Which multilateral development bank has been set up by BRICS as an alternative to the World Bank and the International Monetary Fund?

IIFT 2015 Question Paper

For the following questions answer them individually

Solution

A new bank dedicated to the emerging BRICS countries opened for business in China's commercial hub of Shanghai on Tuesday, the official Xinhua news agency reported. The so-called emerging BRICS countries are made up of Brazil, Russia, India, China and South Africa, and their "New Development Bank" has been seen as a challenge to the Washington-based International Monetary Fund and World Bank.

Given below are some popular stock indices of the world. Match the stock index with the country and stock market it represents.

Solution

The DAX is a blue chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. Prices are taken from the Xetra trading venue.

The Nikkei 225, more commonly called the Nikkei, the Nikkei index, or the Nikkei Stock Average, is a stock market index for the Tokyo Stock Exchange. It has been calculated daily by the Nihon Keizai Shinbun newspaper since 1950.

The Korea Composite Stock Price Index or KOSPI is the index of all common stocks traded on the Stock Market Division—previously, Korea Stock Exchange—of the Korea Exchange. It is the representative stock market index of South Korea, like the S&P 500 in the United States.

The Bovespa Index (Portuguese: Índice Bovespa) best known as Ibovespa is the benchmark index of about 60 stocks that are traded on the B3 (Bovespa: BOlsa de Valores do Estado de São PAulo).

Hence, option D is the correct answer.

The remains of which ancient civilization can be seen at the site of Machu Pichu in Peru?

Solution

Although known locally, it was not known to the Spanish during the colonial period and remained unknown to the outside world until American historian Hiram Bingham brought it to international attention in 1911. Machu Picchu was built in the classical Inca style, with polished dry-stone walls.

Who is acknowledged as the creator of Chandigarh’s Rock Garden?

Solution

The Rock Garden of Chandigarh is a sculpture garden in Chandigarh, India. It is also known as Nek Chand's Rock Garden after its founder Nek Chand, a government official who started the garden secretly in his spare time in 1957.

Which is the first Eurozone nation to exit its bailout package?

Solution

In December 2013, after three years on financial life support,Ireland finally left the EU/IMF bailout programme, although it retained a debt of €22.5 billion to the IMF; in August 2014, early repayment of €15 billion was being considered, which would save the country €375 million in surcharges.

Match the name of the city with the river on whose banks it is located

Solution

Budapest is the capital city of Hungary, made up of Buda and Pest, with the Danube River flowing past them, along a stretch of 28 kilometers.

The city of Baghdad is situated on the bank of river Tigris.

Rome is situated at the banks of 'Tiber River'.

A Center of Asia, Seoul Metropolitan. The history of the city of Seoul dates back approximately 2,000 years, to when Wiryeseong, the capital of Baekje, was located on the banks of the Hangang River in the southeastern part of what is now Seoul.

Hence, option A is the correct answer.

What is the motto of the 2016 Summer Olympics to be held in Rio de Janeiro?

Solution

Live Your Passion is the motto of the 2016 Summer Olympics to be held in Rio de Janeiro.

Which film won the 2015 Oscar Award for the “Best Animated Feature Film”?

Solution

'Big Hero 6' was directed by Don Hall and Chris Williams, and produced by Kristina Reed and Roy Conli won the 2015 Oscar Award for the “Best Animated Feature Film”.

Who among the following has won the maximum all time Grand Slam Women’s Singles title?

Solution

Margaret Court, also known as Margaret Smith Court, is a retired Australian tennis player and former world No. 1. In tennis, she amassed more major titles than any other player in history.

In 1970, Court became the first woman during the Open era (and the second woman in history) to win the singles Grand Slam (all four major tournaments in the same calendar year). She won 24 of those titles (11 in the Open era), a record that still stands.

Match the name of the Multinational Firm with whom the following Indians are/ have been associated as CEO

Solution

Anshu Jain is a British Indian business executive who currently serves as president of Cantor Fitzgerald. Jain formerly served as the Co-CEO of Deutsche Bank from 2012 until July 2015. Jain was a member of Deutsche Bank’s Management Board.

Shantanu Narayen is an Indian American business executive, and the CEO of Adobe Systems, and president of the board of the Adobe Foundation. Prior to this, he had been the president and chief operating officer since 2005.

Ajaypal "Ajay" Singh Banga is an Indian Sikh American business executive. He is the current president and chief executive officer of MasterCard.

Rakesh Kapoor is an Indian businessman. He is chief executive of Reckitt Benckiser plc, a UK FTSE-listed multinational consumer goods company, a major producer of health, hygiene and home products.

Hence, we can say that option A is the correct answer.

A person with ‘AB’ blood group is also called a universal recipient because of the

Who is the Vice Chairman of the NITI Aayog?

Solution

Rajiv Kumar (born 6 July 1951) is an Indian economist and is currently the vice-chairman of the NITI Aayog.

The first Export Processing Zone of Asia was set up in

Solution

India is one of the first countries in Asia to recognize the effectiveness of the Export Processing Zone (EPZ) model in promoting export. India was inspired by China for setting up of SEZ. Asia's First EPZ was set up in Kandla in 1965.

Who launched a ‘crowd funding’ campaign to raise funds for bailing out Greece?

Solution

Campaign organiser Thomas Feeney wasted no time in launching the campaign again. A crowdfunding campaign trying to raise €1.6 billion to bail out Greece has ended with contributions just shy of the €2 million mark - or 0 per cent of the total needed to make a difference to Greece.

Match the name of the book with its autor.

Solution

To Kill a Mockingbird - Harper Lee

A Passage to India (1924) is a novel by English author E. M. Forster.

Globalization and Its Discontents is a book published in 2002 by the 2001 Nobel laureate Joseph E. Stiglitz.

The World Is Flat: A Brief History of the Twenty-first Century is an international best-selling book by Thomas L. Friedman.

The U.S. recently announced that its redesigned ten-dollar bill, to be issued in 2020, will include the

Solution

The U.S. plans to put a woman on the $10 bill, announcing Wednesday that the next $10 bill will feature the likeness of a woman who has played a major role in American history and has been a champion for democracy.

The new note, anticipated to be released in 2020, would be unveiled just in time for the 100th anniversary of the passage of the 19th Amendment, which secured women’s suffrage. “America’s currency makes a statement about who we are and what we stand for as a nation,” Treasury Secretary Jack Lew said on a call Wednesday.

The new Centre-State tax sharing model promised a 10% increase in the State’s share. This 10% increase will result from increasing the share from

Solution

The Narendra Modi government accepted recommendations of the 14th Finance Commission for increasing share of states in central taxes to 42%.

The commission recommended increase in the share of states in the centre's tax revenue from the current 32% to 42%-the single largest increase ever recommended. The recommendation, which the government will likely accept, will give more power to states in determining how they spend this money (it also correspondingly reduces the fiscal resources available to the centre).

Hence, option A is the correct answer.

Which of the following countries is not a member of European Union?

Solution

The European Union (EU) is a political and economic union of certain European states. At present, it has 28 member states: Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Italy, Ireland, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Spain, Slovakia, Slovenia, Sweden and the United Kingdom (UK).

Clearly, Norway is not a member of EU.

As per the monetary policy agreement between RBI and the Finance Ministry, the RBI is required to maintain inflation in the range of:

Solution

As per the monetary policy agreement between RBI and the Finance Ministry, the RBI is required to maintain inflation in the range in 4 $$\pm$$ 2 % interval. i.e. 2% to 6%

Who discovered ‘Pluto’ in the year 1930?

Solution

Clyde William Tombaugh was an American astronomer. He discovered Pluto in 1930, the first object to be discovered in what would later be identified as the Kuiper belt.

According to the World Investment Report 2015 published by UNCTAD, which of the following countries was the largest recipient of FDI inflows in 2014?

Solution

China received a total sum of 129 billions USD as FDI inflows in 2014 which was the highest for any nation in the world.

Euro dollars are

Solution

Eurodollars are time deposits denominated in U.S. dollars at banks outside the United States, and thus are not under the jurisdiction of the Federal Reserve. Consequently, such deposits are subject to much less regulation than similar deposits within the U.S. The term was originally coined for U.S. dollars in European banks, but it expanded over the years to its present definition. A U.S. dollar-denominated deposit in Tokyo or Beijing would be likewise deemed a Eurodollar deposit. There is no connection with the euro currency or the eurozone.

Match the Prime Ministers and Presidents of India who have been contemporaries in Office

Solution

Prime Minister President

Indira Gandhi ------------------Sarvepalli Radhakrishnan, Zakir Husain, V. V. Giri, Fakhruddin Ali Ahmed

Rajiv Gandhi -------------------Zail Singh, R. Venkataraman

I K Gujral ------------------------Shankar Dayal Sharma, K. R. Narayanan

Manmohan Singh --------------A. P. J. Abdul Kalam, Pratibha Patil, Pranab Mukherjee

We can see that option D contains all correct matches.

