Identify the correct statement:

IIFT 2011 Question Paper

Before the internet, one of the most rapid changes to the global economy and trade was wrought by something so blatantly useful that it is hard to imagine a struggle to get it adopted: the shipping container. In the early 1960s, before the standard container became ubiquitous, freight costs were I0 per cent of the value of US imports, about the same barrier to trade as the average official government import tariff. Yet in a journey that went halfway round the world, half of those costs could be incurred in two ten-mile movements through the ports at either end. The predominant ‘break-bulk’ method, where each shipment was individually split up into loads that could be handled by a team of dockers, was vastly complex and labour-intensive. Ships could take weeks or months to load, as a huge variety of cargoes of different weights, shapes and sizes had to be stacked together by hand. Indeed, one of the most unreliable aspects of such a labour-intensive process was the labour. Ports, like mines, were frequently seething pits of industrial unrest. Irregular work on one side combined with what was often a tight-knit, well - organized labour community on the other.

In 1956, loading break-bulk cargo cost $5.83 per ton. The entrepreneurial genius who saw the possibilities for standardized container shipping, Malcolm McLean, floated his first containerized ship in that year and claimed to be able to shift cargo for 15.8 cents a ton. Boxes of the same size that could be loaded by crane and neatly stacked were much faster to load. Moreover, carrying cargo in a standard container would allow it to be shifted between truck, train and ship without having to be repacked each time.

But between McLean’s container and the standardization of the global market were an array of formidable obstacles. They began at home in the US with the official Interstate Commerce Commission, which could prevent price competition by setting rates for freight haulage by route and commodity, and the powerful International Longshoremen's Association (ILA) labour union. More broadly, the biggest hurdle was achieving what economists call ‘network effects’: the benefit of a standard technology rises exponentially as more people use it. To dominate world trade, containers had to be easily interchangeable between different shipping lines, ports, trucks and railcars. And to maximize efficiency, they all needed to be the same size. The adoption of a network technology often involves overcoming the resistance of those who are heavily invested in the old system. And while the efficiency gains are clear to see, there are very obvious losers as well as winners. For containerization, perhaps the most spectacular example was the demise of New York City as a port.

In the early I950s, New York handled a third of US seaborne trade in manufactured goods. But it was woefully inefficient, even with existing break-bulk technology: 283 piers, 98 of which were able to handle ocean-going ships, jutted out into the river from Brooklyn and Manhattan. Trucks bound‘ for the docks had to fiive through the crowded, narrow streets of Manhattan, wait for an hour or two before even entering a pier, and then undergo a laborious two-stage process in which the goods foot were fithr unloaded into a transit shed and then loaded onto a ship. ‘Public loader’ work gangs held exclusive rights to load and unload on a particular pier, a power in effect granted by the ILA, which enforced its monopoly with sabotage and violence against than competitors. The ILA fought ferociously against containerization, correctly foreseeing that it would destroy their privileged position as bandits controlling the mountain pass. On this occasion, bypassing them simply involved going across the river. A container port was built in New Jersey, where a 1500-foot wharf allowed ships to dock parallel to shore and containers to be lified on and off by crane. Between 1963 - 4 and 1975 - 6, the number of days worked by longshoremen in Manhattan went from 1.4 million to 127,041.

Containers rapidly captured the transatlantic market, and then the growing trade with Asia. The effect of containerization is hard to see immediately in freight rates, since the oil price hikes of the 1970s kept them high, but the speed with which shippers adopted; containerization made it clear it brought big benefits of efficiency and cost. The extraordinary growth of the Asian tiger economies of Singapore, Taiwan, Korea and Hong Kong, which based their development strategy on exports, was greatly helped by the container trade that quickly built up between the US and east Asia. Ocean-borne exports from South Korea were 2.9 million tons in 1969 and 6 million in 1973, and its exports to the US tripled.

But the new technology did not get adopted all on its own. It needed a couple of pushes from government - both, as it happens, largely to do with the military. As far as the ships were concerned, the same link between the merchant and military navy that had inspired the Navigation Acts in seventeenth-century England endured into twentieth-century America. The government's first helping hand was to give a spur to the system by adopting it to transport military cargo. The US armed forces, seeing the efficiency of the system, started contracting McLean’s company Pan-Atlantic, later renamed Sea-land, to carry equipment to the quarter of a million American soldiers stationed in Western Europe. One of the few benefits of America's misadventure in Vietnam was a rapid expansion of containerization. Because war involves massive movements of men and material, it is often armies that pioneer new techniques in supply chains.

The government’s other role was in banging heads together sufficiently to get all companies to accept the same size container. Standard sizes were essential to deliver the economies of scale that came from interchangeability - which, as far as the military was concerned, was vital if the ships had to be commandeered in case war broke out. This was a significant problem to overcome, not least because all the companies that had started using the container had settled on different sizes. Pan- Atlantic used 35- foot containers, because that was the maximum size allowed on the highways in its home base in New Jersey. Another of the big shipping companies, Matson Navigation, used a 24-foot container since its biggest trade was in canned pineapple from Hawaii, and a container bigger than that would have been too heavy for a crane to lift. Grace Line, which largely traded with Latin America, used a foot container that was easier to truck around winding mountain roads.

Establishing a US standard and then getting it adopted internationally took more than a decade. Indeed, not only did the US Maritime Administration have to mediate in these rivalries but also to fight its own turf battles with the American Standards Association, an agency set up by the private sector. The matter was settled by using the power of federal money: the Federal Maritime Board (FMB), which handed out to public subsidies for shipbuilding, decreed that only the 8 x 8-foot containers in the lengths of l0, 20, 30 or 40 feet would be eligible for handouts.

Solution

In the early 1960s, before the standard container became ubiquitous, freight costs were I0 per cent of the value of US imports, about the same barrier to trade as the average official government import tariff. - Option A is incorrect.

From the 5th paragraph, option B is correct.

It has not been mentioned that imports increased Option C is incorrect.

The weight of boxes were the real reason, not the size. Option D is wrong.

Hence, option B is the correct answer.

Identify the false statement:

Solution

Option B can be inferred from the sixth paragraph.

Option C can be inferred from the first paragraph.

Option D can be inferred from the last paragraph.

Trucks bound‘ for the docks had to five through the crowded, narrow streets of Manhattan, wait for an hour or two before even entering a pier, and then undergo a laborious two-stage process in which the goods foot were fithr unloaded into a transit shed and then loaded onto a ship. - Option A is incorrect.

Hence, option A is the correct answer.

The emergence of containerization technology in early seventies resulted in:

Solution

The effect of containerization is hard to see immediately in freight rates, since the oil price hikes of the 1970s kept them high, but the speed with which shippers adopted; containerization made it clear it brought big benefits of efficiency and cost. The extraordinary growth of the Asian tiger economies of Singapore, Taiwan, Korea and Hong Kong, which based their development strategy on exports, was greatly helped by the container trade that quickly built up between the US and east Asia. - From these lines, option C can be inferred.

Hence, option C is the correct answer.

Match the following

Solution

Option D) a - iii; b - iv, c - ii; d - i is the correct answer.

The correct matching based on the passage is:

ILA (International Longshoremen's Association) → Dockers (iii)

The ILA represented dockworkers who resisted containerization because it reduced their labor demand.

FMB (Federal Maritime Board) → Standardization (iv)

The FMB played a key role in enforcing standardized container sizes by tying subsidies to specific container dimensions.

Grace Line → Mountain roads (ii)

Grace Line used a specific container size that was easier to transport on winding mountain roads in Latin America.

McLean (Malcolm McLean) → New Jersey (i)

Malcolm McLean pioneered container shipping and built a container port in New Jersey.

Read the following passage carefully and answer the questions given at the end.

I have tried to introduce into the discussion a number of attributes of consumer behaviour and motivations, which I believe are important inputs into devising a strategy for commercially viable financial inclusion. These related broadly to the (i) the sources of livelihood of the potential consumer segment for financial inclusion (ii) how they spend their money, particularly on non-regular items (iii) their choices and motivations with respect to saving and (iv) their motivations for borrowing and their ability to access institutional sources of finance for their basic requirements. In discussing each of these sets of issues, I spent some time drawing implications for business strategies by financial service providers. In this section, I will briefly highlight, at the risk of some repetition, what I consider to be the key messages of the lecture.

The first message emerges from the preliminary discussion on the current scenario on financial inclusion, both at the aggregate level and across income categories. The data suggest that even savings accounts, the most basic financial service, have low penetration amongst the lowest income households. I want to emphasize that we are not talking about Below Poverty Line households only; Rs. 50,000 per year in 2007, while perhaps not quite middle class, was certainly quite far above the official poverty line. The same concerns about lack of penetration amongst the lowest income group for loans also arise. To reiterate the question that arises from these data patterns: is this because people can’t access banks or other service providers or because they don’t see value in doing so? This question needs to be addressed if an effective inclusion strategy is to be developed.

