Which of the following year exhibited highest percentage decrease over the preceding year in the automobile production?

IIFT 2009 Question Paper

Answer the questions based on the following graphs

Solution

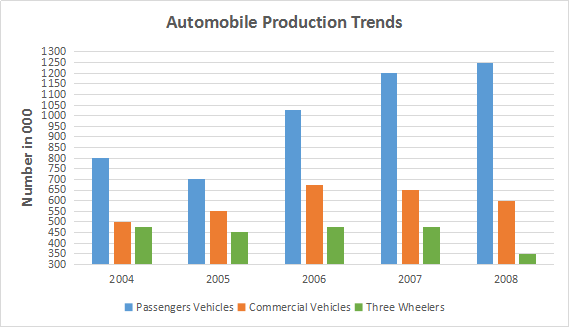

Total automobile production in the year 2004 = 800+500+475 = 1775

Total automobile production in the year 2005 = 700+550+450 = 1700

Total automobile production in the year 2006 = 1025+675+475 = 2175

Total automobile production in the year 2007 = 1200+650+475 = 2325

Total automobile production in the year 2008 = 1250+600+350 = 2200

We can see that production decreased only twice during the given period in the year 2005 and 2008.

Hence, the percentage decrease in the year 2005 over the year 2004 = $$\dfrac{1775-1700}{1775}\times 100$$ = 4.225 percent.

Similarly, the percentage decrease in the year 2008 over the year 2007 = $$\dfrac{2325-2200}{2325}\times 100$$ = 5.376 percent.

Therefore, we can say that option D is the correct answer.

Assume whatever that is not sold domestically was exported, then which year has registered highest growth in exports of automobiles?

Solution

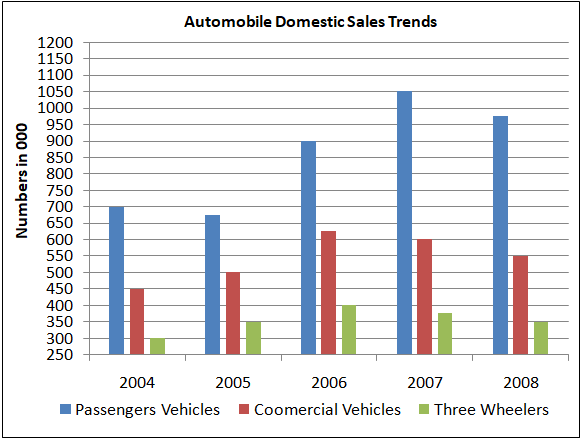

Total automobile production exported in the year 2004 = (800+500+475)-(700+450+300) = 325

Total automobile production exported in the year 2005 = (700+550+450)-(675+500+350) = 175

Total automobile production exported in the year 2006 = (1025+675+475)-(900+625+400) = 250

Total automobile production exported in the year 2007 = (1200+650+475)-(1050+600+375) = 300

Total automobile production exported in the year 2008 = (1250+600+350)-(975+550+350) = 325

From the data itself we can see that highest growth occurred in the year 2006.

Therefore, we can say that option B is the correct answer.

If the ratio of the domestic sale price of a commercial vehicle, a passenger vehicle, and a three wheeler is 5 : 3 : 2 then what percent of earnings (approximately) is contributed by commercial vehicle segment to the overall earnings from domestic sales during the period 2004-2008?

Solution

Total commercial vehicles sold from the year 2004 to 2008 = 450+500+625+600+550 = 2725

Total passenger vehicles sold from the year 2004 to 2008 = 700+675+900+1050+975 = 4300

Total three wheelers sold from the year 2004 to 2008 = 300+350+400+375+350 = 1775

Hence, the percent of earnings is contributed by commercial vehicle segment alone = $$\dfrac{5*2725}{5*2725+3*4300+2*1775}\times 100$$ = 45.30 % $$\approx$$ 45%.

Hence, option A is the correct answer.

For which year were the domestic sales of automobiles closest to the average (2004-2008) domestic sales of automobiles?

Solution

Total domestic sales of automobiles in the year 2004 = (700+450+300) = 1450

Total domestic sales of automobiles in the year 2005 = (675+500+350) = 1525

Total domestic sales of automobiles in the year 2006 = (900+625+400) = 1925

Total domestic sales of automobiles in the year 2007 = (1050+600+375) = 2025

Total domestic sales of automobiles in the year 2008 = (975+550+350) = 1875

Average domestic sales of automobiles for the given period = $$\dfrac{1450+1525+1925+2025+1875}{5}$$ = 1760.