Mark the wrong combination

Solution

Sir Alexander Fleming, a Scottish researcher, is credited with the discovery of penicillin in 1928. At the time, Fleming was experimenting with the influenza virus in the Laboratory of the Inoculation Department at St. Mary’s Hospital in London.

Often described as a careless lab technician, Fleming returned from a two-week vacation to find that a mold had developed on an accidentally contaminated staphylococcus culture plate. Upon examination of the mold, he noticed that the culture prevented the growth of staphylococci.

Hence, option D is the incorrect answer. Rest of the options contain correct pair.

Mother Teresa was born in

Solution

Mother Teresa, known in the Roman Catholic Church as Saint Teresa of Calcutta was an Albanian-Indian Roman Catholic nun and missionary. She was born in Skopje (now the capital of Macedonia), then part of the Kosovo Vilayet of the Ottoman Empire. After living in Macedonia for eighteen years she moved to Ireland and then to India, where she lived for most of her life.

In 1985-86, an official policy introduced by Gorbachev in Soviet Union that stressed on honest discussion about the country’s social issues and concerns was called

Solution

In May 1985, two months after coming to power, Mikhail Gorbachev delivered a speech in St. Petersburg (then known as Leningrad), in which he publicly criticized the inefficient economic system of the Soviet Union, making him the first Communist leader to do so.

This was followed by a February 1986 speech to the Communist Party Congress, in which he expanded upon the need for political and economic restructuring, or perestroika, and called for a new era of transparency and openness, or glasnost. Therefore, option A is the correct answer.

The British Cosmologist Stephen Hawing and the Russian entrepreneur Yuri Milner have launched a project to search for the extra terrestrial life. This project is called:

Solution

The Breakthrough Listen Project: BLP is US$100-million global astronomical initiative launched in 2015 by Internet investor Yuri Milner and cosmologist Stephen Hawking. It has teams from around the world to find signs of intelligent life in universe. The 10-year programme aims to survey 1,000,000 closest stars to Earth by scanning entire galactic plane of Milky Way. It will listen for messages from the 100 closest galaxies at 10 billion different frequencies originated beyond our galaxy.

Match the name of the organization with the name of the city in which it is headquartered.

Solution

International Monetary Fund (IMF) - Washington DC, US

International Olympic Committee - Lausanne, Switzerland

International Labour Organisation (ILO) - Geneva, Switzerland

International Chamber of Commerce - Paris, France

Hence, option C is the correct answer.

The internal evaluation for Economics course in an Engineering programme is based on the score of four quizzes. Rahul has secured 70, 90 and 80 in the first three quizzes. The fourth quiz has ten True-False type questions, each carrying 10 marks. What is the probability that Rahul’s average internal marks for the Economics course is more than 80, given that he decides to guess randomly on the final quiz?

Solution

Rahul has to score either 90 or 100 marks in the fourth quiz in order to have average more than 80.

So,there will be two cases:

Case 1: If Rahul scores 90 marks

Then 9 out of 10 will be correct and those 9 correct answers can be in any order. So, total ways of arranging them is $$\frac{10!}{9!}$$

And the probability of choosing either a right answer or wrong answer is $$\frac{1}{2}$$

Hence, the probability of getting 9 answers correct is: $$\frac{10!}{9!}$$ x $$(\frac{1}{2})^{10}$$

Case 2: If Rahul scores 100 marks

Then 10 out of 10 will be correct. So, total ways of arranging them is $$\frac{10!}{10!}$$ = 1

And the probability of choosing either a right answer or wrong answer is $$\frac{1}{2}$$

Hence, the probability of getting all 10 answers correct is: $$(\frac{1}{2})^{10}$$

So, the final probability is $$\frac{10!}{9!}$$ x $$\frac{1}{2^{10}}$$ + $$\frac{1}{2^{10}}$$ = $$\frac{11}{1024}$$

In 2004, Rohini was thrice as old as her brother Arvind. In 2014, Rohini was only six years older than her brother. In which year was Rohini born?

Solution

In 2004, let age of Arvind be x, then age of Rohini will be 3x.

It is also given that in 2014, she is older by 6 years than her brother.

It means that their ages differ by 6 years.

So, 3x - x = 6

2x = 6

x=3.

In 2004, Arvind age is 3 years and Rohini age is 9 years.

Hence, Rohini was born in 1995.

If p, q and r are three unequal numbers such that p, q and r are in A.P., and p, r-q and q-p are in G.P., then p : q : r is equal to:

Solution

Given that p, q and r are in A.P.,

2q = p + r

p = 2q - r Eq -1

Given that p, r-q and q-p are in G.P.,

Let us assume the common ratio of k in G.P.

r-q = k(p) Eq -2

q-p = k(r-q) Eq -3

q-p = $$k^{2}$$(p) Eq -4

Substitute Eq-1 in Eq-3,

q-(2q-r) = k(r-q)

r-q = k(r-q)

So, k=1

From Eq -4, we get q=2p

Now substitute q=2p in Eq-1 we get r=3p

Hence, ratio of p:q:r = p:2p:3p = 1:2:3

If $$log_{25}{5}$$ = a and $$log_{25}{15} $$ = b, then the value of $$log_{25}{27}$$ is:

Solution

$$log_{25}{5}$$ = a

=> a=1/2

$$log_{25}{15}$$ = $$log_{25}{3}+log_{25}{5}$$ = b

$$\frac{1}{2} \log_{5}{3} + \frac{1}{2}$$ = b

$$\log_{5}{3}$$ = 2(b - $$\frac{1}{2})$$.............(i)

$$log_{25}{27}$$ = $$\frac{3}{2} \log_{5}{3}$$.........(ii)

Replacing $$\log_{5}{3}$$ = 2(b - $$\frac{1}{2})$$ in (ii) we get

$$log_{25}{27}$$ = 3(b - $$\frac{1}{2}$$)

We can write -$$\frac{1}{2}$$ as (- 1 + $$\frac{1}{2}$$) or (-1 + a)

So, $$log_{25}{27}$$ = 3(b + a - 1)

Hence, option C is the correct answer.

During the essay writing stage of MBA admission process in a reputed B-School, each group consists of 10 students. In one such group, two students are batchmates from the same IIT department. Assuming that the students are sitting in a row, the number of ways in which the students can sit so that the two batchmates are not sitting next to each other, is:

Solution

Consider the case where batchmates are sitting together and then subtract those cases from total no. of cases.

When 10 students are arranged in a line, total arrangements possible are 10!

Now considering batchmates sitting together,

B1 B2 _ _ _ _ _ _ _ _

Then total arrangements possible are 9!*2!

Total ways = 10! - 9!*2!

9!*8 = 2903040

The pre-paid recharge of Airtel gives 21% less talktime than the same price pre-paid recharge of Vodafone. The post-paid talktime of Airtel is 12% more than its pre-paid recharge, having the same price. Further, the post-paid talktime of same price of Vodafone is 15% less than its pre-paid recharge. How much percent less / more talktime (approximately) can one get from the Airtel post-paid service compared to the post-paid service of Vodafone?

Solution

Let the value of pre-paid recharge of Vodafone be 100.

Then the value of pre-paid recharge of Airtel is 79.

Airtel gives 12% more to post-paid, so post-paid value is 79 x 1.12 = 88.48

Vodafone gives 15% less to post-paid than its pre-paid so its value is 85.

Clearly Airtel gives more to its post-paid customers.

Percentage = $$\frac{3.48}{85}$$ x 100 = 4.09%

Therefore, option A is the right answer.

As a strategy towards retention of customers, the service centre of a split AC machine manufacturer offers discount as per the following rule: for the second service in a year, the customer can avail of a 10% discount; for the third and fourth servicing within a year, the customer can avail of 11% and 12% discounts respectively of the previous amount paid, Finally, if a customer gets more than four services within a year, he has to pay just 45% of the original servicing charges. If Rohan has availed 5 services from the same service centre in a given year, the total percentage discount availed by him is approximately:

Solution

Let the original service charge be Rs. 1000

1st service charge = Rs. 1000

2nd service charge @ 10% discount = Rs. 900

3rd service charge @ 11% discount = Rs. 801

4th service charge @ 12% discount = Rs. 704.88

5th service charge @ 45% = Rs. 450

Total service charge for Rohan = Rs. 1000 + Rs. 900 + Rs. 801 + Rs. 704.88 + Rs. 450 = Rs. 3855.887

Discount % = 22.88%

Hence, option B is the correct answer.

A tank is connected with both inlet pipes and outlet pipes. Individually, an inlet pipe can fill the tank in 7 hours and an outlet pipe can empty it in 5 hours. If all the pipes are kept open, it takes exactly 7 hours for a completely filled-in tank to empty. If the total number of pipes connected to the tank is 11, how many of these are inlet pipes?

Solution

Let the number of inlet pipes be x, then the number of outlet pipes will be 11-x.