The second message is that the process of financial inclusion is going to be incomplete and inadequate if it is measured only in terms of new accounts being opened and operated. From the employment and earning patterns, there emerged a sense that better access to various kinds of financial services would help to increase the livelihood potential of a number of occupational categories, which in turn would help reduce the income differentials between these and more regular, salaried jobs. The fact that a huge proportion of the Indian workforce is either self- employed and in the casual labour segment suggests the need for products that will make access to credit easier to the former, while offering opportunities for risk mitigation and consumption smoothing to the latter.

The third message emerges from the analysis of expenditure patterns is the significance of infrequent, but quantitatively significant expenditures like ceremonies and medical costs. Essentially, dealing with these kinds of expenditures requires either low- cost insurance options, supported by a correspondingly low-cost health care system or a low level systematic investment plan, which allows even poor households to create enough of a buffer to deal with these demands as and when they arise. As has already been pointed out, it is not as though such products are not being offered by domestic financial service providers. It is really a matter of extending them to make them accessible to a very large number of lower income households, with a low and possibly uncertain ability to maintain regular contributions.

The fourth message comes strongly from the motivations to both save and borrow, which, as one might reasonably expect, significantly overlap with each other. It is striking that the need to deal with emergencies, both financial and medical, plays such an important role in both sets of motivations. The latter is, as has been said, amenable to a low-cost, mass insurance scheme, with the attendant service provision. However, the former, which is a theme that recurs through the entire discussion on consumer characteristics, certainly suggests that the need for some kind of income and consumption smoothing product is a significant one in an effective financial inclusion agenda. This, of course, raises broader questions about the role of social safety nets, which offer at least some minimum income security and consumption smoothing. How extensive these mechanisms should be, how much security they should offer and for how long and how they should be financed are fundamental policy questions that go beyond the realm of the financial sector. However, to the extent that risk mitigation is a significant financial need, it must receive the attention of any meaningful financial inclusion strategy, in a way which provides practical answers to all these three questions.

The fifth and final message is actually the point I began the lecture with. It is the critical importance of the principle of commercial viability. Every aspect of a financial inclusion strategy — whether it is the design of products and services or the delivery mechanism — needs to be viewed in terms of the business opportunity that it offers and not as a deliverable that has been imposed on the service provider. However, it is also important to emphasize that commercial viability need not necessarily be viewed in terms of immediate cost and profitability calculations. Like in many other products, financial services also offer the prospect of a life-cycle model of marketing. Establishing a relationship with first-time consumers of financial products and services offers the opportunity to leverage this relationship into a wider set of financial transactions as at least some of these consumers move steadily up the income ladder. In fact, in a high growth scenario, a high proportion of such households are likely to move quite quickly from very basic financial services to more and more sophisticated ones. ln other words, the commercial viability and profitability of a financial inclusion strategy need not be viewed only from the perspective of immediacy. There is a viable investment dimension to it as well.

Which of the following statements is incorrect?

Solution

Option A is correct. It is mentioned in the last paragraph.

In fifth paragraph, the importance of savings account is mentioned. Therefore, option B is correct.

In second paragraph it is mentioned, 'The same concerns about lack of penetration amongst the lowest income group for loans also arise'. Option D is correct.

In second paragraph, author mentioned that savings account have low penetration amongst the lowest income group. This doesn't mean refer to below poverty line households only. Therefore, option C is incorrect.

The answer is option C.

Which of the following statements is correct?

Solution

In second paragraph it is mentioned that the process of financial inclusion is going to be incomplete and inadequate if it is measured only in terms of new accounts being opened and operated. This is the converse of the context made in option A. Therefore, option A is incorrect.

In last paragraph, it is mentioned "However, it is also important to emphasize that commercial viability need not necessarily be viewed in terms of immediate cost and profitability calculations". From this, we can infer that option C is incorrect.

From fifth paragraph, we can infer that option D is incorrect.

In third paragraph, it is mentioned "The fact that a huge proportion of the Indian workforce is either self- employed and in the casual labour segment suggests the need for products that will make access to credit easier to the former, while offering opportunities for risk mitigation and consumption smoothing to the latter." This implies option B is correct.

The answer is option B.

Identify the correct statement from the following:

Solution

In third paragraph, it is mentioned that casual labour needs risk mitigation products. Therefore, option A is incorrect. In second paragraph, it is mentioned that Rs. 50,000 per year in 2007, while perhaps not quite middle class, was certainly quite far above the official poverty line. This implies option B is incorrect. From fifth paragraph, we can infer that option C is incorrect. As mentioned in third paragraph, option D is correct.

The answer is option D.

Identify the wrong statement from the following:

Solution

In the fourth paragraph, it is mentioned, "Essentially, dealing with these kinds of expenditures requires a low-level systematic investment plan". This implies option A is correct. In the fifth paragraph, it is mentioned, "It is striking that the need to deal with emergencies, both financial and medical, plays such an important role in both sets of motivations." This implies that option C is correct. The point mentioned in option D can be inferred from the last paragraph of the passage.

In the last paragraph, it is mentioned, "In fact, in a high growth scenario, a high proportion of such households are likely to move quite quickly from very basic financial services to more and more sophisticated ones". Therefore, option B is incorrect.

The answer is option B.

Read the following passage carefully and answer the questions given at the end.

When Ratan Tata moved the Supreme Court, claiming his right to privacy had been violated, he called Harish Salve. The choice was not surprising. The former solicitor general had been topping the legal charts ever since he scripted a surprising win for Mukesh Ambani against his brother Anil. That dispute set the gold standard for legal fees. On Mukesh’s side were Salve, Rohinton Nariman, and Abhishek Manu Singhvi. The younger brother had an equally formidable line-up led by Ram Jethmalani and Mukul Rohatgi.

The dispute dated back three-and-a-half years to when Anil filed case against his brother for reneging on an agreement to supply 28 million cubic metres of gas per day from its Krishna-Godavari basin fields at a rate of $ 2.34 for 17 years. The average legal fee was Rs. 25 lakh for a full day's appearance, not to mention the overnight stays at Mumbai's five-star suites, business class travel, and on occasion, use of the private jet. Little wonder though that Salve agreed to take on Tata’s case pro bono. He could afford philanthropy with one of India’s wealthiest tycoons.

The lawyers’ fees alone, at a conservative estimate, must have cost the Ambanis at least Rs. 15 crore each. Both the brothers had booked their legal teams in the same hotel, first the Oberoi and, after the 26/ ll Mumbai attacks, the Trident. lt’s not the essentials as much as the frills that raise eyebrows. The veteran Jethmalani is surprisingly the most modest in his fees since he does not charge rates according to the strength of the client's purse. But as the crises have multiplied, lawyers‘fees have exploded.

The 50 court hearings in the Haldia Petrochemicals vs. the West Bengal Government cost the former a total of Rs. 25 crore in lawyer fees and the 20 hearings in the Bombay Mill Case, which dragged on for three years, cost the mill owners almost Rs. 10 crore. Large corporate firms, which engage star counsels on behalf of the client, also need to know their quirks. For instance, Salve will only accept the first brief. He will never be the second counsel in a case. Some lawyers prefer to be paid partly in cash but the best are content with cheques. Some expect the client not to blink while picking up a dinner tab of Rs. 1.75 lakh at a Chennai five star. A lawyer is known to carry his home linen and curtains with him while travelling on work. A firm may even have to pick up a hot Vertu phone of the moment or a Jaeger-LeCoutre watch of the hour to keep a lawyer in good humour.

Some are even paid to not appear at all for the other side - Aryama Sundaram was retained by Anil Ambani in the gas feud but he did not fight the case. Or take Raytheon when it was fighting the Jindals. Raytheon had paid seven top lawyers a retainer fee of Rs. 2.5 lakh each just to ensure that the Jindals would not be able to make a proper case on a taxation issue. They miscalculated when a star lawyer fought the case at the last minute. “I don’t take negative retainers”, shrugs Rohatgi, former additional solicitor general. “A Lawyer’s job is to appear for any client that comes to him. lt’s not for the lawyers to judge if a client is good or bad but the court”. Indeed. He is, after all, the lawyer who argued so famously in court that B. Ramalinga Raju did not ‘fudge any account in the Satyam Case. All he did was “window dressing”.

Some high profile cases have continued for years, providing a steady source of income, from the Scindia succession battle which dates to 1989, to the JetLite Sahara battle now in taxation arbitration to the BCCI which is currently in litigation with Lalit Modi, Rajasthan Royals and Kings XI Punjab.

Think of the large law firms as the big Hollywood studios and the senior counsel as the superstar. There are a few familiar faces to be found in most of the big ticket cases, whether it is the Ambani gas case, Vodafone taxation or Bombay Mills case. Explains Salve, “There is a reason why we have more than one senior advocate on a case. When you're arguing, he’s reading the court. He picks up a point or a vibe that you may have missed.” Says Rajan Karanjawala, whose firm has prepared the briefs for cases ranging from the Tata's recent right to privacy case to Karisma Kapoor’s divorce, “The four jewels in the crown today are Salve, Rohatgi, Rohinton Nariman and Singhvi. They have replaced the old guard of Fali Nariman, Soli Sorabjee, Ashok Desai and K.K. Venugopal.” He adds, “The one person who defies the generational gap is Jethmalani who was India's leading criminal lawyer in the 1960s and is so today.”

