period?

The percentage increase in price of logs over the period of time equals 20/15-1 = 33.33%

The percentage increase in price of plywood over the period of time equals 7/3 - 1 = 133.33%

The percentage increase in price of sawtimber over the period of time equals 200/100 - 1 = 100%

Hence, the maximum percentage increase in price over the period of time happened with plywood.

If the prices of sawtimber increased by 33.33%, in which year was the difference in prices of one tonne of saw timber and one cubic metre of logs the least?

After an increase by 33%, the difference in the prices of one tonne of saw timber and one cubic metre of logs is given below according to the respective years.

The difference in 1987 is 15 - 10*133.33% = 1.67

The difference in 1988 is 16 - 10*133.33% = 2.67

The difference in 1989 is 17.5 - 12*133.33% = 1.5

The difference in 1990 is 15 - 10*133.33% = 1.67

The difference in 1991 is 17.5 - 12.5*133.33% = 0.833

The difference in 1992 is 18 - 15*133.33% = -2

The difference in 1993 is 20 - 20*133.33% = -6.67

Hence, the difference is least in the year 1991.

If one cubic metre = 700 kg for plywood and 800 kg for saw timber, find in which year was the difference in the prices of plywood and saw timber (per cubic metre) the maximum?

From the above diagram, we can say that difference is highest in 1992.

If the volume sales of plywood, saw timber and logs were 40%, 30% and 30% respectively, then what was the average realisation in 1993 per cubic metre of sales? (Weight of one cubic metre of saw dust and plywood both = 800 kg)

In 1993, price of logs = Rs. 20 per cubic metre.

volume sales of plywood, saw timber and logs were 40%, 30% and 30%

In 1993, price of plywood = Rs. 7 per tonne

In 1993, price of plywood = Rs. 20 per tonne

Weight of one cubic metre of saw dust and plywood both = 800 kg

1 tonne=1000kg

Price of 1000kg of plywood= Rs 7

Price of 800kg( 1 m$$^3$$)= 7 x 0.8 = Rs 5.6 per cubic metre.

Price of saw timber = 20 x 0.8 = Rs 16 per cubic metre.

We know that the sales volume of plywood, saw timber and logs are in the ratio 4 : 3 : 3.

Thus, the average realization must be the weighted avg of these three-

$$\frac{(4\times 5.6)+(3 \times 16)+(3 \times 20)}{4+3+3}$$

=13.1

= Rs. 13 (Approximately)

In the previous question, if in 1994, prices increased by 5%, 1% and 10% while the volume sales break-up was 40%, 30% and 30% for plywood, saw timber and logs respectively, then what was the average realisation?

In this case the average realization will be-

$$\frac{(4\times 5.26 \times 1.05)+(3 \times 14.28 \times 1.01)+(3 \times 20 \times 1.1)}{4+3+3} \approx 13.15$$

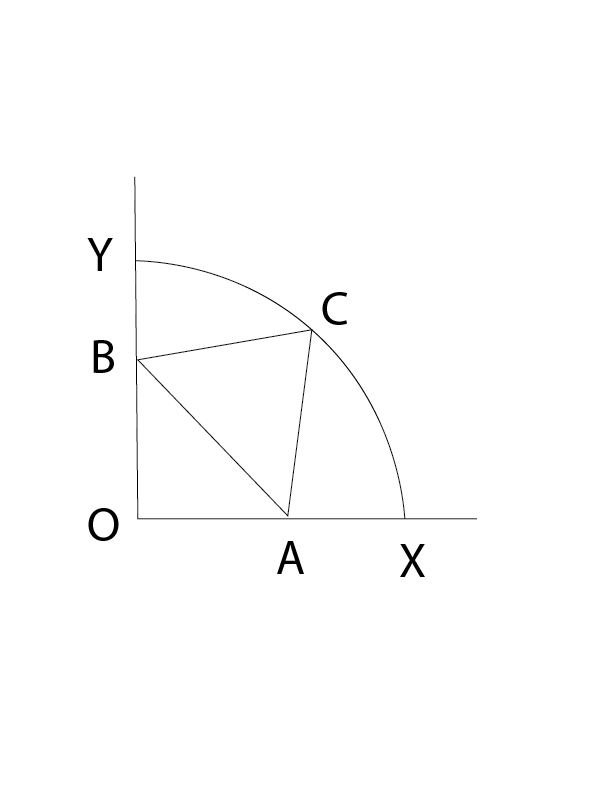

Find the length of AB if $$\angle YBC = \angle CAX = \angle YOX = 90$$.

I. Radius of the arc is given.

II. OA = 5

Only statement A: Angles OAC, ACB, CBO are right angles => OACB is a rectangle. OC = AB and OC is radius => AB is equal to radius. Hence, we can find the answer using statement A only.

Only statement B: The point B can change even though the point A s fixed at a distance of 5 units on x-axis from origin. Hence, length of AB changes => We cannot find the answer using statement B only.

Is n odd?

I. n is divisible by 3, 5, 7 and 9.

II. 0 < n < 400

Let's consider the statements one by one.

Statement 1: n is a multiple of HCF(3,5,7,9) = 315. Hence, n can be 315, 630, 945 .... Hence we cannot say if n is odd or even.

Statement 2: 0<n<400, we cannot say if n is odd or even.

Taking both statements together, n=315. Hence, it is odd.

Thus the question can be answered using both statements together.

Find $$2 \circledast 3$$, where $$2\circledast 3$$ need not be equal to $$3\circledast2$$

I. $$1 \circledast 2$$=3

II. $$a \circledast b=\frac{a+b}{a}$$, where a and b are positive.

The definition of the given function is expressed in statement 2, where $$a \circledast b=\frac{a+b}{a}$$

Hence $$2\circledast3=\frac{2+3}{2}$$.

Hence the answer can be determined by b alone. A does not give any releant information.

Radha and Rani appeared in an examination. What was the total number of questions?

I. Radha and Rani together solved 20% of the paper.

II. Radha alone solved 5/3 rd of the paper solved by Rani.

Let the total questions be x and the questions solved by Radha and Rani be y and z respectively.

According to the first statement, y+z = 20% of x

Accoding to the second statement, y = 5/3rd of z

There are 2 equations and three variables. Hence the solution cannot be determined.

What is the price of tea?

I. Price of coffee is Rs. 5 more than that of tea.

II. Price of coffee was Rs. 5 less than the price of a cold drink which cost three times the price of tea.

Let price of tea be t, coffee be c and cold drink be d.

Statement 1: c=t+5, we cannot infer value of t from this information

Statement 2: c=d-5 and d=3t, we cannot infer the value of t from this information

Using the statements together, c=t+5 and c=3t-5.

=>t+5=3t-5

=>2t=10

=> t=5

Hence, we can answer the questions using both statements together.

What is the value of ‘a’?

I. Ratio of a and b is 3 : 5, where b is positive.

II. Ratio of 2a and b is 10 12 , where a is positive.

We cannot uniquely determine a value for a using either statement alone.

Using both statements together, we get an inconsistent set of equations. Hence, there is no solution using both statements together.

Thus, the question cannot be answered using both statements together.

In a group of 150 students, find the number of girls.