The rate of emptying the tank is more than filling the tank if all the pipes are kept opened.

$$\frac{11-x}{5}$$ - $$\frac{x}{7}$$ = $$\frac{1}{7}$$

Solving, 12x =72,Hence x = 6

Therefore, the number of inlet pipes is 6.

In a certain village, 22% of the families own agricultural land, 18% own a mobile phone and 1600 families own both agricultural land and a mobile phone. If 68% of the families neither own agricultural land nor a mobile phone, then the total number of families living in the village is:

Solution

22% of the families own agricultural land, 18% own a mobile phone, 1600 families own both and 68% families own none.

P(A $$\cup$$ B) = P(A) + P(B) - P(A $$\cap$$ B)

32 = 22 + 18 - x

x=8. Hence, there will be 8% families who own both.

8% =1600 (Given in question)

Total families in a village =>100% = 20000

In the board meeting of a FMCG Company, everybody present in the meeting shakes hand with everybody else. If the total number of handshakes is 78, the number of members who attended the board meeting is:

Solution

Total handshakes are given by: N$$C_2$$

N$$C_2$$ = 78

$$\frac{N*(N-1)}{2}$$ = 78

N=13

Hence, option D is the correct answer.

A firm is thinking of buying a printer for its office use for the next one year. The criterion for choosing is based on the least per-page printing cost. It can choose between an inkjet printer which costs Rs. 5000 and a laser printer which costs Rs. 8000. The per-page printing cost for an inkjet is Rs. 1.80 and that for a laser printer is Rs. 1.50. The firm should purchase the laser printer, if the minimum number of a pages to be printed in the year exceeds

Solution

We have to find for how many pages, the cost of printing including the price of the printer, will be same for both the printers.

Let the number of pages be n

For inkjet printer, the cost is 5000 + 1.80*n

For laser printer, the cost is 8000 + 1.50*n

Equating: 5000 + 1.80*n = 8000 + 1.50*n

n=10000

For n>10000, the per page printing cost is lesser for laser printer than inkjet printer.

So, firm should purchase laser printer if number of pages printed are more than 10000.

Hence, option B is the correct answer.

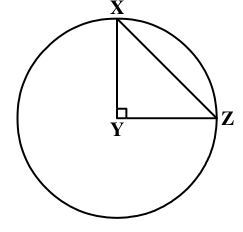

If in the figure below, angle XYZ = 90° and the length of the arc XZ = 10$$\pi$$, then the area of the sector XYZ is

Solution

Length of arc XZ is the perimeter of quarter circle.

$$\frac{\pi r}{2}$$ = 10$$\pi$$

r=20

Area of sector XYZ = Area of quarter circle = $$\frac{\pi r^{2}}{4}$$

Area = 100$$\pi$$

A chartered bus carrying office employees travels everyday in two shifts- morning and evening. In the evening, the bus travels at an average speed which is 50% greater than the morning average speed; but takes 50% more time than the amount of time it takes in the morning. The average speed of the chartered bus for the entire journey is greater/less than its average speed in the morning by

Solution

Distance = Speed x Time

In morning slot, Let speed be S and time taken be T, then distance covered = ST

Then, in evening slot, speed will be 1.5S and time taken will be 1.5T, then distance covered = 2.25ST

Average Speed = $$\frac{Total \space distance \space covered}{Total \space time \space taken}$$

For entire journey, average speed is:

Average Speed =$$\frac{ST + 2.25ST}{T + 1.5T}$$ = $$\frac{3.25ST}{2.5T}$$ = 1.3S

For morning, Average Speed is S.

Hence, the average speed of the bus for the entire journey is greater than its average speed in the morning by 30%

If a right circular cylinder of height 14 $$cm$$ is inscribed in a sphere of radius 8 $$cm$$, then the volume of the cylinder is:

Solution

The radius of sphere is 8 $$cm$$. Then applying Pythagoras, the radius of base of cylinder is $$\sqrt{15}$$ $$cm$$

The height of cylinder is given as 14 $$cm$$. Volume of cylinder is $$\pi$$ $$r^{2}$$h

$$\frac{22}{7}$$* 15*14 = 660 $$cm^3$$

Seema has joined a new Company after the completion of her B.Tech from a reputed engineering college in Chennai. She saves 10% of her income in each of the first three months of her service and for every subsequent month, her savings are Rs. 50 more than the savings of the immediate previous month. If her joining income was Rs. 3000, her total savings from the start of the service will be Rs. 11400 in:

Solution

Seema saved Rs. 900 in the first 3 months. She must saved Rs. (11400 - 900) = Rs. 10500 in the subsequent months.

The sequence will be of the form: 350 + 400 +........... $$n$$ terms = 10500

=> $$\frac{n}{2}$$ [2*350 + ($$n$$-1)*50] = 10500

=> $$\frac{n}{2}$$ [70 + ($$n$$-1)5] = 1050

=> $$n^{2}$$ + 13$$n$$ = 420

Solving, we get $$n$$ = 15

The savings of Rs. 10500 is done in 15 months. Seema saved Rs. 11400 in 15+3 = 18 months.

Hence, option C is the correct answer.

Sailesh is working as a sales executive with a reputed FMCG Company in Hyderabad. As per the Company’s policy, Sailesh gets a commission of 6% on all sales upto Rs. 1,00,000 and 5% on all sales in excess of this amount. If Sailesh remits Rs. 2,65,000 to the FMCG company after deducting his commission, his total sales were worth:

Solution

Let total sales be 'x'

The commission that Sailesh will get is x - 265000

He gets 6% on sales upto 100000 and 5% on sales greater than that.

Calculating his commission on total sales:

0.06*100000 + 0.05(x-100000)

Equating,

0.05x + 1000 = x - 265000

0.95x = 266000

x= 280000

Hence, his sales were worth 280,000

Three carpenters P, Q and R are entrusted with office furniture work. P can do a job in 42 days. If Q is 26% more efficient than P and R is 50% more efficient than Q, then Q and R together can finish the job in approximately:

Solution

P is doing a job in 42 days. In one day, he does 1/42 of the work.

Q is more efficient than P by 26%.

Then, the part of work that Q does in one day is: $$\frac{1}{42}$$ x 1.26 = 3/100

R is more efficient than Q by 50%.

Then, the part of work that R does in one day is: $$\frac{3}{100}$$ x 1.5 = 9/200

If Q and R are put together then part of work they will finish in a day is:

$$\frac{3}{100}$$ + $$\frac{9}{200}$$ = $$\frac{15}{200}$$

Hence total work can be done in 200/15 = 13.33 days $$\cong$$ 13 days

There are two alloys P and Q made up of silver, copper and aluminium. Alloy P contains 45% silver and rest aluminum. Alloy Q contains 30% silver, 35% copper and rest aluminium. Alloys P and Q are mixed in the ratio of 1 : 4.5. The approximate percentages of silver and copper in the newly formed alloy is:

Solution

Composition of alloy P

Silver:Copper:Aluminium = 45:0:55

Composition of alloy Q

Silver:Copper:Aluminium = 30:35:35

They are mixed in ratio of 1: 4.5

Let us consider alloy P is taken 200 grams and alloy Q is taken 900 grams.

Then for alloy P :-

Silver:Copper:Aluminium = 90:0:110

For alloy Q:

Silver:Copper:Aluminium = 270:315:315

Total weight of P and Q combined is 1100 grams.

When P and Q are mixed, the new combined ratio of

Silver:Copper:Aluminium = 360:315:425

Percentage of Silver in mixture = $$\frac{360}{1100}$$ x 100 $$\cong$$ 33%

Percentage of Copper in mixture = $$\frac{315}{1100}$$ x 100 $$\cong$$ 29%

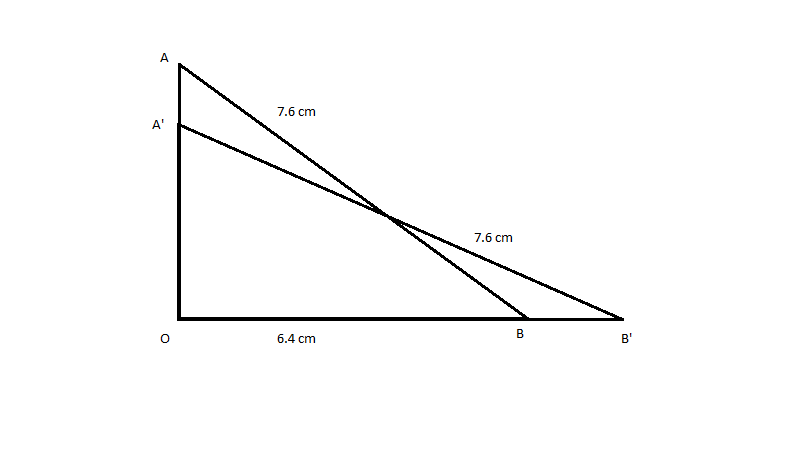

A ladder of 7.6 m long is standing against a wall and the distance between the wall and the base of the a ladder is 6.4 m. If the top of the ladder now slips by 1.2m, then the foot of the ladder shifts by approximately:

Solution

The starting position of ladder is AB.