The demand for superstar lawyers has far outstripped the supply. So a one-man show by, say, Rohatgi can run up billings of Rs. 40 crore, the same as a mid-sized corporate law firm like Titus and Co that employs 28 juniors. The big law filik such as AZB or Amarchand & Mangaldas or Luthra & Luthra have to do all the groundwork for the counsel, from humouring the clerk to ensure the A-lister turns up on the hearing day to sourcing appropriate foreign judgments in emerging areas such as environmental and patent laws. “We are partners in this. There are so few lawyers and so many matters,” points out Diljeet Titus.

As the trust between individuals has broken down, governments have questioned corporates and corporates are questioning each other, and an array of new issues has come up. The courts have become stronger. “The lawyer,” says Sundaram, with the flourish that has seen him pick up many Dhurandhares and Senakas at pricey art auctions, “has emerged as the modern day purohit.” Each purohit is head priest of a particular style. Says Karanjawala, “Harish is the closest example in today's bar to Fali Nariman; Rohinton has the best law library in his brain; Mukul is easily India's busiest lawyer while Manu Singhvi is the greatest multi-tasker.” Salve has managed a fine balancing act where he has represented Mulayam Singh Yadav and Mayawati, Parkash Singh Badal and Amarinder Singh, Lalit Modi and Subhash Chandra and even the Ambani brothers, of course in different cases. Jethmalani is the man to call for anyone in trouble. In judicial circles he is known as the first resort for the last resort. Even Jethmalani’s junior Satish Maneshinde, who came to Mumbai in I993 as a penniless law graduate from Karnataka, shot to fame (and wealth) after he got bail for Sanjay Dutt in 1996. Now he owns a plush office in Worli and has become a one-stop shop for celebrities

in trouble.

Which of the following is not true about Ram Jethmalani?

Solution

To determine which statement about Ram Jethmalani is not true, we can evaluate the options against the passage. The passage confirms that Jethmalani is known in judicial circles as "the first resort for the last resort," making the option true.

It also describes him as "surprisingly the most modest in his fees" since he doesn’t adjust rates based on a client’s wealth, supporting option b.

Option c, stating he has been India’s leading criminal lawyer since the 1960s, aligns with the passage’s note that he was a top lawyer in the 1960s and remains so today.

However, option d, claiming "none of his juniors have done well in their careers," is false because the passage highlights Satish Maneshinde, a junior of Jethmalani, who achieved fame and wealth after securing bail for Sanjay Dutt and now owns a plush office in Worli.

Since the question asks which statement is invalid, option d is contradicted by this evidence, while the others are supported; the answer is d. In short, option d is not true because at least one of Jethmalani’s juniors succeeded, contrary to the claim of "none."

Match the following:

Solution

In the 2nd last paragraph it is given that "Harish is the closest example in today's bar to Fali Nariman"

Thus, a-ii

In the last paragraph it is given that "Rohinton has the best law library in his brain"

Thus, b-iv

Hence, a-i and b-iv

The only option that captures this is option B.

Hence, option B is the correct answer.

What does a ‘negative retainer’ refer to?

Solution

From fifth paragraph, we can understand that a negative retainer is the one who pays a lawyer not to fight a case for the other side. The answer is option B.

What does the phrase ‘pro bono’ mean?

Solution

From second paragraph, we can infer that pro bono refers to a service to serve a public good. From the given options, option B is the appropriate one. The answer is option B.

Read the following passage carefully and answer the questions given at the end.

The second issue I want to address is one that comes up frequently - that Indian banks should aim to become global. Most people who put forward this view have not thought through the costs and benefits analytically; they only see this as an aspiration consistent with India’s growing international profile. In its 1998 report, the Narasimham (II) Committee envisaged a three tier structure for the Indian banking sector: 3 or 4 large banks having an international presence on the top, 8-10 mid-sized banks, with a network of branches throughout the country and engaged in universal banking, in the middle, and local banks and regional rural banks operating in smaller regions forming the bottom layer. However, the Indian banking system has not consolidated in the manner envisioned by the Narasimham Committee. The current structure is that India has 81 scheduled commercial banks of which 26 are public sector banks, 21 are private sector banks and 34 are foreign banks. Even a quick review would reveal that there is no segmentation in the banking structure along the lines of Narasimham II.

A natural sequel to this issue of the envisaged structure of the Indian banking system is the Reserve Bank’s position on bank consolidation. Our view on bank consolidation is that the process should be market-driven, based on profitability considerations and brought about through a process of mergers & amalgamations (M&As;). The initiative for this has to come from the boards of the banks concerned which have to make a decision based on a judgment of the synergies involved in the business models and the compatibility of the business cultures. The Reserve Bank’s role in the reorganisation of the banking system will normally be only that of a facilitator.

lt should be noted though that bank consolidation through mergers is not always a totally benign option. On the positive side are a higher exposure threshold, international acceptance and recognition, improved risk management and improvement in financials due to economies of scale and scope. This can be achieved both through organic and inorganic growth. On the negative side, experience shows that consolidation would fail if there are no synergies in the business models and there is no compatibility in the business cultures and technology platforms of the merging banks.

Having given that broad brush position on bank consolidation let me address two specific questions: (i) can Indian banks aspire to global size?; and (ii) should Indian banks aspire to global size? On the first question, as per the current global league tables based on the size of assets, our largest bank, the State Bank of India (SBI), together with its subsidiaries, comes in at No.74 followed by ICICI Bank at No. I45 and Bank of Baroda at 188. It is, therefore, unlikely that any of our banks will jump into the top ten of the global league even after reasonable consolidation.

Then comes the next question of whether Indian banks should become global. Opinion on this is divided. Those who argue that we must go global contend that the issue is not so much the size of our banks in global rankings but of Indian banks having a strong enough, global presence. The main argument is that the increasing global size and influence of Indian corporates warrant a corresponding increase in the global footprint of Indian banks. The opposing view is that Indian banks should look inwards rather than outwards, focus their efforts on financial deepening at home rather than aspiring to global size.

It is possible to take a middle path and argue that looking outwards towards increased global presence and looking inwards towards deeper financial penetration are not mutually exclusive; it should be possible to aim for both. With the onset of the global financial crisis, there has definitely been a pause to the rapid expansion overseas of our banks. Nevertheless, notwithstanding the risks involved, it will be opportune for some of our larger banks to be looking out for opportunities for consolidation both organically and inorganically. They should look out more actively in regions which hold out a promise of attractive acquisitions.

The surmise, therefore, is that Indian banks should increase their global footprint opportunistically even if they do not get to the top of the league table.

Identify the correct statement from the following:

Solution

In the first paragraph, it is mentioned that there is no segmentation in the Indian banking structure along the lines of Narasimham II. Therefore, Option C is the correct statement.

Option A: There is no mention of large banks that have an international presence should not be engaged in universal banking.

Option B mentions that "all banks should become global," which is too extreme. Therefore, it is incorrect.

Option D: RBI's role would be that of a facilitator in the reorganisation of the banking system, not consolidation of a banking system. Therefore, it is incorrect.

Identify the correct statement from the following:

Solution

In fourth paragraph, it is mentioned, "It is unlikely that any of our banks will jump into the top ten of the global league even after reasonable consolidation." This implies, option C is incorrect. The point mentioned in option B is nowhere mentioned or inferred from the given passage.

Option D is correct. This can be inferred from second last paragraph - "They should look out more actively in regions which hold out a promise of attractive acquisitions."

The answer is option D.

Identify the wrong statement from the following:

Solution

In fourth paragraph, it is mentioned that banks SBI, ICICI and Bank of Baroda are in top 200 of the global league. This implies option C is incorrect.

The answer is option C.

Each sentence below has four underlined words or phrases, marked A, B, C and D. Identify the underlined part that must be change to make the sentence correct.

Neither the examiner (A) nor his assistant (B) were informed (C) about the cancellation of the examination. No Error (D).

Solution

The verb following neither-nor is according to the nearest subject. In the given sentence, 'assistant' is singular. So, 'were' is incorrect. It should be 'was'.

Hence, option C is the correct answer.

Being (A) a short holiday (B) we had to return (C) without visiting many of the places (D)

Solution

The sentence should have a subject which is missing in this case.

Thus, In 'A' there should be some subject like 'it' which is missing.

Hence, option A is incorrect.

Hence, option A is the correct answer.

Each question below consists of an incomplete sentence. Four words or pharses marked A, B, C and D are given beneath each sentence. Mark the option that best completes the sentence.

____________made after English settlers came to Jamestown was a map of Virginia by john Smith, the famous adventurer.

Solution

Among the given options, option B provides the correct start.

The answer is option B.