I. Each girl was given 50 paise, while each boy was given 25 paise to purchase goods totaling Rs. 49.

II. Girls and boys were given 30 paise each to buy goods totalling Rs. 45.

Let the number of girls be g and boys be b. Hence, b+g=150

Statement 1: 50g+25b=4900 => 2g+b=196. Solving the two equations, g=46. Hence, answer can be obtained using statement 1 alone.

Statement 2: 30b+30g=4500 => b+g=150. As both the equations are equal, we cannot find a unique solution.

Thus, the question can be answered using one of the statements alone and not the other.

There are four envelopes — E1, E2, E3 and E4 — in which one was supposed to put letters L1, L2, L3 and L4 meant for persons C1, C2, C3 and C4 respectively, but by mistake the letters got jumbled up and went in wrong envelopes. Now if C2 is allowed to open an envelope at random, then how will he identify the envelope containing the letter for him?

I. L2 has been put in E1.

II. The letter belonging to C3 has gone in the correct envelope.

From the statements we need to infer which envelope contains L2.

From statement 1, we know that C2 should open E1.

From statement 2, we cannot tell which envelope contains L2.

Hence, the question can be answered using one of the statements alone and not the other.

There are four racks numbered 1, 2, 3, 4 and four books numbered 1, 2, 3, 4. If an even rack has to contain an odd-numbered book and an odd rack contains an even-numbered book, then what is the position of book 4?

I. Second book has been put in third rack.

II. Third book has been put in second rack.

Let's take the two statements individually:

Statement 1: If the second book is in Rack 3, then the fourth book must be in the only remaining odd numbered rack i.e. rack 1. Hence, we can infer the position of book 4 using the first statement.

Statement 2: If the third book is in Rack 2, then the first book must be in Rack 4. However, we don't know anything about the position of Book 4. Hence, we cannot infer the position of book 4 using the second statement.

Hence, the question can be answered using one of the statements but not the other.

Find the value of X in terms of ‘a’.

I. Arithmetic mean of X and Y is ’a’ while the geometric mean is also ‘a’.

II. Y X = R; X - Y = D.

Statement 1: a = (X+Y)/2 and $$a^2 = XY$$. Hence, $$a=(X+a^2/X)/2$$. Hence, we can re-arrange the equation to represent X in terms of a

Statement 2: There is no relation given between X and a. Hence, we cannot find value of X in terms of a.

Hence, the question can be answered by one statement alone and not the other.

There are two concentric circles C1 and C2 with radii r1 and r2. The circles are such that C1 fully encloses C2. Then what is the radius of C1?

I. The difference of their circumference is k cm.

II. The difference of their areas is m sq. cm.

We know that r1>r2.

Statement 1: $$2\pi(r1-r2) $$ = k. We cannot determine r1 from this information

Statement 2: $$\pi(r1^2-r2^2)$$ = m. We cannot determine r1 from this information.

Using both statements together, (r1+r2)/2 = m/k. We now have two linear equations with two variables. Hence, we can determine the value of r1 in terms of m and k.

Hence, the answer can be found using both statements together.

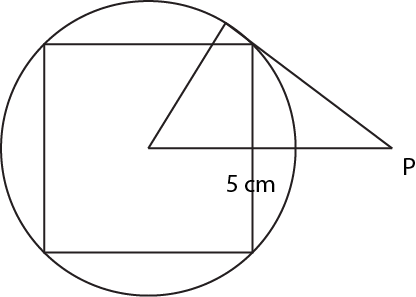

A circle circumscribes a square. What is the area of the square?

I. Radius of the circle is given.

II. Length of the tangent from a point 5 cm away from the centre of the circle is given.

As the circle circumscribes the square, diameter of the circle= diagonal of the square. Let the side of the circle be s. If we can determine the value of s, then we can find the area of the square $$s^2$$.

Statement 1: Let the radius be r. 2r = $$s \sqrt{2}$$. Hence, s = $$r\sqrt{2}$$. Thus, we can find the area of the circle using this information.

Statement 2: This scenario can be drawn as shown below:

A line drawn from the center of the circle intersects the tangent at an angle of 90°. Hence, the triangle formed is a right-angled triangle with the hypotenuse of 5 cm, one side equal to the radius of the circle and second side equal to the length of the tangent. If the length of the tangent is known then we can calculate the radius using Pythogoras theorem. If the radius is known, the area of the square can be calculated as shown above.

A company has a job to prepare certain number cans and there are three machines A, B and C for this job. A can complete the job in 3 days, B can complete the job in 4 days, and C can complete the job in 6 days. How many days will the company take to complete the job if all the machines are used simultaneously?

If they work together, then total work done in single day = $$\frac{1}{3} + \frac{1}{4} + \frac{1}{6} = \frac{9}{12}$$

So $$\frac{9}{12}$$ work is done in 1 day

Hence unit work will be done in $$\frac{12}{9}$$ or $$\frac{4}{3}$$ days.

$$n^3$$ is odd. Which of the following statement(s) is/are true?

I. $$n$$ is odd.

II.$$n^2$$ is odd.

III.$$n^2$$ is even.

if $$n^3$$ is odd then $$n$$ will be odd. let's say it is $$2k+1$$

then $$n^2$$ will be = $$(4k^2 + 4k + 1)$$ which will be odd

Hence answer will be C.

Answer the questions based on the following information. Production pattern for number of units (in cubic feet) per day.

The finished goods are to be transported to the market by a truck having a capacity of 2000 cubic feet. Any finished goods (ready at the end of the day) retained overnight at the factory will incur a storage cost of Rs 5 per cubic foot for each night of storage. The hiring cost for the truck is Rs 1000 per day.

If all the units should be sent to the market, then on which days should the trucks be hired to minimize the cost?

The truck should be sent on a day on which maximum number of units can be sent. It happens on 2nd, 4th, 5th and 7th day. Hence the answer is b.

If the storage cost is reduced to Re 0.80 per cubic feet per day, then on which day(s), should the truck be hired?

If the truck is hired only for the 7th day, the cost will be (150*6 + 180*5 + 120*4 + 250*3 + 160*2 + 120)*0.8 = 2776

So, total cost incurred = 2776 + 1000 = 3776

If a truck is hired on 4th day and 7th day, the cost incurred will be (150*3 + 180*2 + 120)*0.8 + 1000 + (160*2 + 120)*0.8 + 1000 = 3096

So, a truck should be hired on the 4th and 7th day.

One bacterium splits into eight bacteria of the next generation. But due to environmental condition only 50% survives and remaining 50% dies. If the seventh generation number is 4,096 million, what is the number in first generation?

let's say x is the initial number of bacterias :

So in 2nd generation no. of bacterias = $$\frac{8x}{2} = 4x$$

In 3rd generation, it will be = 16x

4th gen. = 64x

5th gen. = 256x

6th gen. = 1024x

7th gen. = 4096x

Hence x = 1 million

Three circles, each of radius 20, have centres at P, Q and R. Further, AB = 5, CD = 10 and EF = 12. What is the perimeter of ΔPQR ?

As radius of circle is 20, lengths of PR, QR and PQ will be (15+5+15) , (10+10+10) , (8+12+8) respectively.