AB = 7.6 cm and OB = 6.4 cm

Applying Pythagoras Theorem in $$\triangle$$ AOB

$$OA^{2}$$ + $$OB^{2}$$ = $$AB^{2}$$

OA = 4.10 cm

Now ladder top slips by 1.2 cm, the new position of ladder becomes A'B'

OA' = 4.10 - 1.2 = 2.9 cm

Applying Pythagoras Theorem in $$\triangle$$ A'OB'

$$OA'^{2}$$ + $$OB'^{2}$$ = $$A'B'^{2}$$

OB' = 7.02 cm

Hence, the foot of the ladder is shifted by approximately OB' - OB = 0.6cm

The value of x for which the equation $$\sqrt{4x - 9}$$ + $$\sqrt{4x + 9}$$ = 5 + $$\sqrt{7}$$ will be satisfied, is:

Solution

This question can be solved with the help of options easily.

We can say that 4x - 9 $$\geq$$ 0. Hence x $$\geq$$ 2.25. Now we can check option C and D.

Option C: $$\sqrt{4x - 9}$$ + $$\sqrt{4x + 9}$$ = $$\sqrt{3}$$ + $$\sqrt{21}$$ Which is not same as what we have in the question. Hence, this is not the correct answer.

Option D: $$\sqrt{4x - 9}$$ + $$\sqrt{4x + 9}$$ = $$\sqrt{7}$$ + $$\sqrt{25}$$ = 5 + $$\sqrt{7}$$. Which is the same as what we have in the question. Hence, we can say that option D the correct answer.

The simplest value of the expression $$(\frac{4^{p+\frac{1}{4}}\times \sqrt{2 \times 2^{p}}}{2\times \sqrt{2^-p}})^\frac{1}{p}$$

Solution

Simplifying the surds, and writing everything on numerator we get:

= $${(2^{2p + 1/2 + 1/2 + p/2 - 1 + p/2}})^{1/p}$$

= $${(2^{3p}})^{1/p}$$

= $$2^{3}$$ = 8

In a reputed engineering college in Delhi, students are evaluated based on trimesters. The probability that an Engineering student fails in the first trimester is 0.08. If he does not fail in the first trimester, the probability that he is promoted to the second year is 0.87. The probability that the student will complete the first year in the Engineering College is approximately:

Solution

The probability that the student passes in the first trimester is 0.92

Now given that if the student passes in the first trimester then probability of moving into second second year is 0.87

Hence, the probability of completing first year is 0.92 x 0.87 = 0.80

Solve the questions based on the information provided in the passage below:

Six engineers Anthony, Brad, Carla, Dinesh, Evan and Frank are offered jobs at six different locations -England, Germany, India, Australia, Singapore and UAE. The jobs offered are in six different branches, and are based on their competence as well as preference. The branches are IT, Mechanical, Chemical, Electronics, Metallurgy and Electrical, though not necessarily in the same order. Their placements are subject to the following conditions:

i.The engineer in the Electrical Department is not placed in Germany.

ii.Anthony is placed in Singapore while Dinesh in UAE.

iii.Frank is not in the Metallurgy Department but Brad is in the Chemical Department.

iv.Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

v.The only department offering jobs in India is the Chemical Department while there are no vacancies for IT in Singapore.

vi. Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. Both of them settle for the options available based on their interests in the locations allotted to them.

vii. In recent years, UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England.

Who joined the Electronics Department?

Solution

In statement 2 it is given that Anthony is placed in Singapore while Dinesh in UAE and in statement 4 it is given that Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

In statement 6, it is given that UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England. In statement 3, it is mentioned that Brad is in the chemical department and in statement 5 it is mentioned that only India is offering chemical department jobs.

In statement 6, it is mentioned that Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. This implies Frank secured a job in IT department and Anthony in Electrical department.

Carla joined the Electronics department.

The answer is option C.

The person placed in UAE is in the _____________ Department

Solution

In statement 2 it is given that Anthony is placed in Singapore while Dinesh in UAE and in statement 4 it is given that Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

In statement 6, it is given that UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England. In statement 3, it is mentioned that Brad is in the chemical department and in statement 5 it is mentioned that only India is offering chemical department jobs.

In statement 6, it is mentioned that Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. This implies Frank secured a job in IT department and Anthony in Electrical department.

The person placed in UAE is in the Metallurgy department.

The answer is option C.

Out of the following, which is the correct combination?

Solution

In statement 2 it is given that Anthony is placed in Singapore while Dinesh in UAE and in statement 4 it is given that Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

In statement 6, it is given that UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England. In statement 3, it is mentioned that Brad is in the chemical department and in statement 5 it is mentioned that only India is offering chemical department jobs.

In statement 6, it is mentioned that Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. This implies Frank secured a job in IT department and Anthony in Electrical department.

Among the given options, option B is the correct combination.

The answer is option B.

Who joined the IT Department in Australia?

Solution

In statement 2 it is given that Anthony is placed in Singapore while Dinesh in UAE and in statement 4 it is given that Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

In statement 6, it is given that UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England. In statement 3, it is mentioned that Brad is in the chemical department and in statement 5 it is mentioned that only India is offering chemical department jobs.

In statement 6, it is mentioned that Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. This implies Frank secured a job in IT department and Anthony in Electrical department.

Frank joined the IT Department in Australia.

The answer is option A.

Which combination is true for Dinesh?

Solution

In statement 2 it is given that Anthony is placed in Singapore while Dinesh in UAE and in statement 4 it is given that Evan is placed in the Mechanical Department while Frank is offered a job in Australia.

In statement 6, it is given that UAE has emerged as a hub for metallurgy exports and thus recruitment is done for the same while all mechanical posts are in England. In statement 3, it is mentioned that Brad is in the chemical department and in statement 5 it is mentioned that only India is offering chemical department jobs.

In statement 6, it is mentioned that Anthony is interested in IT and Electrical Department while Frank is interested in IT and Mechanical Department. This implies Frank secured a job in IT department and Anthony in Electrical department.

Dinesh - UAE - Metallurgy

The answer is option D.

For the following questions answer them individually

Based on the given statement, choose the right conclusion:

‘If the breakfast doesn’t have eggs, I will not go for a walk and will not have lunch.’

Solution

Let P = The breakfast doesn't have eggs

Q = I will not go for a walk and will not have lunch

So, ~P = The breakfast has eggs

~Q = I will go for a walk or will have lunch, the breakfast has eggs

~Q~P = I will go for a walk or will have lunch, the breakfast has eggs.

Hence option B is correct.

Read the details below and answer the questions that follow.

For astrological reasons, a mother named all her daughters with the letter ‘K’ as Kamla, Kamlesh, Kriti, Kripa, Kranti, and Kalpana.

i. Kamla is not the tallest, while Kripa is not the most qualified.

ii. The shortest is the most qualified amongst them all.

iii. Kalpana is more qualified than Kamlesh, who is more qualified than Kriti.

iv. Kamla is less qualified than Kamlesh but is taller than Kamlesh.

v. Kalpana is shorter than Kriti but taller than Kranti.

vi. Kriti is more qualified than Kamla, while Kamlesh is taller than Kriti.

vii. Kripa is the least qualified amongst the daughters.

Who is the third tallest starting in decreasing order of height?

Solution

Let us arrange the daughters in the decreasing order of height first.

Kalpana is shorter than Kriti but taller than Kranti.

Therefore, Kriti > Kalpana > Kranti.

Kamlesh is taller than Kriti.

Kamlesh > Kriti > Kalpana > Kranti.

Kamla is taller than Kamlesh. Kamla is not the tallest. Therefore, Kripa must be the tallest person.

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Let us arrange the daughters in terms of their qualification.

The shortest person is the most qualified.

Therefore, Kranti must be the most qualified person among the 6 daughters.

Kalpana is more qualified than Kamlesh who is more qualified than Kriti.

Kalpana > Kamlesh > Kriti.

Kamla is less qualified than Kamlesh. Kriti is more qualified than Kamla. Kripa is the least qualified among the daughters.

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Height (in decreasing order):

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Qualification (in decreasing order):

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Kamlesh is the third tallest person. Therefore, option B is the right answer.

Who is the most qualified?

Solution

Let us arrange the daughters in the decreasing order of height first.

Kalpana is shorter than Kriti but taller than Kranti.

Therefore, Kriti > Kalpana > Kranti.

Kamlesh is taller than Kriti.

Kamlesh > Kriti > Kalpana > Kranti.

Kamla is taller than Kamlesh. Kamla is not the tallest. Therefore, Kripa must be the tallest person.

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Let us arrange the daughters in terms of their qualification.

The shortest person is the most qualified.

Therefore, Kranti must be the most qualified person among the 6 daughters.

Kalpana is more qualified than Kamlesh who is more qualified than Kriti.

Kalpana > Kamlesh > Kriti.

Kamla is less qualified than Kamlesh. Kriti is more qualified than Kamla. Kripa is the least qualified among the daughters.