The concept this weekend promises to attract ___________ than attended the last one.

Solution

The adverb 'even' should be used as there is a comparison happening with last time. Among the given options, option D is the appropriate one.

The answer is option D.

In the question below, there are two sentences containing underlined homonyms, which may either be mis –spelt or inappropriately used in the context of the sentence. Select the appropriate answer from the option given below:

I. A vote of censur was passed against the Chairman.

II. Before release, every film is passed by the Censor Board.

Solution

Only sentence II is correct.

Sentence I is incorrect.

Correct sentence: A vote of censure was passed against the Chairman.

The answer is option B.

I. This behaviour does not compliment his position.

II. He thanked his boss for the complement.

Solution

Complement - adding value, Compliment - praising someone

Sentences I and II are incorrect.

Sentence I - This behaviour does not complement his position.

Sentence II - He thanked his boss for the compliment.

The answer is option D.

For each of the following sentences, choose the most appropriate “one word” for the given expressions.

One who is unrelenting and cannot be moved by entreaties :

Solution

The correct word is inexorable.

Inexorable - impossible to persuade

The answer is option A.

The art of cutting trees and bushes into ornamental shapes:

Solution

Topiary - the art or practice of clipping shrubs or trees into ornamental shapes.

The answer is option D.

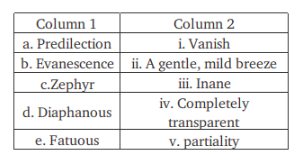

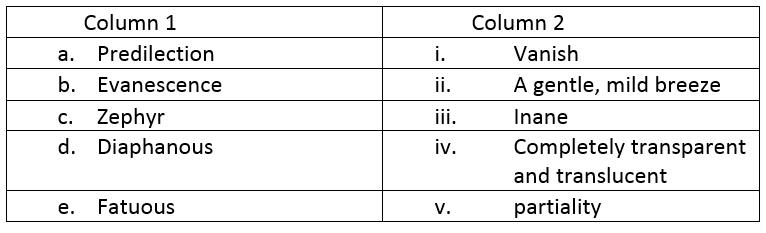

Match the words in column 1 with their appropriate meaning in column 2.

Solution

Predilection means a preference or special liking for something; a bias in favour of something.

Evanescence means the rapid fading from sight or memory of that person. , or the rapid fading from sight or memory of that person.

Zephyr means a soft gentle breeze.

Diaphanous means light, delicate, and translucent.

Fatuous means silly and pointless.

Hence, option C is the correct answer.

Solution

Perspicacity - the quality of having a ready insight into things; shrewdness.

Uxorious - having or showing a great or excessive fondness for one's wife.

Nebbish - a person, especially a man, who is regarded as pitifully ineffectual, timid, or submissive.

Chicanery - the use of deception or subterfuge to achieve one's purpose.

Inchoate - just begun and so not fully formed or developed; rudimentary.

Hence, option B is the correct answer.

Identify antonyms for the following words.

Risible:

Solution

Risible means provoking laughter through being ludicrous. Therefore, 'serious' is a perfect antonym for the world 'Rising'.

Therefore, option A is the correct answer.

Tenebrous:

Solution

Tenebrous means dark; shadowy or obscure. Therefore, 'bright' is a perfect antonym for the world 'Tenebrous'.

Therefore, option C is the correct answer.

A partially completed paragraph is below, followed by fillers a,b,c. From options A, B, C and D, identify the right combination and order of fillers a,b or c that will best complete the paragraph.

In cultivating team spirit, one should not forget the importance of discipline. _________________ It is the duty of all the numbers of the team to observe discipline in its proper perspective.

a. A proper team spirit can seldom be based on discipline.

b.It is a well known fact that team spirit and discipline can never go hand in hand

c. Discipline in its right perspective would mean sacrificing self to some extent.

Solution

Statements a and b are incorrect as both are contrary to the given context. Only option C is in line with the context.

The answer is option D.

Forests are gifts of nature __________. Yet, with the spread of civilisation, man has not only spurned the forests, but has been ruthlessly destroying them.

a. It is on historical record that the vast sahara desert of today once used to be full of thick forests.

b. A large part of humanity still lives deep inside forests, particularly in the tropical regions of the earth.

c. Human evolution itself has taken place in the forests.

Solution

Statement (a) mentions something which is out of the given context. Statements (c) and (b) in the order will complete the paragraph.

The answer is option C.

For the following questions answer them individually

Given below are the first and last parts of a sentence, and the remaining sentence is broken into four parts p, q, r and s. From A, B, C and D, choose the arrangement of these parts that forms a complete, meaningful sentence.

A number of measures ______________ of the Municipal Corporations.

p.The financial conditions.

q. For mobilisation of resources

r. In order to improve

s. Are being taken by the State Governments

Solution

A number of measure is logically followed by Are being taken by the State Governments.

s is followed by q as it explains the reason for taking the measures.

r follows q as it further explains the reason for taking the measures.

p follows r as p states what is being improved which is given in r

Thus, the correct order is sqrp.

Which of the following cannot be termed as an ‘oxymoron’?

Solution

oxymoron means a figure of speech in which apparently contradictory terms appear in conjunction. A living death, conspicuous by one’s absence and deafening silence are examples of oxymoron. Hence, we can say that option B is the correct answer.

In the following question, the options 1, 2, 3 and 4 have a word written in four different ways, of which only one is correct. Identify the correctly spelt word.

Solution

'Septuagenarian' is the correct spelling which means a person who is between 70 and 79 years old. Hence, option D is the correct answer.

In the following question, a sentence has been broken up into parts, and the parts have been scrambled and numbered. Choose the correct order of these parts from the alternatives 1, 2, 3 and 4.

a. food supply

b. storage, distribution and handling

c. pastoral industry and fishing

d. besides increasing

e. by preventing wastage in

f. the productivity from agriculture

g. can be increased

Solution

The correct sentence would be: Besides increasing the productivity from agriculture, pastol industry and fishing. Food supply can be increased by preventing wastage in storage, distribution and handling. The answer is option C.

Option A: In this one ,D-C-F would form "besides increasing pastoral industry and fishing the productivity from agriculture" doesn't make coherent sense.

Option B: This would form "Besides increasing food supply the productivity from agriculture can be increased by preventing wastage in pastoral industry and fishing, storage, distribution and handling" . This statement lacks the logical flow where the sentence talks about other than productivity from agriculture, the food supply could be increased by reducing wastage.

Option D:In this sequence, F-C-E would give "the productivity from agriculture pastoral industry and fishing by preventing wastage in" does not form a coherent sentence, so this option is eliminated.

Arrange the following letters to form a meaningful word.

Solution

OVERHEAD is the word that can be formed from the given letters.

Hence, option C is the correct answer.

Solution

The word is Competitor.

Hence, option B is the correct answer.

In each of the following question a sentence is given in “Direct Speech “Identify the right alternative 1 2 3 and 4 which best expresses this sentence in “Indirect Speech”.

He said to her, “Are you coming to the party?”

Solution

Present tense -> past tense

Indirect speech - He asked her whether she was coming to the party.

The answer is option A.

The teacher said, “Be quiet, boys.”

Solution

Indirect speech - The teacher urged the boys to be quiet.

The answer is option C.

For the following questions answer them individually

Match the Latin phrases in column 1 with their appropriate meaning in column 2:

Solution

Predilection means a preference or special liking for something; a bias in favour of something.

Evanescence means the rapid fading from sight or memory of that person. , or the rapid fading from sight or memory of that person.

Zephyr means a soft gentle breeze.

Diaphanous means light, delicate, and translucent.

Fatuous means silly and pointless.

Hence, option C is the correct answer.

Mandeep and Jagdeep had gone to visit Ranpur, which is a seaside town and also known for the presence of the historical ruins of an ancient kingdom. They stayed in a hotel which is exactly 250 meters away from the railway station. At the hotel, Mandeep and Jagdeep learnt from a tourist information booklet that the distance between the sea-beach and the gate of the historical ruins is exactly 1 km. Next morning they visited the sea-beach to witness sunrise and afterwards decided to have a race from the beach to the gate of the ruins. Jagdeep defeated Mandeep in the race by 60 meters or 12 seconds. The following morning they had another round of race from the railway station to the hotel. How long did Jagdeep take to cover the distance on the second day?

Solution

Jagdeep defeated Mandeep in a 1 km race by 60 m or 12 seconds.

Therefore, Mandeep can cover 60 m in 12 seconds

Speed of Mandeep = 5 m/s

Time taken by Mandeep to cover 1 km or 1000 m = 200 s

Time taken by Jagdeep to cover 1000 m = (200 - 12) = 188 s

Time taken by Jagdeep to cover 250 m = 47 s

Hence, option B is the correct answer.