Hence, we can say that the domestic sales in the year 2008 is the closest to the average domestic sales. Hence, option D is the correct answer.

Which of the following years exhibited highest percentage increase over the preceding year in the automobile sales?

Solution

Total domestic sales of automobiles in the year 2004 = (700+450+300) = 1450

Total domestic sales of automobiles in the year 2005 = (675+500+350) = 1525

Total domestic sales of automobiles in the year 2006 = (900+625+400) = 1925

Total domestic sales of automobiles in the year 2007 = (1050+600+375) = 2025

Total domestic sales of automobiles in the year 2008 = (975+550+350) = 1875

We can see that the automobiles sales rose by the highest amount in the year 2006 as compared to other years. Also, the base is relatively smaller for remaining year except 2004. But the absolute growth is much higher in the year 2006 as compared to the year 2005. Hence, option B is the correct answer.

The ratio between absolute increase in domestic sales over preceding year and absolute increase in production over the preceding year is highest during which year?

Solution

Total automobile production in the year 2004 = 800+500+475 = 1775

Total automobile production in the year 2005 = 700+550+450 = 1700

Total automobile production in the year 2006 = 1025+675+475 = 2175

Total automobile production in the year 2007 = 1200+650+475 = 2325

Total automobile production in the year 2008 = 1250+600+350 = 2200

Total domestic sales of automobiles in the year 2004 = (700+450+300) = 1450

Total domestic sales of automobiles in the year 2005 = (675+500+350) = 1525

Total domestic sales of automobiles in the year 2006 = (900+625+400) = 1925

Total domestic sales of automobiles in the year 2007 = (1050+600+375) = 2025

Total domestic sales of automobiles in the year 2008 = (975+550+350) = 1875

In the year 2005 and 2008 the production and sales respectively are not increasing absolutely. Hence, we will check only for the year 2006 and 2007.

The ratio between absolute increase in domestic sales in the year 2006 over the year 2005 and absolute increase in production in the year 2006 over the year 2005 = $$\dfrac{1925-1525}{2175-1700}$$ = 0.84

Similarly, the required ratio for year 2007 = $$\dfrac{2025-1925}{2325-2175}$$ = 0.66

Hence, we can say that the ratio is the highest for the year 2006. Therefore, option B is the correct answer.

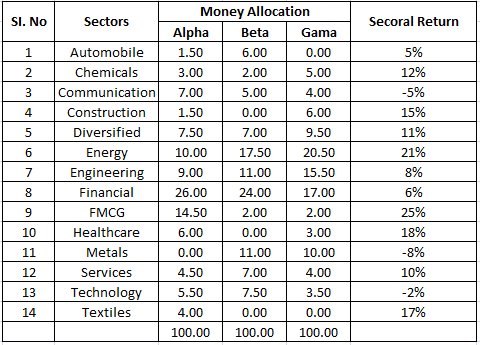

Answer the questions based on the following information.

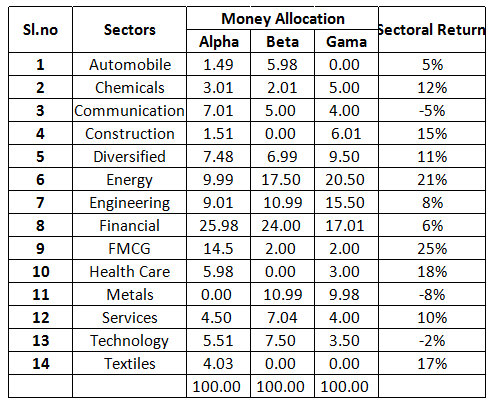

The table below gives the details of money allocation by three Mutual funds namely, Alpha, Beta, and Gama. The return for each fund depends on the money they allocate to different sectors and the returns generated by the sectors. The last column of the table gives return for each of the sectors for a one year period.

Which fund has received more return per rupee of investment for one year period?

Solution

As the numbers are far apart we can approximate the money allocation data to the nearest multiple of 0.5. The money allocation data can be approximated as below.

Let us assume that Rs. 100 is invested in each fund.