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Height (in decreasing order):

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Qualification (in decreasing order):

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Kranti is the most-qualified among the daughters. Therefore, option D is the right answer.

What is the rank of Kriti in increasing order of qualification?

Solution

Let us arrange the daughters in the decreasing order of height first.

Kalpana is shorter than Kriti but taller than Kranti.

Therefore, Kriti > Kalpana > Kranti.

Kamlesh is taller than Kriti.

Kamlesh > Kriti > Kalpana > Kranti.

Kamla is taller than Kamlesh. Kamla is not the tallest. Therefore, Kripa must be the tallest person.

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Let us arrange the daughters in terms of their qualification.

The shortest person is the most qualified.

Therefore, Kranti must be the most qualified person among the 6 daughters.

Kalpana is more qualified than Kamlesh who is more qualified than Kriti.

Kalpana > Kamlesh > Kriti.

Kamla is less qualified than Kamlesh. Kriti is more qualified than Kamla. Kripa is the least qualified among the daughters.

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Height (in decreasing order):

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Qualification (in decreasing order):

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Rank of Kriti in the increasing order of qualification is 3. Therefore, option B is the right answer.

What is the rank of Kamla in increasing order of height?

Solution

Let us arrange the daughters in the decreasing order of height first.

Kalpana is shorter than Kriti but taller than Kranti.

Therefore, Kriti > Kalpana > Kranti.

Kamlesh is taller than Kriti.

Kamlesh > Kriti > Kalpana > Kranti.

Kamla is taller than Kamlesh. Kamla is not the tallest. Therefore, Kripa must be the tallest person.

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Let us arrange the daughters in terms of their qualification.

The shortest person is the most qualified.

Therefore, Kranti must be the most qualified person among the 6 daughters.

Kalpana is more qualified than Kamlesh who is more qualified than Kriti.

Kalpana > Kamlesh > Kriti.

Kamla is less qualified than Kamlesh. Kriti is more qualified than Kamla. Kripa is the least qualified among the daughters.

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Height (in decreasing order):

Kripa > Kamla > Kamlesh > Kriti > Kalpana > Kranti.

Qualification (in decreasing order):

Kranti > Kalpana > Kamlesh > Kriti > Kamla > Kripa.

Rank of Kamala in the increasing order of height is 5. Therefore, option B is the right answer.

For the following questions answer them individually

Based on the number series given, fill in the missing number. 18, 37, 76, 155, ________, 633, 1272

Solution

The logic employed is as follows:

18*2 + 1 = 36 + 1 = 37

37*2 + 2 = 74 + 2 = 76

76*2 + 3 = 152 + 3 = 155

155*2 + 4 = 310 + 4 = 314

314*2 + 5 = 628 + 5 = 633

As we can see, the blank should be filled by 314. Therefore, option B is the right answer.

Based on the conditions stated in the passage below, answer the questions that follow.

There are three countries, USA, UAE and UK. An exporter can select one country or two countries or all the three countries subject to the conditions below:

Condition 1: Both USA and UAE have to be selected.

Condition 2: Either USA or UK, but not both have to be selected.

Condition 3: UAE can be selected only if UK has been selected.

Condition 4: USA can be selected only if UK is selected.

How many ways countries can be selected if no condition is imposed?

Solution

Since there is no condition for the selection of the countries, we can select

USA; UK; UAE, USA & UK; USA & UAE; UAE & UK, USA, UAE& UK

=7 ways

How many countries can be selected to meet only condition 1?

Solution

According to condition 1, both USA and UAE are selected.

To make sure that none of the other conditions are met, UK cannot be selected.

Thus, only 2 countries can be selected.

Hence, the answer is option B.

How many countries can be selected to meet only conditions 2 and 3?

Solution

According to condition 2, Either USA or UK can be selected but not both.

According to condition 3, UAE can be selected if the UK is selected.

Thus, the choices are:

a. Only USA

b. Only UK

c. UK and UAE

Hence, either 2 or 1 countries can be selected.

The answer is option B.

For the following questions answer them individually

Based on the following relations, which of the given options indicate that W is the niece of X?

A+B means that A is the brother of B.

A*B means that A is the father of B.

A-B means that A is the sister of B.

Solution

Option 1) From Option 1, we cannot determine W's gender, but we can say that W is either the brother or sister of X, which is not the required relation.

Option 2) From Option 2, we cannot determine the gender of x, but we can say that W is the father of X, which is not the required relation.

Option 3) From Option 3, we can determine that W is the niece of X.

Option 4) From Option 4, we can determine that W is the daughter of X, which is not the required relation.

Only option C gives the required relationship, i.e., W is the niece of X.

Hence, the answer is option C.

Alex walks 1 mile towards East and then he turns towards South and walks further 5 miles. After that he turns East and walks 2 miles further. Finally he turns to his North and walks 9 miles. How far is he from the starting point?

Solution

From the given statements, choose the conclusions which follow logically:

Statements:

i. Some iphones are mobiles

ii. Some mobiles are ipads

iii. Some ipads are tablets

Conclusions:

I. Some tablets are iphones

II. Some mobiles are tablets

III. Some ipads are iphones

IV. All iphones are tablets

Solution

The basic diagram from the given conditions is as follows.

Thus, we can observe that none of the conclusions are definitely correct.

Hence, the answer is option D.

Read the passage below and answer the questions that follow.

Export cargo of a trader can go through seven cities P, Q, R, S, T, U and V. The following cities have a two way connection i.e., Cargo can move in both directions between them; S and U, P and Q, Q and R, V and T, R and T, V and U. Cargo can move only in one direction from U to Q.

If the trader wants the cargo to move from City S to City T then excluding cities S and T, what is the minimum number of cities that the cargo has to cross in transit?

Solution

S -> U -> V -> T

The minimum number of cities that the cargo has to cross in transit = 2 (U and V)

The answer is option C.

If the trader wants the cargo to go to City U from City P through the longest route, how many cities will he be required to cross (excluding cities P and U)?

Solution

U -> V -> T -> R -> Q -> P

The number of cities required to cross = 4

The answer is option B.

To move cargo from City P to City U, which of the following statements will minimise the number of cities to be crossed in transit?

Solution

A) Connect cities U to R with a two way connection

Number of cities to be crossed = 2 (Q and R)

B) Connect cities P to S with a one way connection from cities S to P

Number of cities to be crossed = 4

C) Connect cities U to Q with a two way connection

Number of cities to be crossed = 1

D) Connect cities R to V with a two way connection

Number of cities to be crossed = 3

The answer is option C.

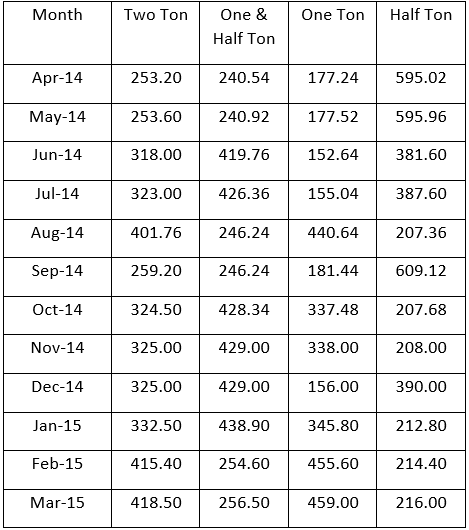

Read the following information and tables and answer the questions that follow.

Torrent Enterprises sells air conditioners of Eagle Brand in the retail market of Delhi. The month-wise total number of Window Air Conditioner (WAC) units sold by Torrent during April 2014 to March 2015 are shown below in Table A. Table B shows the share of different types of WACs in total monthly sales for the said period.

Number of Units Sold by Torrent Enterprises During the Period April 14 to March 15

Table A

Table B

Performance measures are as follows:

Half Yearly Sales Performance:

$$\frac{\text{Oct 14 to Mar 15 Average Sales - April 14 to Sep 14 Average Sales}}{\text{April 14 to Sep 14 Average Sales}}$$

Monthly Sales Performance:

$$\frac{\text{Current Month Sales - Pervious Month Sales}}{\text{Previous Month Sales}}$$

Sales Volatility:

$$\frac{\text{Maximum Monthly Sales - Minimum Monthly Sales}}{\text{Average Monthly Sales}}$$

What is the closest average number of 1 1⁄2 ton Window ACs sold by Torrent Enterprises during April 2014 - March 2015?

Solution

Let's calculate the different WAC types during April 2014 - March 2015 and tabulate it as follows

Average number of 11⁄2 ton Window ACs sold by Torrent Enterprises during April 2014 - March 2015=

=(727.7+1275.12+757.34+1296.24)/12

=338

Hence B is the correct answer.