Sujoy, Mritunjoy and Paranjoy are three friends, who have worked in software firms Z Solutions, G Software’s and R Mindpower respectively for decade. The friends decided to float a new software firm named XY Infotech in January 2010. However, due to certain compulsions, Mritunjoy and Paranjoy were not able to immediately join the start-up in the appointed time. It was decided between friends that Sujoy will be running the venture as the full time director during 2010, and Mritunjoy and Paranjoy will be able to join the business only in January 2011. In order to compensate Sujoy for his efforts, it was decied that he will receive 10 percent of the profits and in the first year will invest lesser amount as compared to his friends. The remaining profit will be distributed among the friends in line with their contribution. Sujoy invested Rs. 35,000/- for 12 months, Mritunjoy invested Rs. 1,30,000/- for 6 months and Paranjoy invested Rs. 75,000/- for 8 months. If the total profit earned during 2010 was Rs. 4,50,000/-, then Paranjoy earned a profit of:

Solution

Total profit = Rs. 450000

Sujoy will get 10% of this.

So, the profit to be distributed = Rs. 405000

Sujoy's investment = 12 * Rs. 35000 = Rs. 420000

Mritunjoy's investment = 6 * Rs. 130000 = Rs.780000

Paranjoy's investment = 8 * Rs. 75000 = Rs. Rs. 600000

Paranjoy's share in profit = Rs. $$\dfrac{600000}{420000 + 780000 + 600000}$$ * 405000 = Rs. 135000

Hence, option B is the correct answer.

In Bilaspur village, 12 men and 18 boys completed construction of a primary health center in 60 days, by working for 7.5 hours a day. Subsequently the residents of the neighbouring Harigarh village also decided to construct a primary health center in their locality, which would be twice the size of the facility build in Bilaspur. If a man is able to perform the work equal to the same done by 2 boys, then how many boys will be required to help 21 men to complete the work in Harigarh in 50 days, working 9 hours a day?

Solution

It is given that a man is able to perform the work equal to the same done by 2 boys. Hence, we can assume that In Bilaspur village 21=(12+18/2) men completed construction of a primary health center in 60 days, by working for 7.5 hours a day.

Hence, total men hours required to completed the primary health center in Bilaspur = 7.5*21*60 = 9450.

Let us assume that 'n' be the number of boys required to help 21 men to complete the work in Harigarh in 50 days by working 9 hours a day.

Therefore, we can say that

$$\Rightarrow$$ 2*9450 = 50*9*(21+t/2)

$$\Rightarrow$$ 42 = 21+t/2

$$\Rightarrow$$ t = 42

Hence, option D is the correct answer.

$$(\sqrt{\frac{225}{729}}-\sqrt{\frac{25}{144}})\div\sqrt{\frac{16}{81}}=?$$

Solution

$$(\sqrt{\frac{225}{729}}-\sqrt{\frac{25}{144}})\div\sqrt{\frac{16}{81}}=x$$ This can be simplified as

$$(\frac{15}{27}-\frac{5}{12})\div\frac{4}{9}=x$$

$$(\frac{5}{36})*\frac{9}{4}=x$$

x=$$\frac{5}{16}$$. Hence, option A is the correct answer.

If $$\frac{x}{y}=\frac{7}{4}$$, find the value of $$\frac{x^{2}-y^{2}}{x^{2}+y^{2}}$$

Solution

Given that If $$\frac{x}{y}=\frac{7}{4}$$

Therefore, $$(\frac{x}{y})^2=\frac{49}{16}$$ ... (1)

$$\dfrac{x^{2}-y^{2}}{x^{2}+y^{2}}$$ this can be written as,

$$\Rightarrow$$ $$\dfrac{(\frac{x}{y})^2-1}{(\frac{x}{y})^2+1}$$

$$\Rightarrow$$ $$\dfrac{\frac{49}{16}-1}{\frac{49}{16}+1}$$

$$\Rightarrow$$ $$\dfrac{49-16}{49+16}$$

$$\Rightarrow$$ $$\dfrac{33}{65}$$

Hence, option C is the correct answer.

While preparing for a management entrance examination Romit attempted to solve three paper, namely Mathematics, Verbal English and Logical Analysis, each of which have the full marks of 100. It is observed that one-third of the marks obtained by Romit in Logical Analysis is greater than half of his marks obtained in Verbal English By 5. He has obtained a total of 210 marks in the examination and 70 marks in Mathematics. What is the difference between the marks obtained by him in Mathematics and Verbal English?

Solution

Let 'a' and 'b' be the marks obtained by Romit in Verbal English and Logical Analysis respectively. It is given that,

a + b + 70 = 210

a + b = 140. ... (1)

It is observed that one-third of the marks obtained by Romit in Logical Analysis is greater than half of his marks obtained in Verbal English By 5.

$$\dfrac{b}{3} - \dfrac{a}{2} = 5$$

$$2b - 3a = 30$$ ... (2)

On solving equation (1) and (2) we get b = 90 and a = 50.

Hence, the difference between the marks obtained by him in Mathematics and Verbal English = 70 - 50 = 20.

Therefore, option C is the correct answer.

Aniket and Animesh are two colleagues working in PQ Communications, and each of them earned an investible surplus of Rs. 1, 50, 000/- during a certain period. While Animesh is a risk-averse person, Aniket prefers to go for higher return opportunities. Animesh uses his entire savings in Public Provident Fund (PPF) and National Saving Certificates (NSC). It is observed that one-third of the savings made by Animesh in PPF is equal to one-half of his savings in NSC. On the other hand, Aniket distributes his investible funds in share market, NSC and PPF. It is observed that his investments in share market exceeds his savings in NSC and PPF by Rs. 20,000/- and Rs. 40,000/- respectively. The difference between the amount invested in NSC by Animesh and Aniket is:

Solution

Let 'x' be the amount invested by Aniket in share market. Therefore, amount invested by him in NSC and PPF will be 'x-20000' and 'x-40000' respectively.

It is given that, x + x-20000 + x-40000 = 150000

$$\Rightarrow$$ x = 70000.

Hence, the amount invested by Aniket in NSC = x - 20000 = 50000.

It is given that one-third of the savings made by Animesh in PPF is equal to one-half of his savings in NSC.

Let 'y' be the amount invested by Animesh in NSC. Then we can say that he invested '150000-y' in PPF.

$$\Rightarrow$$ $$\dfrac{150000-y}{3} = \dfrac{y}{2}$$

$$\Rightarrow$$ $$300000-2y = 3y$$

$$\Rightarrow$$ $$y = 60000$$

Therefore, the difference between the amount invested in NSC by Animesh and Aniket = 60000 - 50000 = Rs. 10000. Hence, option D is the correct answer.

In March 2011, EF Public Library purchased a total of 15 new books published in 2010 with a total expenditure of Rs. 4500. Of these books, 13 books were purchased from MN Distributors, while the remaining two were purchased from UV Publishers. It is observed that one-sixth of the average price of all the 15 books purchased is equal to one-fifth of the average price of the 13 books obtained from MN Distributors. Of the two books obtained from UV Publishers, if one-third of the price of one volume is equal to one-half of the price of the other, then the price of the two books are:

Solution

Let 'x' and 'y' be the average price of 13 books obtained from MN Distributors and remaining 2 books purchased from UV Publishers respectively.

It is given that he spent a total of Rs. 4500. Therefore,

13x + 2y = 4500 ... (1)

It is also observed that one-sixth of the average price of all the 15 books purchased is equal to one-fifth of the average price of the 13 books obtained from MN Distributors.

$$\dfrac{4500/15}{6} = \dfrac{x}{5}$$

$$x = 250$$ ... (2)

Form equation (1) and (2) we can say that 2y = 1250.

Let 'a' and 'b' be the price of two books purchased from UV Publishers. It is given that one-third of the price of one volume is equal to one-half of the price of the other.

Therefore, $$\dfrac{a}{3} = \dfrac{b}{2}$$ ... (3)

Also, $$2y = 1250 = a + b$$ ... (4)

From, equation (3) and (4) we can say that a = 750 and b = 500. Hence, option C is the correct answer.

2 years ago, one-fifth of Amita’s age was equal to one-fourth of the age of Sumita, and the average of their age was 27 years. If the age of Paramita is also considered, the average age of three of them declines to 24. What will be the average age of Sumita and Paramita 3 years from now?

Solution

Let 'A', 'S' and 'P' be Amita's, Sumita's and Paramita's present age.

It is given that 2 years ago, one-fifth of Amita’s age was equal to one-fourth of the age of Sumita, and the average of their age was 27 years.

$$\dfrac{(A-2)+(S-2)}{2} = 27$$

$$A+S = 58$$ ... (1)

Also, $$\dfrac{A-2}{5} = \dfrac{S-2}{4}$$

$$4A-8 = 5S-10$$

$$5S - 4A = 2$$ ... (2)

From equation (1) and (2) we can say that S = 26, A = 32.

Average age of Amita, Sumita and Paramita before 2 years = 24.

$$\dfrac{(A-2)+(S-2)+(P-2)}{3} = 24$$

$$A+S+P = 78$$. Hence, P = 20.