So perimeter will be = 28 + 30 + 35 = 93

Answer the questions based on the following information. The following operations are defined for real numbers.

a # b=a + b, if a and b both are positive else a # b=1

a $$\triangledown$$ b=$$(a \times b)^{a+b}$$ if $$a\times\ b$$ is positive else a $$\triangledown$$b=1.

$$\frac{(2\#1)}{(1 \triangledown 2)}$$ =

$$2\#1 = 2+1 = 3$$

$$1 \triangledown 2 = (1 \times 2)^(1+2) = 2^3$$

So answer will be $$\frac{3}{8}$$

$$\frac{((1\#1) \# 2) - (10^{1.3} \triangledown \log_{10}{0.1})}{1 \triangledown 2}$$

$$((1\#1) \# 2) = 2 \# 2 = 4$$

$$\log_{10} 0.1$$ = $$\log_{10} 10^{-1}$$ = -1

As $$(10^{1.3} \times -1)$$ is not positive, $$(10^{1.3} \triangledown \log_{10}{0.1})$$ = 1

$$1 \triangledown 2$$ = $$(1x2)^{(1+2)}$$ = $$2^3$$ = 8

Hence, the fraction is (4-1)/8 = 3/8

$$(BE)^2 = MPB$$, where B, E, M and P are distinct integers. Then M =

A digit number when squared produces a 3 digit number. This means that the number ranges from [10, 31].

First digit of $$BE^2$$ should be unit digit of $$E^2$$. But unit digit of $$E^2$$ is B. Look at the numbers and the unit digit of their square.

0-0, 1-1, 2-4, 3-9, 4-6, 5-5, 6-6, 7-9, 8-4, 9-1. Only 2-4, 3-9, 4-6, 7-9, 8-4 and 9-1 are kind of pairs we are looking after.But all the pairs except 9-1 produce a number greater than 31. Now, the number we can form from 9-1 is 19 whose square is 361 which satisfies all the condition we are looking for. This is the only such number.

Five-digit numbers are formed using only 0, 1, 2, 3, 4 exactly once. What is the difference between the maximum and minimum number that can be formed?

Maximum five digit number which can be formed by using numbers is 43210

And minimum five digit number = 10234

Difference = 43210 - 10234 = 32976

How many five digit numbers can be formed from 1, 2, 3, 4, 5, without repetition, when the digit at the unit’s place must be greater than that in the ten’s place?

Possible numbers with unit's place as 5 = $$4 \times 3 \times 2 \times 1 = 24$$

Possible numbers with unit's place as 4 and ten's place 3,2,1 = $$3 \times 3 \times 2 \times 1 = 18$$

Possible numbers with unit's place as 3 and ten's place 2,1 = $$2 \times 3 \times 2 \times 1 = 12$$

Possible numbers with unit's place as 3 and ten's place 1 = $$1 \times 3 \times 2 \times 1 = 6$$

Total possible values = 24+18+12+6 = 60

Distance between A and B is 72 km. Two men started walking from A and B at the same time towards each other. The person who started from A travelled uniformly with average speed of 4 km/hr. While the other man travelled with varying speed as follows: in the first hour his speed was 2 km/hr, in the second hour it was 2.5 km/hr, in the third hour it was 3 km/hr, and so on. When will they meet each other?

In the first hour, they cover 6km. In the second hour they cover 6.5km. In the third hour, they cover 7km and so on.

Finally, they cover 72km in 9 hours.

Distance covered by A in 9 hours = 4*9 = 36km

=> They meet mid-way between A and B.

P, Q, R and S are four statements. Relation between these statements is as follows.

I. If P is true, then Q must be true.

II. If Q is true, then R must be true.

III. If S is true, then either Q is false or R is false.

Which of the following must be true?

Options B,C and D are given vice-versa to given statements which is not necessarily true.

But according to option A, P is true, then Q and R will be true too but S will be false as for S, either Q or R should be false.

So answer will be A.

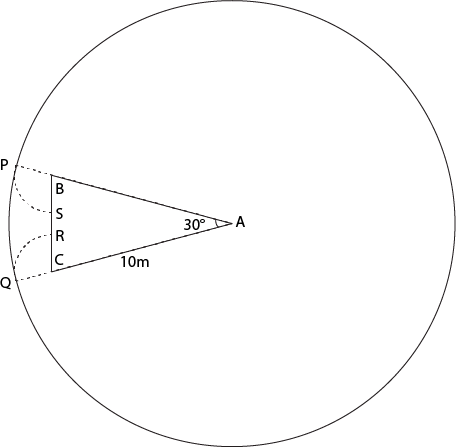

Answer the questions based on the following information. A cow is tethered at point A by a rope. Neither the rope nor the cow is allowed to enter ΔABC.

∠BAC = 30°

I(AB) = I(AC) = 10 m

What is the area that can be grazed by the cow if the length of the rope is 8 m?

What is the area that can be grazed by the cow if the length of the rope is 12 m?

Area grazed by cow will be = Area of the larger circle - Sector APQ + Sector PBS + Sector CQR

Area of larger circle - Sector APQ = $$\pi r^2 - \frac{\pi r^2}{12}$$ = $$132 \pi$$

Sectors PBS and CQR are symmetrical and hence will have equal area.

In triangle ABC, AB = AC => ABC is isosceles triangle.

As A = 30° => B = C =75°

Hence, angle PBS = 180-75 = 105°

Hence, Area of sector PBS = 105/360 * $$\pi * 2^2$$ = $$ 7 \pi / 6$$

Thus area that can be grazed by the cow = $$132 \pi + 2*7 \pi /6$$ = $$403\pi /3$$

Which of the following must be false?

Among all positions for A, if it has first position then either B will be at the 3rd position or C and D will be together which is not possible Hence answer will be A) .

If A is not at the third place, then which of the following options does C have?

If A is not at the third place, then it has only two choices either 2nd or 4th position

So if A is at 2nd position, then B has only fourth position as choice and C can have either first or third position.

And if A is at 4th position, then B has only 2nd position and again C can have either first or third position.

Hence answer will be C.

If A and B are together, then which of the following must be necessarily true?

If A and B are together, then it can't be at first and second place as C and D will be together which is not possible.

Now if A can be at third place and B is at second place then C and D can be placed accordingly.

Answer will be B).

A yearly payment to the servant is Rs. 90 plus one turban. The servant leaves the job after 9 months and receives Rs. 65 and a turban. Then find the price of the turban.

Let's say price of turban is x.

So total price for 12 months will be = $$90+x$$

total price for 9 months = $$\frac{(90+x) \times 9}{12} = (65+x) $$

By solving above equation, we will get value of x= 10.

Four identical coins are placed in a square. For each coin the ratio of area to circumference is same as the ratio of circumference to area. Then find the area of the square that is not covered by the coins.

$$\frac{(\pi r^2)}{2 \pi r}$$ = $$\frac{2 \pi r}{ \pi r^2}$$

So r = 2

Hence required area = (Area of square) - (Area of 4 circles)

= $$(8^2) - (4 \pi (2^2))$$ (As side of square will be 4*2 = 8)

= $$16 (4- \pi)$$

The intended diagram can be drawn as follows:

ABCD is the square and the coins are placed (numbered 1,2,3,4)

Three wheels can complete 60, 36 and 24 revolutions per minute. There is a red spot on each wheel that touches the ground at time zero. After how much time, all these spots will simultaneously touch the ground again?