The absolute difference between average annual sales (in units) of which pair of WACs type is the highest

Solution

Let's calculate the different WAC types during April 2014 - March 2015 and tabulate it as follows

Let's solve the options one by one,

Option A :The absolute difference between average annual sales of 1 Ton and 1⁄2 Ton = 338.03-281.37 = 56.66

Option B: The absolute difference between average annual sales of 1 Ton and 2 Ton = 329.138-281.37 = 47.768

Option C: The absolute difference between average annual sales of 2 Ton and 1⁄2 Ton = 352.128-329.138 = 22.99

Option D:The absolute difference between average annual sales of 11⁄2 Ton and 1⁄2 Ton = 352.128-338.03 = 14.098

The absolute difference between average annual sales of 1 Ton and 1⁄2 Ton is the highest.

Hence A is the correct answer.

Which type of WAC has performed the second best in Half Yearly Sales Performance?

Solution

Let's calculate the different WAC types during April 2014 - March 2015 and tabulate it as follows

Let's calculate Half yearly Sales for Various WAC types:

2 Ton:(2141/6)-(1809/6)/(1809/6)= 0.18(approx)

1⁄2 Ton:(1449/6)-(2777/6)/(2777/6)= -0.48(approx)

1 1⁄2 Ton: (2236/6)-(1820/6)/(1820/6)=0.23(approx)

1 ton :(2092/6)-(1284/6)/(1284/6)=0.63(approx)

Therefore 1 1⁄2 Ton WAC has performed the second best in Half Yearly Sales Performance.

Hence C is the correct answer.

In which of the months given below, the total WAC Monthly Sales Performance was the highest?

Solution

Let's calculate the different WAC types during April 2014 - March 2015 and tabulate it as follows

Monthly Sales Performance in May 2014 =(1268-1266)/1266 = 0.00128

Monthly Sales Performance in June 2014=(1272-1268)/1268 = 0.0032

Monthly Sales Performance in October 2014 =(1298-1296)/1296 = 0.00154

Monthly Sales Performance in February 2015 =(1340-1330)/1330 = 0.0075

So the Monthly Sales Performance in February 2015 is the highest.

Hence D is the correct answer.

Which type of WAC has the least Sales Volatility?

Solution

Let's calculate the different WAC types during April 2014 - March 2015 and tabulate it as follows

Sales Volatility can be calculated by the formula (Maximum Monthly Sales - Minimum Monthly sales )/ Average Monthly sales

1⁄2 Ton = 609-207/352.128 = 1.14

1 Ton =459-153/281.37 = 1.09

11⁄2 Ton = 439-241/338.03 = 0.59

2 Ton = 419-253/ 329.138 = 0.5

Among the different WAC types 2 Ton has the lowest Sales volatility.

Hence D is the correct answer.

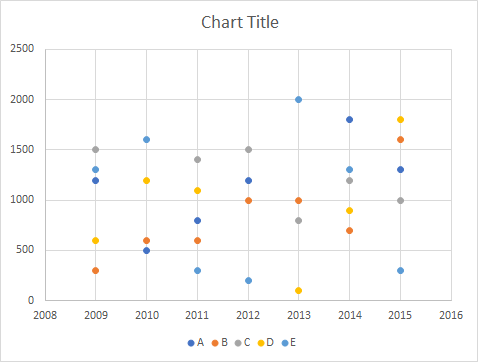

Read the following information, graph and table and answer the questions that follow.

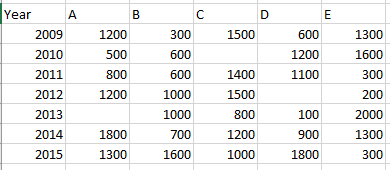

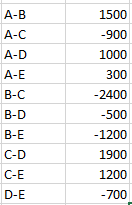

Ellen Inc. is a Mumbai based company which sells five products branded as A, B, C, D and E in India. Anita looks after entire sales of North India working from regional office in Delhi. She was preparing for annual review meeting scheduled next day in Mumbai. She was attempting to analyse sales in North India for the seven year period from 2009 to 2015. She first calculated average sales in rupees of all the five brands and constructed a table exhibiting the difference between average sales of each pair of brands as shown in the following table:

Average Sales of Product A minus Average Sales of Product B

After taking a print out of the above table, she attempted to look at the trend of sales and plotted a graph in MS Excel. Later she took a print out of the graph and left for a meeting. While on her way she figured out that due to some printer cartridge problem sales of Product A in 2013, Product C in 2010, and Product D in 2012 were not visible in the graph as reproduced below. Anita had to make some quick calculations to arrive at the information outlined in the following question.

What are the sales of Product A in 2013, Product C in 2010 and Product D in 2012?

Solution

Let's tabulate the chart ,

Since difference in average sales is given , Difference in sales can be found by multiplying it by 7

For example

Let the sales of A be $$a_1,a_2,a_3,a_4,a_5,a_6,a_7$$ in 2009 - 2015 respectively.

Let the sales of B be $$b_1,b_2,b_3,b_4,b_5,b_6,b_7$$

Given that $$\frac{\left(a_1+a_2+a_3+a_4+a_5+a_6+a_7\right)}{7}-\frac{\left(b_1+b_2+b_3+b_4+b_5+b_6+b_7\right)}{7}=214.29$$

Hence A- B = 214.29 * 7 = 1500

Similarly, all the remaining differences in sales can be calculated

Let the sales of A in 2013 be 'a', C in 2010 be 'c', D in 2012 be 'd' .

Total sales of A = (6800+a)

B = 5800

C = (7400+c)

D = (5700+d)

E = 7000

A - B = 6800+a - 5800 = 1500 => a = 500 crores

B - C = 5800 - 7400 - c = -2400 => c = 800 crores

D - E = 5700 + d - 7000 = -700 => d = 600 crores

Hence C is the correct answer.

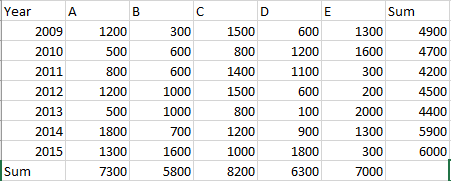

Annual sales average of all products is the least in which year?

Solution

On Tabulating the chart , we get

from the previous question value of a=500,c=800,d=600

The product having the least sales value will obviously have the least avg sales value

Sales in the year 2010=4700

Sales in the year 2011=4200

Sales in the year 2012=4500

Sales in the year 2013=4400

Hence in 2011 average of all the products sold is the least

So B is the correct answer

Which product has the least average sales for the seven year period 2009-15?

Solution

On Tabulating the chart , we get

Since difference in average sales is given

Difference in sales can be found out by multiplying it by 7

Let the sales of A in 2013 be a , C in 2010 be c, d in 2012 be d

Total sales of A = (6800+a)

B = 5800

C = (7400+c)

D = (5700+d)

E = 7000

On evaluating we get value of a = 500,c=800,d= 600 crores

Sales of product A = 7300

Sales of product B = 5800

Sales of product D = 6300

Sales of product E = 7000

Product B has the least average sales.

Hence B is the correct answer.

The difference between average sales of products for the period 2009-15 is the least for which pair of products?

Solution

On Tabulating the chart , we get

Since difference in average sales is given

Difference in sales can be found out by multiplying it by 7

Let the sales of A in 2013 be a , C in 2010 be c, d in 2012 be d

Total sales of A = (6800+a)

B = 5800

C = (7400+c)

D = (5700+d)

E = 7000

On evaluating we get value of a = 500,c=800,d= 600 crores

On substituting all the values in the tables ,

Option A: The difference between the average sales of products A and B = 7300-5800 = 1500

Option B: The difference between the average sales of products B and C = 8200 - 5800 =2400

Option C: The difference between the average sales of products C and D= 8200 - 6300 = 1900

Option D: The difference between the average sales of products D and E= 7000 - 6300 = 700

The difference between the average sales of products D and E is the least.

Hence option D is the correct answer.

If Year on Year (YoY) Growth is

{Current Year Sales − Previous Year Sales }/ Previous Year Sales

then the YoY growth of combined sales of all products has suffered maximum decline in which year?

Solution

Let's tabulate the chart ,

Since difference in average sales is given , Difference in sales can be found by multiplying it by 7

Let the sales of A in 2013 be 'a', C in 2010 be 'c', D in 2012 be 'd' .

Total sales of A = (6800+a*1000

B = 5800

C = (7400+c)

D = (5700+d)

E = 7000

On evaluating we get value of a = 500,c=800,d= 600 crores

On finding the unknown values , we get the below table

Let's evaluate the options one by one,

Option A: YoY growth of combined sales of all products in 2010 = 4700-4900/4900 = -0.0408

Option B: YoY growth of combined sales of all products in 2011 = 4200-4700/4700 = -0.1064

Option C: YoY growth of combined sales of all products in 2013 = 4400-4500/4500 = -0.0222

Option D: YoY growth of combined sales of all products in 2015 = 6000-5900/5900 = 0.0169

Among the above values, it is clear that the YoY growth of combined sales of all products in 2011 had a maximum decline.

Hence B is the correct answer.

Read the following information and graph and answer the questions that follow.