Therefore, the average age of Sumita and Paramita 3 years from now? = $$\dfrac{(S+3)+(P+3)}{2}$$ = $$\dfrac{(26+3)+(20+3)}{2}$$ = 26 years.

Hence, option B is the correct answer.

An old lady engaged a domestic help on the condition that she would pay him Rs. 90 and a gift after service of one year. He served only 9 months and received the gift and Rs. 65. Find the value of the gift.

Solution

Let 'G' be the value of the gift. Hence, the monthly salary of domestic help = $$\dfrac{90+G}{12}$$.

Therefore, $$9*\dfrac{90+G}{12} = G+65$$

$$3G = 30$$. Hence, G = Rs. 10.

There are four prime numbers written in ascending order of magnitude. The product of the first three is 7429 and last three is 12673. Find the first number.

Solution

Let 'a', 'b', 'c' and 'd' be the prime number in ascending order. The product of the first three is 7429 and last three is 12673. Find the first number.

Given that $$a*b*c = 7429$$ and $$b*c*d = 12673$$

Therefore, $$\dfrac{b*c*d}{a*b*c} = \dfrac{12673}{7429}$$

$$\Rightarrow$$ $$\dfrac{d}{a} = \dfrac{29}{17}$$

Since a and d are prime number there won't be any common factor which can divide both. Hence, a = 17, b = 19, c = 23 and d = 29.

Therefore, option B is the correct answer.

A rectangular piece of paper is 22 cm. long and 10 cm. wide. A cylinder is formed by rolling the paper along its length. Find the volume of the cylinder.

Solution

When the paper is rolled along its length, the circumference of the cylinder formed is equal to the length and the height is equal to the breadth of the rectangle.

Let 'r' be the radius and 'h' be the height of the cylinder formed.

$$2\pi*r = 22$$ and h = 10

Hence, the volume of the cylinder = $$\pi*r^2*h$$ = $$\dfrac{22}{7}*(7/2)^2*10$$ = 385 $$cm^3$$.

Find the value of x from the following equation:

$$\log_{10}{3}+\log_{10}(4x+1)=\log_{10}(x+1)+1$$

Solution

$$\log_{10}{3}+\log_{10}(4x+1)=\log_{10}(x+1)+1$$ can be written as

$$\log_{10}{3}+\log_{10}(4x+1)=\log_{10}(x+1)+\log_{10}{10}$$

We know that $$\log_{10}{a}+\log_{10}{b}=\log_{10}{ab}$$

$$\log_{10}{3*(4x+1)}=\log_{10}{(x+1)*10}$$

$$12x+3=10x+10$$

$$x=7/2$$. Hence, option B is the correct answer.

Consider the volumes of the following objects and arrange them in decreasing order:

i. A parallelepiped of length 5 cm, breadth 3 cm and height 4 cm

ii. A cube of each side 4 cm.

iii. A cylinder of radius 3 cm and length 3 cm

iv. A sphere of radius 3 cm

Solution

i. Volume of the parallelepiped of length 5 cm, breadth 3 cm and height 4 cm = 3*4*5 = 60 cm$$^3$$

ii. Volume of the cube of each side 4 cm = 4^3 = 64 cm$$^3$$

iii.Volume of the cylinder of radius 3 cm and length 3 cm = $$\pi*3^2*3$$ = 84.82 cm$$^3$$

iv. Volume of the sphere of radius 3 cm = $$4/3*\pi*3^3$$ = 113.09 cm$$^3$$

Therefore, we can say that volumes of the objects in decreasing order = iv,iii,ii,i.

Hence, option A is the correct answer.

If x satisfies the inequality $$|x - 1| + |x - 2| + |x - 3| \geq 6$$, then:

Solution

Given that $$|x - 1| + |x - 2| + |x - 3| \geq 6$$.

Case 1: When x > 3

$$(x - 1) + (x - 2) + (x - 3) \geq 6$$

$$x \geq 4$$

Therefore, the value of x $$\in$$ [4, $$\infty$$)

Case 2: When 2 < x < 3

$$(x - 1) + (x - 2) - (x - 3) \geq 6$$

$$x \geq 6$$

Therefore, no possible value of x in this domain.

Case 3: When 1 < x < 2

$$(x - 1) - (x - 2) - (x - 3) \geq 6$$

$$x \leq -2$$

Therefore, no possible value of x in this domain.

Case 3: When x < 1

$$-(x - 1) - (x - 2) - (x - 3) \geq 6$$

$$x \leq 0$$

Therefore, the value of x $$\in$$ (-$$\infty$$, 0]

Therefore, the value of x that will satisfy this inequality: x $$\in$$ (-$$\infty$$, 0] $$\cup$$ [4, $$\infty$$).

Hence, option B is the correct answer.

A five digit number divisible by 3 is to be formed using the numerals 0, 1, 2, 3, 4 and 5 without repetition. The total number of ways in which this can be done is:

Solution

For a number to be divisible by 3, the sum of it's digit should be a multiple of 3. This can be done in two ways. When the number are formed by using either {1, 2, 3, 4, 5} or {0, 1, 2, 4, 5}.

Total 5 digit numbers that can be formed by {1, 2, 3, 4, 5} without repetition = 5*4*3*2*1 = 120

Total 5 digit numbers that can be formed by {0, 1, 2, 4, 5} without repetition = 4*4*3*2*1 = 96

Therefore, total such number = 120 + 96 = 216. Hence, option D is the correct answer.

If 2, a, b, c, d, e, f and 65 form an arithmetic progression, find out the value of ‘e’.

Solution

Given that 2, a, b, c, d, e, f and 65 are in an AP.

65 = 2 + (8-1)d

d = 9.

Therefore, e = 2+(6-1)*9 = 2+45 = 47. Therefore, option B is the correct answer.

A contract is to be completed in 56 days and 104 men are set to work. Each working 8 hours a day, after 30 days, 2/5th of the work is finished. How many additional men may be employed so that work may be completed on time, each man now working 9 hours per day?

Solution

Let 'W' be the amount of work. It is given that,

$$\dfrac{2}{5}*W = 104*8*30$$ ... (1)

Let 'X' be the number of additional men required to finish the work on time.

$$W - \dfrac{2}{5}*W = (104+x)*9*(56-30)$$ ... (2)

By equation (1) and (2) we can say that,

$$\dfrac{2}{3} = \dfrac{104*8*30}{(104+x)*9*(56-30)}$$

$$\Rightarrow$$ $$(104+x)*9*26 = 12*104*30$$

$$\Rightarrow$$ $$(104+x)=160$$

$$\Rightarrow$$ $$x=56$$.

Hence, option A is the correct answer.

A bag contains 8 red and 6 blue balls. If 5 balls are drawn at random, what is the probability that 3 of them are red and 2 are blue?

Solution

5 balls are drawn at random, hence the probability that 3 of them are red and 2 are blue = $$\dfrac{8c3*6c2}{14c5}$$ = $$\dfrac{60}{143}$$

Hence, option D is the correct answer.

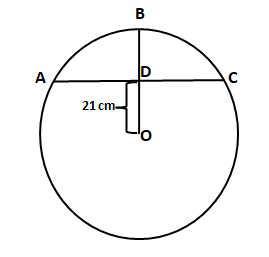

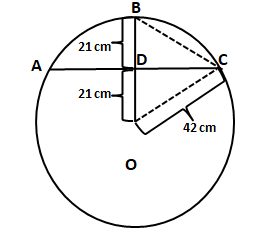

In a circle, the height of an arc is 21 cm and the diameter is 84 cm. Find the chord of ‘half of the arc’

Solution

Let ABC be the arc as shown in the figure. It is known that the diameter of the circle = 84 cm. Hence, the radius of the circle = 42 cm.

We can see that both CO and BO are equivalent to the radius of the circle. Hence, CO = 42 cm and BD = BO - OD = 42 - 21 = 21 cm.

In triangle ODC, $$cosDOC = \dfrac{21}{42}$$

Hence, $$\angle$$ DOC = 60°

In triangle BOC, OB = OC. Hence, we can say that $$\angle$$ OCB = $$\angle$$ OBC = 60°.

Therefore, OBC is an equilateral triangle. Hence, OB = OC = BC = 42 cm.

Hence, we can say that the length of the chord of ‘half of the arc’ = 42 cm. Therefore, option C is the correct answer.

Mr. and Mrs. Gupta have three children - Pratik, Writtik and Kajol, all of whom were born in different cities. Pratik is 2 years elder to Writtik. Mr. Gupta was 30 years of age when Kajol was born in Hyderabad, while Mrs. Gupta was 28 years of age when Writtik was born in Bangalore. If Kajol was 5 years of age when Pratik was born in Mumbai, then what were the ages of Mr. and Mrs. Gupta respectively at the time of Pratik’s birth?

Solution

Mr. and Mrs. Gupta have three children - Pratik, Writtik and Kajol, all of whom were born in different cities. Pratik is 2 years elder to Writtik. Mr. Gupta was 30 years of age when Kajol was born in Hyderabad, while Mrs. Gupta was 28 years of age when Writtik was born in Bangalore. If Kajol was 5 years of age when Pratik was born in Mumbai, then what were the ages of Mr. and Mrs. Gupta respectively at the time of Pratik’s birth.