The first wheel completes a revolution in $$\frac{60}{60}=1$$ second

The second wheel completes a revolution in $$\frac{60}{36}=1\frac{2}{3}$$ second

The third wheel completes a revolution in $$\frac{60}{24}=2\frac{1}{2}$$ second

The three wheels touch the ground simultaneously at time which are multiples of the above three times.

Hence, the required number is $$LCM(1,\frac{5}{3},\frac{5}{2}) = 5$$ seconds.

So, the correct option is option (c)

A certain number, when divided by 899, leaves a remainder 63. Find the remainder when the same number is divided by 29.

Let's say N is our number

N = (899K + 63) or N = ($$29 \times 31$$K) + 63

So when it is divided by 29, remainder will be $$\frac{63}{29}$$ = 5

A is the set of positive integers such that when divided by 2, 3, 4, 5, 6 leaves the remainders 1, 2, 3, 4, 5 respectively. How many integers between 0 and 100 belong to set A?

Let the number 'n' belong to the set A.

Hence, the remainder when n is divided by 2 is 1

The remainder when n is divided by 3 is 2

The remainder when n is divided by 4 is 3

The remainder when n is divided by 5 is 4 and

The remainder when n is divided by 6 is 5

So, when (n+1) is divisible by 2,3,4,5 and 6.

Hence, (n+1) is of the form 60k for some natural number k.

And n is of the form 60k-1

Between numbers 0 and 100, only 59 is of the form above and hence the correct answer is 1

The maximum number of coins collected by any one of them cannot exceed

As least number of coin, one can have is 10

And no two of them possess same number of coins, hence for having maximum number of coins to one person, the distribution of coins will be = 10,12,14,64

maximum no. of coins = 64

If A collected 54 coins, then the difference in the number of coins between the one who collected maximum number of coins and the one who collected the second highest number of coins must be at least

If A collected 54 coins, remaining will be 46.

Now B,C,D must have atleast 10,12,14 coins

So remaining coins will be 10

So difference between maximum and second maximum should be least when second highest will be as maximum as possible.

I.e. difference = 54- (14+10) = 30

If A collected 54 coins and B collected two more coins than twice the number of coins collected by C, then the number of coins collected by B could be

Number of coins with A = 54

Number of coins with B = 2x+2

Number of coins with C = x

Number of coins with D = y

54+3x+2+y = 100

3x+y = 44

If 2x+2 = 28, then x = 13 and y = 5 which is not possible.

If 2x+2 = 20, then x = 9 which is not possible.

If 2x+2 = 26, then x = 12 and y = 8 which is not possible

If 2x+2 = 22, then x = 10 and y = 14 which is feasible

If Akbar and Anthony wear the same colour of shirts, then which of the following is not true?

Akbar can wear either red or blue.

Anthony can wear either red or green.

So when both of them wear same colour that has to be red.

And Amar can wear either blue or green.

Hence our answer will be A.

If two of them wear the same colour, then how many of the following must be false?

I. Amar wears blue and Akbar does not wear green

II. Amar does not wear blue and Akbar wears blue

III. Amar does not wear blue and Akbar does not wear blue

IV. Amar wears green, Akbar does not wear red, Anthony does not wear green

The different possible cases are:

From the table we can see among all of the statements, only fourth statement is false, as if amar wears green, anthony has to wear green.

Number of students who have opted for subjects A, B and C are 60, 84 and 108 respectively. The examination is to be conducted for these students such that only the students of the same subject are allowed in one room. Also the number of students in each room must be same. What is the minimum number of rooms that should be arranged to meet all these conditions?

As we can see here that total number of students are = 60+84+108 = 252

Now given condition is that in one room only the students of the same subject can be there and the number of rooms should be minimum that means the number of students in a particular room will be maximum.

This Maximum number of students will be HCF (Highest common factor) of 60, 84 and 108 and that will be 12

Hence, number of rooms will be = 252/12 = 21

How many five-digit numbers can be formed using the digits 2, 3, 8, 7, 5 exactly once such that the number is divisible by 125?

As we know for a number to be divisible by 125, its last three digits should be divisible by 125

So for a five digit number, with digits 2,3,8,7,5 its last three digits should be 875 and 375

Hence only 4 numbers are possible with its three digits as 875 and 375

I.e. 23875, 32875, 28375, 82375

You can collect as many rubies and emeralds as you can. Each ruby is worth Rs. 4 crore and each emerald is worth Rs. 5 crore. Each ruby weighs 0.3 kg. And each emerald weighs 0.4 kg. Your bag can carry at the most 12 kg. What should you collect to get the maximum wealth?

Let's say number of rubbies are x and emeralds are y.

So 0.3x + 0.4y = 12

And total wealth = 4x+5y

Now putting value of x from eq.1 to eq.2

i.e. total wealth = 4(12-0.4y)/0.3 + 5y

Now for maximizing total wealth y should be equal to zero.

Hence x = 40

I have one-rupee coins, 50-paisa coins and 25-paisa coins. The number of coins are in the ratio 2.5 : 3 : 4. If the total amount with me is Rs. 210, find the number of one-rupee coins.

Let's say number of coins are 2.5x , 3x and 4x

So total amount will be = 2.5x + 3x(0.5) + 4x(0.25) = 210

So x = 42

And number of 1 rs. coins = 2.5x = 105

My son adores chocolates. He likes biscuits. But he hates apples. I told him that he can buy as many chocolates he wishes. But then he must have biscuits twice the number of chocolates and should have apples more than biscuits and chocolates together. Each chocolate cost Re 1. The cost of apple is twice the chocolate and four biscuits are worth one apple. Then which of the following can be the amount that I spent on that evening on my son if number of chocolates, biscuits and apples brought were all integers?

When numbers of chocolates, biscuits and apples are integers.

Now let's say number of chocolates taken 1 , then biscuits will be 2 and apples can be 4,5,6,7

Hence minimum money that should be spent = 1+1+8 = 10 (Hence option C is cancelled)

Now when number of chocolates are 4

Biscuits will be 8

And apples can be 13,14,15....

Now total money spent can be 4+4+26 = 34 and more of it.

Hence answer will be A

Answer the following questions based on the following information.

A company purchases components A and B from Germany and USA respectively. A and B form 30% and 50% of the total production cost. Current gain is 20%. Due to change in the international scenario, cost of the German mark increased by 30% and that of USA dollar increased by 22%. Due to market conditions, the selling price cannot be increased by more than 10%.

What is the maximum current gain possible?

Let the total production cost be 100.

Hence, selling price is 120.

Price of German component A is 30 and the price of the US component B is 50

After change in exchange rate, price of German component is 30*1.3 = 39

and price of US component is 50*1.22=61

Total increase equals 39+61-30-50 = 20

Hence, the minimum production cost is 100+20=120

The maximum possible selling price is 120*110% = 132.

So, maximum possible gain is (132-120)/120 = 10%

If the USA dollar becomes cheap by 12% over its original cost and the cost of German mark increased by 20%, what will be the gain? (The selling price is not altered.)

Let the total production cost be 100.

Hence, selling price is 120.

Price of German component A is 30 and the price of the US component B is 50

After change in exchange rate, price of German component is 30*1.2 = 36

and price of US component is 50*0.88=44

Total increase equals (36+44)-(30+50) = 0

Hence, the total production cost did not change.