An international Organisation produces a Competitive Index of countries every two years based on eight factors (Institutions, Infrastructure, Macroeconomic Environment, Higher Education, Market Efficiency, Technological Readiness, Business Sophistication and Innovation). The last three indices were developed in 2010, 2012 and 2014. The scores for all eight factors of XYZ country are shown in the graph below:

If Factor performance is measured as 0.30 × Factor Score in 2014 + 0.35 × Factor Score in 2012 + 0.35 × Factor Score in 2010, then which of the following has best Factor Performance?

Solution

Factor performance is measured as 0.30 × Factor Score in 2014 + 0.35 × Factor Score in 2012 + 0.35 × Factor Score in 2010

Let's calculate Factor performance for each of the given options.

Factor performance For Innovation = 0.3*4.5+0.35*4+0.35*4.75 = 4.4125

Factor performance for Business Sophistication =0.3*5.25+0.35*4.75+0.35*4.5=4.8125

Factor performance for Infrastructure = 0.3*5.25+0.35*4+0.35*4 = 4.375

Factor performance for Macroeconomic Environment =0.3*5.5+0.35*4.5+0.35*4.75 = 4.8875

Factor performance for Macroeconomic Environment is the highest.

Hence option D is the correct answer.

If Factor Performance is measured as

$$\frac{ \text {Factor Score 2014 - Factor Score 2012 }}{ \text{Factor Score 2010}}$$

then which of the following has best Factor Performance?

Solution

Factor performance in Innovation = $$\dfrac{4.5 - 4}{4.75}\times 100$$ = 10.53

Factor performance in Business Sophistication = $$\dfrac{5.25 - 4.75}{4.5}\times 100$$ = 11.11

Factor performance in Infrastructure = $$\dfrac{5.25 - 4}{4}\times 100$$ = 31.25

Factor performance in Macroeconomic Environment = $$\dfrac{5.5 - 4.5}{4.75}\times 100$$ = 21.05

We can see that option C is the correct answer.

Which of the following factors has the highest average score across indices of 2010, 2012 and 2014?

Solution

For Infrastructure

Average of the indices = 4+4+5.25/3=13.25/3

=4.4167

For Institutions

Average of the indices =4.25+4.75+4.5/3=13.5/3

=4.5

For Technological readiness

Average of the indices =3.5+3.75+5.5/3=12.75/3

=4.25

For Market Efficiency

Average of the indices =4.25+4.5+4.25/3=13/3

=4.33

The average of the index is highest for Institutions.

Hence B is the correct answer.

Which among the following factors had the least growth rate in 2014 versus scores of 2010?

Solution

The growth rate in 2014 versus scores of 2010 for Business Sophistication =5.25/4.5 = 1.167

Growth rate in 2014 versus scores of 2010 for Institutions = 4.5/4.25 = 1.058

Growth rate in 2014 versus scores of 2010 for Technological Readiness = 5.5/3.5 = 1.571

Growth rate in 2014 versus scores of 2010 for Infrastructure = 5.25/4 = 1.3125

Among the above values, growth rate for institutions was least.

Hence B is the correct answer.

Read the following information and the accompanying graphs to answer the questions that follow.

www.jay.com spent $ 5,57,000 during last 12 months for online display advertisements, also called impressions, on five websites (Website A, Website B, Website C, Website D and Website E). In this arrangement, www.jay.com is the Destination Site, and the five websites are referred to as the Ad Sites. The allocation of online display advertising expenditure is shown in Graph A. The online display advertisements helped www.jay.com to get visitors on its site. Online visitors, visiting the Ad Sites, are served display advertisements of www.jay.com and on clicking they land on the Destination Site (Graph B). Once on the Destination Site, some of the visitors complete the purchase process(Graph C)

Quality traffic = $$\frac{\text{No. of site visitors who start purchase on destination site}}{\text{No. of visitors who click the online display advertisement}}$$

Leakage in online buying = 1 − $$\frac{\text {Complete buying on the destination website}}{\text{Start buying on the destination website}}$$

Efficiency of online display advertising expenditure on an Ad Site = $$\frac{\text{No. of visitors from the Ad Site who complete the purchase process}}{\text{Amount spent on the Ad Site}}$$

Which of following Ad Sites provide facility of least cost per advertisement?

Solution

Let's calculate the Cost per advertisement by using the formula

Cost per advertisement = Advertising expenditure / Impressions made

For website A= 557000 * 0.27/ 240 = 626.625

For website B=557000 * 0.22 / 370 = 331.19

For website D=557000 * 0.13 / 300 = 219.42

For website E=557000*0.20 / 150 = 742.67

So the least cost per advertisement is for Website D.

Hence C is the correct answer.

Which Ad Site has provided maximum quality traffic?

Solution

Let's calculate the Quality traffic using the formula,

Quality traffic =

For Website A = 2800/120k = 23.33 x 10^(-3)

For Website B = 2500/ 60k = 41.67 x 10^(-3)

For Website D = 3000 / 80k = 37.50 x 10^(-3)

For Website E = 3500 / 40k =87.50 x 10^(-3)

The quality traffic for website E is the maximum.

Hence D is the correct answer.

Which Ad Site sent traffic to www.jay.com with maximum leakage?

Solution

Let's calculate the Leakage in online buying by using the formula,

Leakage in online buying = 1 − Complete buying on the destination websiteStart buying on the destination website\frac{\text {Complete buying on the destination website}}{\text{Start buying on the destination website}}

For Website B = 1-(1200/2500)= 0.52

For Website C = 1-(900/2000)= 0.55

For Website D = 1-(1300/3000)= 0.5667

For Website E = 1-(1600/3500)= 0.5428

For Website D the leakage is maximum .

Hence C is the correct answer.

On which Ad Site is the advertising budget spent most efficiently?

Solution

Website A : 2700/150390 = 0.0179

Website B : 1200/122540 = 0.009

Website C :900/100260 = 0.0089

Website E :1600/111400 = 0.014

Hence for website A the advertising budget was spent efficiently

Read the following passages carefully and answer the questions given at the end of each passage

Because of the critical role played by steel in economic development, the steel industry is often considered, especially by the governments, which traditionally owned it, to be an indicator of economic prowess. World production has grown exponentially, but there were big highs and equally big lows all through the 1990s and up to 2002. Recovery from the two World Wars and the Great Depression of the 1930s caused massive disruption and lay-offs. Over-capacity and low steel prices continued to play havoc through the 1970s and 1980s and politicians began to lose their belief that the wealth of a nation was directly coupled to its steel production.

This led to a wave of privatisations, as state-owned enterprises shed their financial liabilities to hungry capitalists. A whole new breed of steel-makers came into being using a new technology, the mini-mill. This used a smaller electric-arc furnace fed that just melts down ‘cold’ scrap. It was a cheaper process than the traditional ‘hot metal integrated mills’ with their mountains of ore and coal and monumental machinery, but it was used almost exclusively for lower-grade building and other ‘long’ products.

By the beginning of 2005, the world steel industry was on a high, after decades of moving from apocalypse to break-even and then back to apocalypse. Since 2003, when a staggering 960 million tonnes were produced-compared to 21.9 million tonnes for aluminium-there had been unprecedented demand, mainly from China and India. China was both the biggest producer, the first country to exceed 200 million tonnes of crude steel in a year, and also its biggest consumer at 244 million tonnes. The global economy was also booming, but this was creating production bottlenecks for all steel-makers and by 2004 steel had for the first time hit an average of $650 per tonne shipped. Profit margins were better, but where was the growth to come from? In tandem, the costs of essential raw materials for steel-making - iron ore coking coal-had gone through the roof, along with bulk shipping costs. The key to future growth was to secure plants in emerging markets where ore and coal were close to production sites, labour costs were much lower and where technology and investment could spur greater savings.

But the central issue was that globally the industry remained a very fragmented one. No single company was producing 100 million tonnes a year, or 10 per cent of total world production. The name of the game was consolidation into fewer, bigger players. With this would come the chance for steel-makers to gain greater pricing power, increasing their profitability and the value of their shares.

Two groups had begun to move ahead of the pack. One was Mittal Steel with its operational headquarters in London’s prestigious Berkeley Square. Mittal Steel was the world’s biggest producer of ‘long’ products. It was young, aggressive, fast, and a big risk-taker, fuelled by its founder Lakshmi Mittal’s visionary zeal to consolidate the industry. Its nearest rival, Arcelor - the world’s most profitable steel company, focusing on ‘flat’ products - was headed by the Frenchman Guy Dolle, and was a combination of three former state-owned European steel plants: Arbed of Luxembourg, Usinor from France and Spain’s Aceralia. These three were now merged, restructured and administered from the grandiose, chateau-like former Arbed headquarters in Luxembourg’s Avenue de la Liberte.

Both groups were passionate about steel. Mittal, already dubbed ‘the Carnegie from Calcutta’, had a clearer vision of the need to streamline steel, but Arcelor was determined to become the biggest as well as the best. Dominating the market would enable either firm to increase its pricing position with customers, the car-makers, ship-builders and construction firms, as well as chasing growth in the new markets of Asia, South America and Eastern Europe.