It is given that Pratik is 2 years elder to Writtik and Kajol was 5 years of age when Pratik was born in Mumbai. Hence, we can say that Kajol is the eldest and Writtik is the youngest.

Mrs. Gupta was 28 years of age when Writtik was born in Bangalore. Hence, at the time of Pratik's birth Mrs. Gupta would have been two years younger i.e. 28 - 2 = 26 years old.

Mr. Gupta was 30 years of age when Kajol was born. Hence, at the time of Pratik's birth Mr. Gupta would have been 5 years older i.e. 30 + 5 = 35 years old.

Hence, option A is the correct answer.

Mr. Sinha received a certain amount of money by winning a lottery contest. He purchased a new vehicle with 40 percent of the money received. He then gave 20 percent of the remaining amount to each of his two sons for investing in their business. Thereafter, Mr. Sinha spent half of the remaining amount for renovation of his house. One-fourth of the remaining amount was then used for purchasing a LCD TV and the remaining amount - Rs. 1,35,000/- was deposited in a bank. What was the amount of his cash prize?

Solution

He purchased a new vehicle with 40 percent of the money received. He then gave 20 percent of the remaining amount to each of his two sons for investing in their business. Thereafter, Mr. Sinha spent half of the remaining amount for renovation of his house. One-fourth of the remaining amount was then used for purchasing a LCD TV and the remaining amount - Rs. 1,35,000/- was deposited in a bank. What was the amount of his cash prize?

Let '100x' be the amount won by Mr. Sinha in the lottery contest.

The amount left with him after purchasing the new vehicle = 0.60*100x = 60x.

The amount left with him after distributing his two sons for investing in their business = (1-2*0.20)*60x = 36x.

The amount left with him after renovating his house = 0.50*36x = 18x.

The amount left with him after purchasing the LCD TV = 0.75*18x = 13.5x.

It is given that, 13.5x = 135000

Therefore, 100x = 10,00,000. Hence, option A is the correct answer.

The ratio of number of male and female journalists in a newspaper office is 5:4. The newspaper has two sections, political and sports. If 30 percent of the male journalists and 40 percent of the female journalists are covering political news, what percentage of the journalists (approx.) in the newspaper is currently involved in sports reporting?

Solution

The ratio of number of male and female journalists in a newspaper office is 5:4. The newspaper has two sections, political and sports. If 30 percent of the male journalists and 40 percent of the female journalists are covering political news, what percentage of the journalists (approx.) in the newspaper is currently involved in sports reporting?

Let '9x' be the number of total journalists in the office. Then, we can say that the number of male and female journalists are '5x' and '4x' respectively.

It is given that 30 percent of the male journalists and 40 percent of the female journalists are covering political news. Hence, total number of journalists who are covering political news = 0.3*5x + 0.4*4x = 3.1x

Therefore, the total number journalists who are covering sports news = 9x - 3.1x = 5.9x.

Hence, the percentage of the journalists in the newspaper is currently involved in sports reporting = $$\dfrac{5.9x}{9x}\times 100$$ $$\approx$$ 65 percent. Therefore, option A is the correct answer.

The ratio of ‘metal 1’ and ‘metal 2’ in alloy ‘A’ is 3 :4. In alloy ‘B’ same metals are mixed in the ratio 5:8. If 26 kg of alloy ‘B’ and 14 kg of alloy ‘A’ are mixed then find out the ratio of ‘metal 1’ and ‘metal 2’ in the new alloy.

Solution

The ratio of ‘metal 1’ and ‘metal 2’ in alloy ‘A’ is 3 :4.Therefore, we can say that 14 kg of alloy 'A' will contain $$\dfrac{3}{7} 14$$ = 6 kg of 'metal 1' and $$\dfrac{4}{7} 14$$ = 8 kg of 'metal 2'.

The ratio of ‘metal 1’ and ‘metal 2’ in alloy ‘B’ is 5 :8.Therefore, we can say that 26 kg of alloy 'B' will contain $$\dfrac{5}{13} 26$$ = 10 kg of 'metal 1' and $$\dfrac{8}{13} 26$$ = 16 kg of 'metal 2'.

Hence, total weight of 'metal 1' in the new alloy = 6 + 10 = 16 kg

Total weight of 'metal 2' in the new alloy = 8 + 16 = 24 kg

Therefore, the ratio of ‘metal 1’ and ‘metal 2’ in the new alloy. = 16 : 24 = 2 :3. Hence, option C is the correct answer.

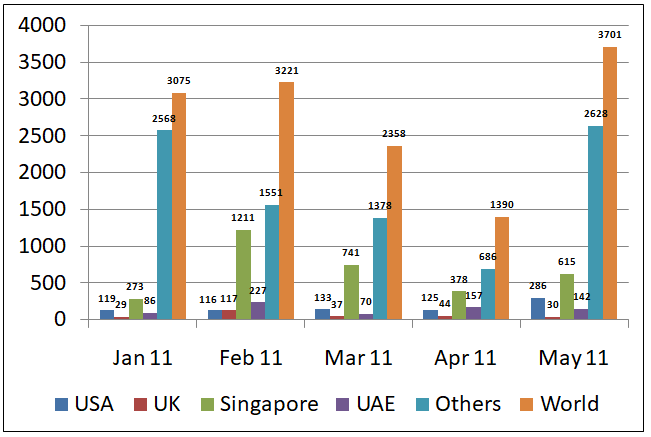

Answer the following questions based on the Diagram below, which reports Country XX’s monthly Outward Investment flows to various countries and the World. The FDI figures are reported US$ Million.

What is the compound average growth rate of Country XX’s overall Outward Investment during the period January 2011 and May 2011?

Solution

Total outward investment flows

The compound average growth rate of Country XX’s overall Outward Investment during the period January 2011 and May 2011 = $$[({\dfrac{3701}{3075}})^{0.25} - 1]\times 100$$ = 4.74 percent.

Hence, option D is the correct answer.

In which month Country XX’s Outward Investment to Singapore dropped most and what is the ‘month on month’ growth in that period?

Solution

We can see that country XX’s Outward Investment to Singapore dropped in Mar 2011 and Apr 2011.

Month on month growth in Mar2011 = $$\frac{741-1211}{1211}\times 100$$ = -38.81 percent.

Month on month growth in Apr 2011 = $$\frac{378-741}{741}\times 100$$ = -48.98 percent.

Hence, option C is the correct answer.

What is the share of Country XX’s Outward Investment together in USA and UK in February 2011 of its total investment in the world?

Solution

Country XX’s Outward Investment together in USA and UK in February 2011 = 116+117 = USD 233 millions.

Country XX’s total Outward Investment in the world in Feb 11 = 3221

Hence, the required percentage = $$\dfrac{233}{3221}\times 100$$ $$\approx$$ 7.24 percent. Therefore, option A is the correct answer.

In which month the share of Country XX’s total Outward Investment together in Singapore and UAE achieved the highest level and what is the value?

Solution

Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = 273+86 = 359 millions.

Therefore, the share of Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = $$\dfrac{359}{3075}*100$$ = 11.67 percent.

Country XX’s total Outward Investment together in Singapore and UAE in Feb 11 = 1211+227 = 1438 millions.

Therefore, the share of Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = $$\dfrac{1438}{3221}*100$$ = 44.64 percent.

Country XX’s total Outward Investment together in Singapore and UAE in Mar 11 = 741+70 = 811 millions.

Therefore, the share of Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = $$\dfrac{811}{2358}*100$$ = 34.39 percent.

Country XX’s total Outward Investment together in Singapore and UAE in Apr 11 = 378+157 = 535 millions.

Therefore, the share of Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = $$\dfrac{535}{1390}*100$$ = 38.49 percent.

Country XX’s total Outward Investment together in Singapore and UAE in May 11 = 615+142 = 757 millions.

Therefore, the share of Country XX’s total Outward Investment together in Singapore and UAE in Jan 11 = $$\dfrac{757}{3701}*100$$ = 20.45 percent.

We can see that the share as a total is the highest for Feb 11 and it is approx 45 percent. Hence, option B is the correct answer.

Between February 2011 and April 2011, to which country did Outward Investment from XX witness the highest decline?

Solution

From February 2011 to April 2011, Outward Investment from XX witness declined in the Singapore by = 1211 - 378 = 833 millions.

From February 2011 to April 2011, Outward Investment from XX witness declined in the UK = 117 - 44 = 73 millions.

From February 2011 to April 2011, Outward Investment from XX witness declined in the UAE = 227 - 157 = 70 millions.

From February 2011 to April 2011, Outward Investment from XX witness declined in the others = 1551 - 686 = 865 millions.

We can see that "others" have a decline of 865 millions and it is the highest decline for any country among the given choices.

Hence, option D is the correct answer.