As the selling price also did not change, the gain percentage equals 20%

Who wore the red saree?

Since the people wearing yellow saree and the white saree were at the ends, Ms West Bengal was not sitting at one of the ends and was not a runner up, the arrangement is as shown below:

Ms. West Bengal was sitting adjacent to

Since the people wearing yellow saree and the white saree were at the ends, Ms West Bengal was not sitting at one of the ends and was not a runner up, the arrangement is as shown below:

Which saree was worn by Ms Andhra Pradesh?

Since the people wearing yellow saree and the white saree were at the ends, Ms West Bengal was not sitting at one of the ends and was not a runner up, the arrangement is as shown below:

Who was the runner-up?

Since the people wearing yellow saree and the white saree were at the ends, Ms West Bengal was not sitting at one of the ends and was not a runner up, the arrangement is as shown below:

I started climbing up the hill at 6 a.m. and reached the top of the temple at 6 p.m. Next day I started coming down at 6 a.m. and reached the foothill at 6 p.m. I walked on the same road. The road is so short that only one person can walk on it. Although I varied my pace on my way, I never stopped on my way. Then which of the following must be true?

The total time taken for both the journeys is the same. So, a) is incorrect. If he goes with the same speed both ways, he would've been at the same point at noon on both days. So, d) is incorrect. If he does not travel with the same speed in both the directions, he need not be at the same spot at noon. So, option b) is incorrect. Option c) is the correct answer.

What is the digit in the unit’s place of $$2^{51}$$?

The last digit of powers of 2 follow a pattern as given below.

The last digit of $$2^1$$ is 2

The last digit of $$2^2$$ is 4

The last digit of $$2^3$$ is 8

The last digit of $$2^4$$ is 6

The last digit of $$2^5$$ is 2

The last digit of $$2^6$$ is 4

The last digit of $$2^7$$ is 8

The last digit of $$2^8$$ is 6

Hence, the last digit of $$2^{51}$$ is 8

There are two containers: the first contains 500 ml of alcohol, while the second contains 500 ml of water. Three cups of alcohol from the first container is taken out and is mixed well in the second container. Then three cups of this mixture is taken out and is mixed in the first container. Let A denote the proportion of water in the first container and B denote the proportion of alcohol in the second container. Then,

Let the volume of the cup be V.

Hence, after removing three cups of alcohol from the first container,

Volume of alcohol in the first container is 500-3V

Volume of water in the second container is 500 and volume of alcohol in the second container is 3V.

So, in each cup, the amount of water contained is $$\frac{500}{500+3V}*V$$

Hence, after adding back 3 cups of the mixture, amount of water in the first container is $$0+\frac{1500V}{500+3V} $$

Amount of alcohol contained in the second container is $$3V - \frac{9V^2}{500+3V} = \frac{1500V}{500+3V}$$

So, the required proportion of water in the first container and alcohol in the second container are equal.

A number is formed by writing first 54 natural numbers next to each other as 12345678910111213 ... Find the remainder when this number is divided by 8.

For a number to be divisible by 8, last 3 digits must be divisible by 8.

Last 3 digits of this number are 354.

354 mod 8 = 2

Hence, 2 is the remainder.

A, B, C, D, ..., X, Y, Z are the players who participated in a tournament. Everyone played with every other player exactly once. A win scores 2 points, a draw scores 1 point and a loss scores 0 point. None of the matches ended in a draw. No two players scored the same score. At the end of the tournament, by ranking list is published which is in accordance with the alphabetical order. Then

The ranking list would be in the order A, B, C, D......., X, Y, Z. Now the A wins all his 25 matches, B wins 24 matches and lost to A. C wins 23 matches and lost to A and B. In this way N 12 matches and looses 13 matches to A,B,C,D....,M

Select the option that best replaces the phrase in quotes. British Airspace has been 'focusing on building European links'.

The best word to use for "links" is "forging".

Hence, "focusing on forging European links" is the correct phrase.

Select the option that best replaces the phrase in quotes. The appetite of banks for funds was lost under the onslaught of the slowdown, corporates refused to borrow even as 'bank deposits flourished'.

Bank deposits are countable. So they swell. They don't flourish. "To flourish" means to develop. The correct answer is option b.

Select the option that best replaces the phrase in quotes. The 8th-century revival of Byzantine learning is 'an inexplicable phenomenon', and its economic and military precursors have yet to be discovered.

There is no error in the given sentence. "An inexplicable phenomenon" means a phenomenon which cannot be explained. So the usage is contextually as well as grammatically correct.

Select the option that best replaces the phrase in quotes. The management can still hire freely but 'cannot scold freely'.

"cannot scold freely" means "cannot scold whenever the management want". This can be replaced by "cannot scold at will."

Select the option that best replaces the phrase in quotes.

Many people mistake familiarity for a vulgar style, and suppose that to write without affectation 'is to write at random speed'.

Option C and Option D are incorrect as the author talks about writing without affectation i.e. writing without any pretension. Hence, it can be mistaken for writing without consideration or care and not writing fast.

Between options A and B, A contains the correct phrase 'at random'. The phrase means without a care and in a disorderly manner. "Writing randomly" does not carry the same implication. Also, here the modifier 'random' is a misplaced modifier. It is modifying the way of writing instead of modifying what is written.

Fill in the blanks: Football evokes a ___ response in India compared to cricket, that almost ___ the nation.

Lukewarm is the correct usage in the first blank as it means not entusiastic. "Electifies" correctly matches the second blank. Hence the correct option is B.

Fill in the blanks: Social studies, science matters of health and safety, the very atmosphere of the classroom —these areas are few of the ___ for the ___ of proper emotional reactions.

Option A is incorrect as in the usage of "these areas", things cannot be used. Similarly option C is incorrect. Option B is incorrect because"basis of proper emotional reaction" is an incorrect usage.

Fill in the blanks: When children become more experienced with words as visual symbols, they find that they can gain meaning without making ___ sounds.

Audible means which can be heard. Audible sounds means the sounds which can be heard..

Fill in the blanks: Learning is more efficient when it is ___. It is less efficient when it is ___.

The two set of words must be opposite to each other. Option A and D are correct in this case. But option A is contextually incorrec as learning cannot be fun if its is fast. The correct answer is D.

Fill in the blanks: To a greater or lesser degree all the civilized countries of the world are made up of a small class of rulers ___ and of a large class of subjects ___.

Option D is incorrect as it contradicts the statements as "rulers do not get ruled." Option A is contextually incorrect as it does not make any sense. Option B is incorrect as powerfully corrupt is grammatically incorrect. Option C is the best match.

Fill in the blanks: Simple arithmetic tells us that there is more ___ than ___.

Option C is incorrect as impracticality and knowledge cannot be related because they are totally different.

Option B is incorrect as improvisation means to perform spontaneously and improving means to get better which are not related.

Option D is contextually incorrect. Option A is correct as it talks about imitation and invention which are related terms.

Fill in the blanks: As a step towards protesting against the spiralling prices, the farmers have decided to stage a picket in an effort to ___.

Farmers face problems due to the spiralling prices. So they protest in order to make their pleas head. "Virility" means manliness which has no context in this passage. The protest need not curb the prices. It will make their pleas heard. "Topple the government" is an extreme form which does not demand merit in this passage. Option B is the correct answer.