Guy Dolle could hear the clump of Mittal’s feet marching ahead, and it hurt. Arcelor was Europe’s reigning steel champion and was arrogantly proud of it. It had a commanding market share of the specialised high-strength steel supplied to European car-makers, and a total overall production approaching 50 million tonnes a year, all with state-of-the-art technology. The group had repaired its consolidated balance sheet, ravished by decades of downturns and continual restructuring costs. It had invested heavily in the quest for best technology and had also acquired companies in Brazil, set up joint ventures in Russia, Japan and China and now was eagerly eyeing gateways to the North American car market. And to its long-suffering shareholders, starved of decent dividends, Arcelor was at last moving in the right direction, after the blood, sweat and tears of shifting from public to private sector. The Luxembourg group was clearly on a wake-up call, gunning to overtake Mittal Steel and keep it at bay.

By 2005, the battle for supremacy had begun to heat up. Two projected state sell-offs by public auction, in Turkey and Ukraine, were particularly attractive commercially. Both auctions were taking place in October, within three weeks of each other. The first, in Turkey, was for the 46.3 percent of government-owned shares in Erdemir, a steel-maker producing 3.5 million tonnes a year for car-makers and other industrial clients in a country of seventy million people shaping up to join the European Union. Mittal and Arcelor both already owned minitory stakes in the Turkish company and were eager to get majority control.

Which of the following statements is true?

Solution

Option A: True, In the second paragraph " China was both the biggest producer, the first country to exceed 200 million tonnes of crude steel in a year, and also its biggest consumer at 244 million tonnes." Thus Option A is correct.

Option B: False, In the fifth paragraph "It’s nearest rival, Arcelor- the world’s most profitable steel company, focusing on ‘flat’ products-was headed by the Frenchman Guy Dolle" Arcelor was the world's most profitable steel company.

Option C: False, Never mentioned in the passage.

Option D: False

Which among the following is the common objective both Mittal and Arcelor had for aspiring to become bigger steel-makers?

Solution

In the passage it is given "Both groups were passionate about steel................ Dominating the market would enable either firm to increase its pricing position with customers, the car-makers, ship-builders and construction firms, as well as chasing growth in the new markets of Asia, South America and Eastern Europe. "

Thus both of them wanted to dominate the market to increase their pricing position with customers.

Hence D is the correct answer.

From the above passage, it clearly emerges that:

Solution

Option A is false as given in the passage " And to its long-suffering shareholders, starved of decent dividends, Arcelor was at last moving in the right direction, after the blood, sweat and tears of shifting from public to private sector." We can infer that Arcelor had not delivered good returns.

Option B is correct as throughout the latter half it is mentioned that Mittal and Arcelor were the only competitors in the market.

Option C is false as in the second paragraph it is given "By the beginning of 2005, the world steel industry was on a high, after decades of moving from apocalypse to break-even and then back to apocalypse. "

Option D cannot be inferred as "Over-capacity and low steel prices continued to play havoc through the 1970s and 1980s and politicians began to lose their belief that the wealth of a nation was directly coupled to its steel production."

What are the plausible reasons for privatization in steel industry?

Solution

From the first two paragraphs we can infer that privatization thrived because of the falling prices and overcapacity.

In the first paragraph "Recovery from the two World Wars and the Great Depression of the 1930s caused massive disruption and lay-offs. Over-capacity and low steel prices continued to play havoc through the 1970s and 1980s and politicians began to lose their belief that the wealth of a nation was directly coupled to its steel production." explained the reason for privatization of the steel industry which is given in the second paragraph

Hence Option C is correct.

Read the following passages carefully and answer the questions given at the end of each passage:

In the decades that Otlet’s papers had sat gathering dust, his dream of a universal knowledge of network had found a new expression across the Atlantic, where a group of engineers and computer scientists laid the groundwork for what would eventually become the Internet. Beginning during the Cold War, the United States poured money into a series of advanced research projects that would eventually lead to the creation of the technologies underpinning the present-day Internet. In 1990s, the World Wide Web appeared and quickly attracted a widespread audience, eventually establishing itself as the foundation of a global knowledge- sharing network much like the one that Otlet envisioned.

Today, the emergence of that network has triggered a series of dramatic - perhaps even “axial” - transformation. In 2011, the world’s population generated more than 1.8 zettabytes of data, including documents, images, phone calls, and radio and television signals. More than a billion people now use Web browsers, and that number will almost certainly increase for years to come. In an era when almost anyone with a mobile phone can press a few keys to search the contents of the world’s libraries, when millions of people negotiate their personal relationships via online social networks, and when institutions of all stripes find their operations disrupted by the sometimes wrenching effects of networks, it scarcely seems like hyperbole - and has even become cliché - to suggest that the advent of the Internet ranks as an event of epochal significance.

While Otlet did not by any stretch of imagination “invent” the Internet - working as he did in an age before digital computers, magnetic storage, or packet - switching networks - nonetheless his vision looks nothing short of prophetic. In Otlet’s day, microfilm may have qualified as the most advanced information storage technology, and the closest thing anyone had ever seen to database was a drawer full of index cards. Yet despite these analog limitations, he envisioned a global network of interconnected institutions that would alter the flow of information around the world, and in the process lead to profound social, cultural, and political transformations.

By today’s standards, Otlet’s proto-Web was a clumsy affair, relying on a patchwork system of index cards, file cabinets, telegraphs machines, and a small army of clerical workers. But in his writing he looked far ahead to a future in which networks circled the globe and data could travel freely. Moreover, he imagined a wide range of expression taking shape across the network: distributed encyclopaedias, virtual classrooms, three-dimensional information spaces, social networks, and other forms of knowledge that anticipated the hyperlinked structure of today’s Web. He saw these developments as fundamentally connected to a

larger utopian project that would bring the world closer to a state of permanent and lasting peace and toward a state of collective spiritual enlightenment.

The conventional history of the Internet traces its roots through an Anglo-American lineage of early computer scientists like Charles Babbage, Ada Lovelace, and Alan Turing; networking visionaries like Vinton G. Cerf and Robert E. Kahn; as well as hypertext seers like Vannevar Bush, J.C. R. Licklider, Douglas Engelbart, Ted Nelson, and of course Tim Berners-Lee and Robert Cailliau, who in 1991 released their first version of the World Wide Web. The dominant influence of the modern computer industry has placed computer science at the center of this story.

Nonetheless Otlet’s work, grounded in an age before microchips and semiconductors, opened the door to an alternative stream of thought, one undergirding our present-day information age even though it has little to do with the history of digital computing. Well before the first Web servers started sending data packets across the Internet, a number of other early twentieth- century figures were pondering the possibility of a new, networked society: H.G. Wells, the English science fiction writer and social activist, who dreamed of building a World Brain, Emanuel Goldberg, a Russian Jew who invented a fully functional mechanical search engine in 1930s Germany before fleeing the Nazis; Scotland’s Patrick Geddes and Austria’s Otto Neurath, who both explored new kinds of highly designed, propagandistic museum exhibits designed to foster social change; Germany’s Wilhelm Ostwald, the Nobel Prize-winning chemist who aspired to build a vast new ‘brain of humanity’; the sculptor Hendrik Andersen and the architect Le Corbusier, both of whom dreamed of designing a World City to house a new, one-world government with a networked information repository at its epicentre. Each shared a commitment to social transformation through the use of available technologies. They also each shared a direct connection to Paul Otlet, who seems to connect a series of major turning points in the history of the early twentieth-century information age, synthesizing and incorporating their ideas along with his own, and ultimately coming tantalizingly close to building a fully integrated global information network.

What is the remark that the author of this passage considers a defensible one, rather than a hyperbole?

Solution

Option A is presented as a straightforward observation, not a contested or exaggerated point.

Option B is mentioned that it scarcely seems like hyperbole - and has even become cliché - to suggest that the advent of the Internet ranks as an event of epochal significance.

Option C, similar to option A, is presented as a factual example of the Internet’s impact, not as a claim needing defense.

Option D is a simple statistic, and not a point of debate.

Hence, Option B would be the correct answer.

In the above passage, Otlet is being credited with

Solution

In third paragraph it is mentioned, 'While Otlet did not “invent” the Internet - working as he did in an age before digital computers, magnetic storage, or packet - switching networks - nonetheless his vision looks nothing short of prophetic.' Therefore, the answer is option C.

What has been said as the common commitment shared by the early twentieth-century figures who imagined and worked for a networked society?

Solution

In the last paragraph, it is mentioned, 'Each shared a commitment to social transformation through the use of available technologies.' Among the given options, option B is the appropriate one.

The answer is option B.

Otlet’s original idea of network can be described as:

Solution

Paragraph 4 talks about Otlet's idea being Futuristic, Visionary and Utopian. The answer is option D.

Read the following passages carefully and answer the questions given at the end of each passage:

Every loan has a lender and a borrower; both voluntarily engage in