Answer the following questions based on the table below, which reports certain data series from National Accounts Statistics of India at Current Prices.

The GDP is sum total of the contributions from primary sector, secondary sector and the tertiary sector. If that be the case, then over 2004-05 to 2009-10, the share of tertiary sector at factor cost in GDP has increased from:

Solution

Value of the GDP from the tertiary sector in the year 2004-05 = 2971464 - 650454 - 744755 = 1576255

Hence, the share of tertiary sector at factor cost in GDP in the year 2004-05 = $$\dfrac{1576255}{2971464}\times 100$$ = 53.05 percent.

Value of the GDP from the tertiary sector in the year 2009-10 = 6133230- 1243566 - 1499601 = 3390063

Hence, the share of tertiary sector at factor cost in GDP in the year 2009-10 = $$\dfrac{3390063}{6133230}\times 100$$ = 55.27 percent.

We can see that the share of tertiary sector at factor cost in GDP increased from 53.05 percent to 55.27 percent. Therefore, option A is the correct answer.

The annual growth rate in the GNP series at factor cost was highest between;

Solution

Let us check the options one by one.

Option (A): The annual growth rate in the GNP series at factor cost between 2008-09 and 2009-10 = $$\dfrac{6095230-5249463}{5249463}\times 100$$ = 16.11 percent.

Option (B): The annual growth rate in the GNP series at factor cost between 2006-07 and 2007-08 = $$\dfrac{4560910-3919007}{3919007}\times 100$$ = 16.38 percent.

Option (C): The annual growth rate in the GNP series at factor cost between 2007-08 and 2008-09 = $$\dfrac{5249463-4560910}{4560910}\times 100$$ = 15.09 percent.

Option (D): The annual growth rate in the GNP series at factor cost between 2005-06 and 2006-07 =$$\dfrac{3919007-3363505}{3363505}\times 100$$ = 16.52 percent.

We can see that the value is the highest between 2005-06 and 2006-07. Hence, option D is the correct answer.

Had Gross Domestic Savings (GDS) between 2008-09 and 2009-10 increased by 30 percent, then during 2009-10 GDS expressed as a percentage of GDP at market prices would have been:

Solution

If Gross Domestic Savings (GDS) in 2009-10 increased by 30 percent over 2008-09 , then the value of GDS in the year 2009-10 = 1.3*1798347 = 2337851.10

Hence, GDS as a percentage of GDP at market prices in the year 2009-10 = $$\dfrac{2337851.10}{6550271}\times 100$$ = 35.69 percent.

Therefore, option C is the correct answer.

Mark the highest figure from the following:

Solution

Let us check the options one by one.

Option (A): Percentage change in GDP from Secondary sector (at Factor Cost) between 2006-07 and 2007-08 = $$\dfrac{1205464-1033410}{1033410}\times 100$$ = 16.65 percent.

Option (B): Percentage change in GDP at Market Prices between 2008-09 and 2009-10 = $$\dfrac{6550271-5582623}{5582623}\times 100$$ = 17.33 percent.

Option (C): Percentage change in Gross Domestic Savings between 2004-05 and 2005-06 = $$\dfrac{1235288-1050703}{1050703}\times 100$$ = 17.57 percent.

Option (D): Percentage change in Gross Domestic Capital Formation between 2008-09 and 2009-10 = $$\dfrac{2344179-1973535}{1973535}\times 100$$ = 18.78 percent.

We can see that value is the highest for option D. Hence, option D is the correct answer.

Identify the correct Statement:

Solution

Gross Domestic Capital Formation expressed as a percentage of GDP (at Market Prices) in the year 2004-05 = $$\dfrac{1052232}{3242209}*100$$ = 32.45 percent.

Gross Domestic Capital Formation expressed as a percentage of GDP (at Market Prices) in the year 2005-06 = $$\dfrac{1266245}{3692485}*100$$ = 34.29 percent.

Gross Domestic Capital Formation expressed as a percentage of GDP (at Market Prices) in the year 2006-07 = $$\dfrac{1540749}{4293672}*100$$ = 35.88 percent.

Gross Domestic Capital Formation expressed as a percentage of GDP (at Market Prices) in the year 2007-08 = $$\dfrac{1896563}{4986426}*100$$ = 38.03 percent.

We can see that Gross Domestic Capital Formation expressed as a percentage of GDP (at Market Prices) has increased consistently between 2004-05 and 2007-08. Hence, option C is the correct answer.

Answer the following questions based on the table below, which reports global market share of Leading Exporting and Importing countries for Select Product groups.

Identify the highest number:

Solution

Increase in Malaysia’s share in global Chemical Products export between 2000 and 2009 = 0.7 - 0.4 = 0.3

Increase in India’s share in global Office and Telecom Equipment export between 2000 and 2009 = 0.3-0.1 = 0.2

Increase in Mexico’s share in global Chemical Products export between 2000 and 2009 = 0.3-0.2 = 0.1

Increase in Thailand’s share in global Integrated Circuits and Electronic Components export between 2000 and 2009 = 2.1 - 1.9 = 0.2

Thus, Increase in Malaysia’s share in global Chemical Products export between 2000 and 2009 is the highest number.

Hence, option A is the correct answer.

Mark the correct statement:

Solution

We can see that the share of the EU has decreased in global import for Office and telecom equipments and thus, option A is incorrect.

We can see that the global export share has remained same for 3 countries:-

Malaysia(Automotive products), India(IC and EC) and South Korea(Clothing Products). Thus, option B is incorrect.

We can see that the global import share has remained same for 3 countries:-

China(Clothing products), Thailand(Clothing products) and South Korea(IC and EC). Thus, option C is also incorrect.

The share of India in importing chemical products has increased by 125% which is greater than any other countries share.

Hence, option D is the correct answer.

Mark the false statement:

Solution

India’s global export share for Clothing Products between 2000 and 2009 = $$\frac{(3.6-3)*100}{3} = 20\%$$

Japan’s global export share for Chemical Products between 2000 and 2009 = $$\frac{(6-4.2)*100}{6} = 30\%$$

South Korea’s global export share for Integrated Circuits and Electronic Components between 2000 and 2009 = $$\frac{(8-7.6)*100}{8} = 5\%$$

Malaysia’s global import share for Clothing Products between 2000 and 2009 = $$\frac{(0.6-0.3)*100}{0.3} = 100\%$$

Thus, option C is incorrect.

Hence, option C is the correct answer.

If between 2000 and 2009, India’s export market share in Integrated Circuits and Electronic Components had increased by 600 percent, the rank of the country in terms of market share in 2009 would have been:

Solution

If between 2000 and 2009, India’s export market share in Integrated Circuits and Electronic Components had increased by 600 percent then the India’s export market share in Integrated Circuits and Electronic Components in 2009 will be 0.7%

Thus, the rank of India will be 8th after, 13.5, 11.4, 10.7, 10.3, 7.6, 7.5 and 2.1

Hence, option B is the correct answer.

Considering both global export and import market dynamics, China has witnessed highest percentage change in its market share between 2000 and 2009 in the following product groups:

Solution

Percentage change in Integrated Circuits and Electronic Components imports for China from 2000-2009 = $$\frac{32.8-6.3}{6.3} \approx 400\%$$

Percentage change in Office and Telecom Equipment exports for China from 2000-2009 = $$\frac{26.2-4.5}{4.5} \approx 500\%$$

Percentage change in Integrated Circuits and Electronic Components exports for China from 2000-2009 = $$\frac{11.4-1.7}{1.7} \approx 550\% $$

Percentage change in Automotive Products imports for China from 2000-2009 = $$\frac{3.6-0.7}{0.7} \approx 400\% $$

Thus, Percentage change in Integrated Circuits and Electronic Components exports for China from 2000-2009 is the highest among the given options.

Hence, option C is the correct answer.

Suppose the ten countries reported in the above table are arranged according to their continent: North America, EU and Asia. Then in terms of export market share for (i) Chemical Products, (ii) Automotive Products, (iii) Office and Telecom Equipment Products and (iv) Integrated Circuits and Electronic Components respectively, the continent-wise ranking in 2009 would be:

Solution

The following table shows the distribution of the countries s EU, Asia and North America along with the shares:-

Thus, option A follows the right order.

Hence, option A is the correct answer.

Read the following instructions and answer the questions.

After the discussion at a high level meeting of government officers, the criteria for issuing of import / export licence to eligible business firms for the year 2011-12 were finalized as follows. The firms must –

I. Have a Grade – ‘A’ certified unit for any products.

II. Not have any legal dispute case against it.

III. Possess minimum asset worth Rs. 40 lakhs.

IV. Submit an environment clearance certificate issued by the Pollution Control Board (PCB) of the state where the firm is located.

V. Deposit the margin money of Rs. 1 lakh.

VI. Arrange for three guarantors with their personal identity cards (IDs).

However, if the firm satisfies all the above mentioned criteria except:

a) Criteria (I), but is a traditional handloom production unit, then the case may be referred to Development Commissioner, Handloom (DCH) of the state.