Fill in the blanks: Science is a sort of news agency comparable ___ to other news agencies.

Option A is incorrect as principally is an incorrect usage. Principal means a chief which does not go in this context. Hencee C is incorrect. Among B and D, B is more suitable as in principle means in primary rule which goes with the tone of the passage.

Fill in the blanks:

Most political leaders acquire their position by causing a large number of people to believe that these leaders are ___ by altruistic desires.

Options B and C are incorrect as desires cannot convince or categorise people. Between options A and D, "actuated" which means motivated is a better fit as "led" is generally used for other people and not inanimate objects like "desires".

Fill in the blanks: Everyone will admit that swindling one's fellow beings is a necessary practice; upon it is based the really sound commercial success formula — ___.

Swindle means to use deception to deprive someone's possession. It means that you have an unequal exchange where you didn't give much of your possession and you robbed the other person of his/her possession. Option C summarises it correctly.

Arrange sentences A, B, C and D between sentences 1 and 6 to form a logical sequence of six sentences.

1. Buddhism is a way to salvation.

A. But Buddhism is more severely analytical.

B. In the Christian tradition there is also a concern for the fate of human society conceived as a whole, rather than merely as a sum or network of individuals.

C. Salvation is a property, or achievement of individuals.

D. Not only does it dissolve society into individuals, the individual in turn is dissolved into component parts and instants, a stream of events.

6. In modern terminology, Buddhist doctrine is reductionist.

Sentence C is the starting sentence as it talks about the as salvation. Sentence B is the next sentence as it mentions the traditions of christanity. A and D differentiates the Buddhism from Christanity. The correct order is CBAD.

Arrange sentences A, B, C and D between sentences 1 and 6 to form a logical sequence of six sentences.

1. The problem of improving Indian agriculture is both a sociological and an administrative one.

A. It also appears that there is a direct relationship between the size of a state and development.

B. The issues of Indian development, and the problem of India's agricultural sector, will remain with us long into the next century.

C. Without improving Indian agriculture, no liberalisation and delicensing will be able to help India.

D. At the end of the day, there has to be a ferment and movement of life and action in the vast segment of rural India.

6. When it starts marching, India will fly.

Statement A highlights the additional issue. Statement B substantiates A. Option C highlights the issues facing indian agriculture as mentioned in B. Option D is the last sentence as in 6, "it" refers to rural class.

Arrange sentences A, B, C and D between sentences 1 and 6 to form a logical sequence of six sentences.

1. Good literary magazines have always been good because of their editors.

A. Furthermore, to edit by committee, as it were, would prevent any magazine from finding its own identity.

B. The more quirky and idiosyncratic they have been, the better the magazine is, at least as a general rule.

C. But the number of editors one can have for a magazine should also be determined by the number of contributions to it.

D. To have four editors for an issue that contains only seven contributions, it is a bit silly to start with.

6. However, in spite of this anomaly, the magazine does acquire merit in its attempt to give a comprehensive view of the Indian literary scene as it is today.

The first sentence talks about magazines. The same idea is continued in sentence B. Hence, B follows the first sentence.

CD is a pair because the "number of editors" concept is introduced in C and then an example is taken in D.

Hence, BCDA is the answer.

Arrange sentences A, B, C and D between sentences 1 and 6 to form a logical sequence of six sentences.

1. It is the success story of the Indian expatriate in the US which today hogs much of the media coverage in India.

A. East and West, the twain have met quite comfortably in their person, thank you.

B. Especially in its more recent romancing — the-NRI phase.

C. Seldom does the price of getting there — more like not getting there — or what's going on behind those sunny smiles get so much media hype.

D. Well groomed, with their perfect Colgate smiles, and hair in place, they appear the picture of confidence which comes from having arrived.

6. The festival of feature films and documentaries made by Americans of Indian descent being screened this fortnight, goes a long way in filling those gaps.

The pronoun "it" in statement B refers to the media attention mentioned in statement 1. Hence, 1-B are a pair. Statements A and D describe the NRIs introduced in B and hence should come after B. As A concludes from the outward characteristics mentioned in D, it should follow D. C mentions the gap in information provided about NRIs and 6 mentions how the film festival is filling those gaps. Hence, C-6 are a pair. Hence, the order is 1BDAC6.

Arrange sentences A, B, C and D between sentences 1 and 6 to form a logical sequence of six sentences.

1. A market for Indian art has existed ever since the international art scene sprang to life.

A. But interest in architectural conceits is an unanticipated fallout of the Festivals of India of the '80s, which were designed to increase exports of Indian crafts.

B. Simultaneously, the Indian elite discarded their synthetic sarees and kitsch plastic furniture and a market came into being.

C. Western dealers, unhappy in a market afflicted by violent price fluctuations and unpredictable profit margins, began to look East, and found cheap antiques with irresistible appeal.

D. The fortunes of the Delhi supremos, the Jew Town dealers in Cochin and myriad others around the country were made.

6. A chain of command was established, from the local contacts to the provincial dealers and up to the big boys, who entertain the Italians and the French, cutting deals worth lakhs in warehouses worth crores.

C and B forms a pair as they illustrate simultaneous happenings- one where Western dealers began to look and East and their Indian counterpart discarded synthetic sarees and plastic furniture. Only C has both these sentences together. Thus, C is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. He was carrying his jacket and walked with his head thrown back.

B. As Annette neared the lamp she saw a figure walking slowly.

C. For a while Michael walked on and she followed 20 paces behind.

D. With a mixture of terror and triumph of recognition she slackened her pace.

The opening sentence is B - it introduces the character the rest of the paragraph is talking about. This is followed by A, which describes the person. The next sentence is D, which talks about the reaction of Annette. The last sentence is C. So, the correct order of sentences is BADC. Option b) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. However, the real challenge today is in unlearning, which is much harder.

B. But the new world of business behaves differently from the world in which we grew up.

C. Learning is important for both people and organisations.

D. Each of us has a 'mental model' that we've used over the years to make sense.

Sentences A and B start with conjunctions. So, they cannot be used to open a paragraph. The best opening sentence is C. This is immediately followed by A, which gives a contradictory opinion to the one in C. A is followed by D which further explores the idea in A. The last sentence is B. So, option a) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. There was nothing quite like a heavy downpour of rain to make life worthwhile.

B. We reached the field, soaked to the skin, and surrounded it.

C. The wet, as far as he was concerned, was ideal.

D. There, sure enough, stood Claudius, looking like a debauched Roman emperor under a shower.

B is the best opening sentence - it talks about the setting of the scene. This is followed by D, which talks about what happened when they reached the field. This is then followed by C, which talks more about the person introduced in sentence D. The closing sentence is A. So, the correct order of sentences is BDCA. Option b) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. Alex had never been happy with his Indian origins.

B. He set about rectifying this grave injustice by making his house in his own image of a country manor.

C. Fate had been unfair to him; if he had had his wish, he would have been a count or an Earl on some English estate, or a medieval monarch in a chateau in France.

D. This illusion of misplaced grandeur, his wife felt, would be Alex's undoing.

The first sentence is A - it introduces the main character in the paragraph. This is followed by C, which gives a background about that person. B and D is a pair. 'This illusion' in D refers to Alex not being happy about his Indian origins - sentence B. So, the correct order of sentences is ACBD. Option c) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. The influence is reflected the most in beaded evening wear.

B. Increasingly, the influence of India's colours and cuts can be seen on western styles.

C. And even as Nehru jackets and Jodhpurs remain staples of the fashion world, designers such as Armani and McFadden have turned to the sleek silhouette of the churidar this year.

D. Indian hot pink, paprika and saffron continue to be popular colours, year in and year out.

B is the first sentence of the paragraph. It introduces the subject of the paragraph - the influence of Indian wear on the west. This is then followed by A, which talks about where the maximum influence is. D, which further elaborates the idea, follows A. The concluding sentence is C. Option a) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. Such a national policy will surely divide and never unite the people.

B. In fact, it suits the purpose of the politicians; they can drag the people into submission by appealing to them in the name of religion.

C. In order to inculcate the unquestioning belief they condemn the other states, which do not follow their religion.

D. The emergence of the theocratic states, where all types of crimes are committed in the name of religion, has revived the religion of the Middle Ages.

CA is a pair. The 'policy' in A refers to the condemnation of the states that do not follow a particular religion. The opening sentence of the paragraph is D and this is immediately followed by B. So, the order of sentences is DBCA. Option b) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. His left-hand concealed a blackjack, his right-hand groped for the torch in his pocket.

B. The meeting was scheduled for 9 o'clock, and his watch showed the time to be a quarter to nine.

C. The man lurked in the corner, away from the glare of light.

D. His heart thumped in his chest, sweat beads formed themselves on his forehead, his mouth was dry.

C is thee starting of the sentencee where the author talks about the situation of man and his appearence. Option A continues the tone of the appearence. Option B mentions the time due to which his heart thumped as mentioned in option D. Hence the sequence is CABD.

Arrange the following sentences to form a coherent paragraph

A. The director walked into the room and took a look around the class.

B. Mitch wanted to scream — the illogicality of the entire scene struck him dumb.

C. The managers stared at him with the look of fear that no democratic country should tolerate in its people.

D. He walked out of the room — it was his irrevocable protest against an insensible and insensitive situation.

AC is a pair. 'Him' in C refers to 'the director' in A. BD is also a pair. 'He' in D refers to 'Mitch' in B. Also, A is the best opening sentence. So, the correct order of sentences is ACBD. Option a) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. The establishment of the Third Reich influenced events in American history by starting a chain of events which culminated in war between Germany and the United States.

B. The Neutrality Acts of 1935 and 1936 prohibited trade with any belligerents or loans to them.

C. While speaking out against Hitler's atrocities, the American people generally favoured isolationist policies and neutrality.

D. The complete destruction of democracy, the persecution of Jews, the war on religion, the cruelty and barbarism of the allies, caused great indignation in this country and brought on fear of another World War.

Option A is the starting sentence where the author focuses on the start f hostility between Germany and USA. Option D continues the tone by stating the consequences. CB are mandatory pair if we look at the word "Neutrality". ADCB is the correct sequence.

Arrange the following sentences to form a coherent paragraph

A. An essay which appeals chiefly to the intellect is Francis Bacon's Of Studies.

B. His careful tripartite division of studies expressed succinctly in aphoristic prose demands the complete attention of the mind of the reader.

C. He considers studies as they should be; for pleasure, for self-improvement, for business.

D. He considers the evils of excess study: laziness, affectation, and preciosity.

A is the opening sentence. This is followed by B, which describes why the essay talked about in A appeals to the intellect. D should follow C. C talks about studies and D talks about 'excess' study. So, the correct order of sentences is ABCD. Option b) is the correct answer.

Arrange the following sentences to form a coherent paragraph

A. By reasoning we mean the mental process of drawing an inference from two or more statements or going from the inference to the statements, which yield that inference.

B. So logical reasoning covers those types of questions, which imply drawing an inference from the problems.

C. Logic means, if we take its original meaning, the science of valid reasoning.

D. Clearly, for understanding arguments and for drawing the inference correctly, it is necessary that we should understand the statements first.

C is the best opening sentence. It introduces the topic of the paragraph - logic. This is followed by A, which goes on to explain the meaning of reasoning. This is then followed by B, which explains 'logical reasoning'. The concluding sentence is D. The correct order of sentences is CABD. Option b) is the correct answer.

Select the pair of sentences that relates logically to the given statement. Either Sita is sick or she is careless.

A. Sita is not sick.

B. Sita is not careless.

C. Sita is sick.

D. Sita is careless.

Either Sita is sick or she is careless => Sita is sick or she is careless.

Consider the pair AD. A says "Sita is not sick". So, it implies that she is careless, which is what is mentioned in statement D. So, AD relate to the original sentence.

Select the pair of sentences that relates logically to the given statement. Ram gets a swollen nose whenever he eats hamburgers.

A. Ram gets a swollen nose.

B. Ram does not eat hamburgers.

C. Ram does not get a swollen nose.

D. Ram eats hamburgers.

The statement can be written as follows:

Ram eats a hamburger => Ram get a swollen nose

Ram did not get a swollen nose => Ram did not eat a hamburger

Option d) is the correct answer.

Select the pair of sentences that relates logically to the given statement. Either the employees have no confidence in the management or they are hostile by nature.

A. They are not hostile by nature.

B. They are hostile by nature.

C. They have confidence in the management.

D. They have no confidence in the management.

The members are either hostile or have no confidence.

Consider the pair of sentences CB.

C says the members have confidence in the management. So, they do not have 'no confidence' => The members should be hostile in nature, which is what statement B says. So, option b) is the correct answer.

Select the pair of sentences that relates logically to the given statement. Whenever Ram reads late into the night, his father beats him.

A. His father does not beat Ram.

B. Ram reads late into the night.

C. Ram reads early in the morning.

D. Ram's father beats him in the morning.

The sentence can be written as follows:

Ram reads late into the night => His father beats him

Ram's father did not beat him => Ram did not read late into the night

So, none of the pairs given in the options follow from the statement.

Select the pair of sentences that relates logically to the given statement. All irresponsible parents shout if their children do not cavort.

A. All irresponsible parents do not shout.

B. Children cavort.

C. Children do not cavort.

D. All irresponsible parents shout.

The statement can be written as follows:

Children do not cavort => Irresponsible parents shout

Irresponsible parents did not shout => Children cavorted

So, AB follows from the statement.

Choose the set in which the third statement is a logical conclusion of the first two.

A. Some Xs are Ps. Some Ps are Ys. Some Xs are Ys.

B. All Sonas are bright. Some bright are crazy. Some Sonas are crazy.

C. No faith is strong. Only strong have biceps. No faith has biceps.

D. All men are weak. Some weak are strong. Some strong are weak.

Statement A: There need not be an intersection between the sets Xs and Ys.

Statement B: There need not be an intersection between the sets Sonas and Crazy.

Statement D: Third statement follows only from the second statement.

The third statement in C follows from its first two statements.

Option b) is the correct answer.

Choose the set in which the third statement is a logical conclusion of the first two.

A. Some icicles are cycles. All cycles are men. Some icicles are men.

B. All girls are teeth. No teeth is yellow. No girls are yellow.

C. No hand is foot. Some foot are heads. Some hands are heads.

D. Every man has a wife. All wives are devoted. No devoted has a husband.

Statement A: Since all cycles are men and some iciles are cycles, it follows that some iciles are definitely men.

Statement B: Girls is a subset of Teeth. There is no intersection between the sets Teeth and Yellow. So, there is no intersection between the sets Girls and Yellow.

The third sentences in C and D need not necessarily follow from the respective first two statements. Option b) is the correct answer.

Choose the set in which the third statement is a logical conclusion of the first two.

A. No sun is not white. All moon is sun. All moon is white.

B. All windows are open. No open space is allocated. All window is closed space.

C. No German can fire. All Americans bombard. Both, Germans and Americans can fight.

D. No X is Z. No Z is Y. No X is Y.

Statement A: No sun is not white => All Sun is white. So, Sun is a subset of white. All moon is sun => Moon is a subset of Sun. So moon is a subset of white.

In none of the other three statements do the third sentences follow from the respective first two statements.

Option a) is the correct answer.

Choose the set in which the third statement is a logical conclusion of the first two.

A. All Ts are square. All squares are rectangular. All Ts are rectangular.

B. Some fat are elongated. Some elongated things are huge. Some fat are huge.

C. Idiots are bumblers. Bumblers fumble. Idiots fumble.

D. Water is good for health. Health foods are rare. Water is rare.

In both A and C the third statement is logically concuded. The reasoning is if A = B, B = C then A = C.

Similarly T's = Square, Square = Rectangle then T's = Rectangle.

Idiots = Bumblers, Bumblers = Fumble then Idiots = Fumble

Efficiency is all right in its place, in the shop, the factory, the store. The trouble with efficiency is that it wants to rule our play as well as our work; it won't be content to reign in the shop, it follows us home. It can be inferred from the above passage that

The author is of the opinion that one cannot limit efficiency to just work. It tends to affect a person's non-work life as well. In other words, efficiency can become all-pervading. Option a) is the correct answer.

In order to ease the traffic congestion, the transport planners decided to have a sophisticated system of elevated monorail travel in the city. However, it was pointed out by somebody that a metro rail system would be a more effective solution to the traffic problem. The plan was thus stalled. Moreover, since a budget had not been drawn up for the project, it was deemed fit to stall the work of the monorail for some time. In the meanwhile, the traffic planners of the city decided to build an efficient system of subways and flyovers in the city with the aim of easing the same problem. At the instant when the planners were preparing to award the contracts to the concerned parties, the transport planners came up with the contention that the subways interfered with the site of a pillar of the monorail system. The traffic planners had to give up the idea and think of other possible solutions.

Which of the following can we infer from the above passage?

Option A cannot be inferred as it is nowhere mentioned. Option B is not necessarily true. The two groups may not agree to each others plans even if they are friendly with each other. Thus, just from the fact that they opposed each others plans we cannot infer that there is contention between the two groups. From the paragraph, we can infer that neither of the two groups can proceed i.e. neither the traffic planners nor the transport planners can move ahead with any plan. Thus, both the parties are dead-locked. Hence, we can infer option C.

The company encourages its managers to interact regularly, without a pre-set agenda, to discuss issues concerning the company and society. This idea has been borrowed from the ancient Indian concept of religious congregation, called satsang. Designations are forgotten during these meetings; hence, it is not uncommon in these meetings to find a sales engineer questioning the CEO on some corporate policy or his knowledge of customers. Based on the information provided in the above passage, it can be inferred that

From the argument, we understand the following points: 1. The company is trying to instill the spirit of dialogue in its employees. 2. This dialogue is agnostic of position or title of the employee.

So, we can infer that the company believes in fostering the spirit of dialogue without degenerating it into a positioning based debate. Option B is the correct answer.

In option C, there is an assumption that the company had some inter-personal problems in the past. However, there is no such information in the passage from which we can infer the assumption. Also, we have to choose the answer according to the contents of the given paragraph. Therefore, option C is incorrect.

From Cochin to Shimla, the new culture vultures are tearing down acres of India's architectural treasures. Ancestral owners are often fobbed off with a few hundred rupees for an exquisitely carved door or window, which fetches fifty times that much from foreign dealers, and yet more from the drawing room sophisticates of Europe and the US. The reason for such shameless rape of the Indian architectural wealth can perhaps, not wrongly, be attributed to the unfortunate blend of activist disunity and the local indifference. It can be inferred from the above passage that

Option b) is incorrect because it says 'only' India is not proud of its culture, which is incorrect.

Option c) is incorrect because we cannot infer if 'most' Indian families have sold off their heirlooms.

Option d) is incorrect because the market is US and Europe and not India. India is the souce.

Option a) can be inferred.

Deepa Metha's Fire is under fire from the country's self-appointed moral police. Their contention is that the film is a violation of the Indian cultural mores and cannot be allowed to influence the Indian psyche. According to them, such films ruin the moral fabric of the nation, which must be protected and defended against such intrusions at all cost, even at the cost of cultural dictatorship.

Based on the information in the above passage, it can be inferred that

According to the paragraph, the moral police thinks that the movies are bound to affect the judgment of Indian audience and hence they need to censor the movie in order to preserve their already existing judgment and protect them from the influence of such a work.

Option B correctly summarizes the inference.

The dominant modern belief is that the soundest foundation of peace would be universal prosperity. One may look in vain for historical evidence that the rich have regularly been more peaceful than the poor, but then it can be argued that they have never felt secure against the poor; that their aggressiveness stemmed from fear; and that the situation would be quite different if everybody were rich. It can be inferred from the above passage that

The sentence is option b) is opposite to what the argument is conveying.

Option a) can be inferred. According to the argument, a lot of aggression has stemmed because the rich want to defend themselves against the poor. In other words, the aggression has stemmed from the desire of the haves to defend themselves against the have-nots.

The effect produced on the mind by travelling depends entirely on the mind of the traveller and on the way in which he conducts himself. The chief idea of one very common type of traveller is to see as many objects of interest as he possibly can. If he can only after his return home say that he has seen such and such temple, castle, picture gallery, or museum, he is perfectly satisfied. Far different is the effect of travels upon those who leave their country with a mind prepared by culture to feel intelligent admiration for all the beauties of nature and art to be found in foreign lands. When they visit a new place, instead of hurrying from temple to museum to picture gallery, they allow the spirit of the place to sink into their minds, and only visit such monuments as the time they have at their disposal allows them to contemplate without irreverent haste.

It can be inferred from the above passage that

According to the passage, the latter kind of travelers only visit such monuments as the time they have at their disposal allows them to contemplate without irreverent haste.

A is incorrect as the preference of the writer is not the main subject of focus.

B is way too harsh. This cannot be inferred from the passage.

C correctly describes the second kind of travelers.

Thus, C is the correct answer.

Whether we look at the intrinsic value of our literature, or at the particular situation of this country, we shall see the strongest reason to think that of all foreign tongues, the English tongue is that which would be the most useful to our native subjects. It can be inferred that

Option a) is incorrect because we cannot infer that the speaker is a colonist. The speaker could be a neutral observer. So, we cannot say that he has the good of the nation at heard. English is not an issue that is related only to the colonial empire. We cannot infer the statement in option c) also.

Option d) is the correct answer.