Total return on investing Rs. 100 in fund Alpha =

1.5*1.05+3*1.12+7*.95+1.5*1.15+7.5*1.11+10*1.21

+9*1.08+26*1.06+14.5*1.25+6*1.18+4.5*1.10+5.5*.98+4*1.17 = Rs. 111.24.

Hence, net return per rupee in fund Alpha = $$\dfrac{111.24}{100}$$ = Rs. 1.1124.

Similarly, we can calculate total return on investing Rs. 100 in fund Beta and Gama.

Net return per rupee in fund Beta = $$\dfrac{107.225}{100}$$ = Rs. 1.07225.

Net return per rupee in fund Gama = $$\dfrac{109.48}{100}$$ = Rs. 1.0948.

We can see that return per rupee is the highest for Alpha fund. Hence, option A is the correct answer.

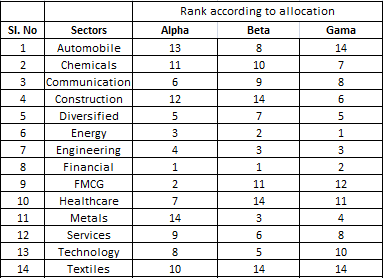

If the allocation of money by the fund managers to different sectors is based on the internal ranking (i.e. Sector with 1st rank gets highest allocation). Sectors with 0 allocation of money should be considered as 14th rank irrespective of the number of sectors in that category. In the light of these examine the following

statements:

I. Automobile is ranked by both Alpha and Beta as same

II. Financial is most favoured by all three Mutual Funds

III. Services is ranked by all three Mutual Funds within top 9 ranks

Select the best option:

Solution

Let us tabulate the ranks of various sectors according to fund allocation.

Statement I : Automobile is ranked by both Alpha and Beta as same. This statement is incorrect.

Statement II : Financial is most favoured by all three Mutual Funds. This statement is incorrect as Energy sector is most favored by fund Gama.

Statement III : Services is ranked by all three Mutual Funds within top 9 ranks. We can see that this statement is correct. Hence, option D is the correct answer.

Ms. Hema invested Rs. 10.00 lakhs in fund Gama in the beginning of the period. What will be the value of the investment at the end of 1 year period?

Solution

As the numbers are far apart we can approximate the money allocation data to the nearest multiple of 0.5. The money allocation data can be approximated as below.

Total return on investing Rs. 100 in fund Gama =

5*1.12+4*.95+6*1.15+9.5*1.11+20.5*1.21+15.5*1.08

+17*1.06+2*1.25+3*1.18+10*.92+4*1.1+3.5*.98 = Rs. 109.48.

Hence, total return of an investment of 10 lakhs in fund Gama after a year = $$\dfrac{109.48}{100}*10$$ = 10.948 lakhs $$\approx$$ 10.95 lakhs.

Hence, option B is the correct answer.

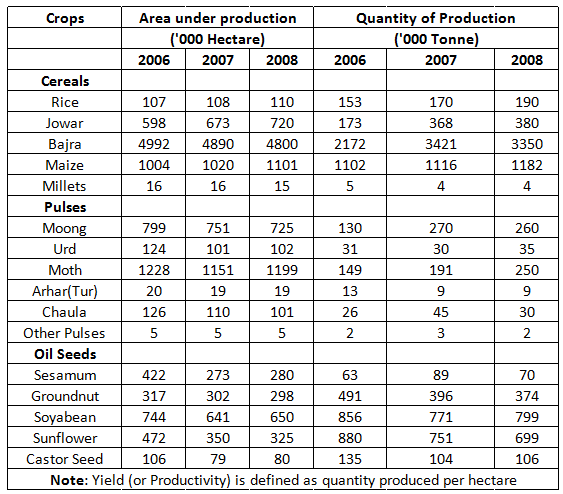

Answer the questions based on the following Table

What is the ratio between Jowar yield (2007) and Soyabean yield (2008)?

Solution

Jowar's yield in the year 2007 = $$\dfrac{368}{673}$$ $$\approx$$ 0.55

Soyabean's yield in the year 2008 = $$\dfrac{799}{650}$$ $$\approx$$ 1.23

Hence, the required ratio = 0.55 : 1.23 = 0.445 : 1 or 0.89: 2.00

Therefore, option C is the correct answer.

Top 3 crops by yield in the year 2006 are:

Solution

Caster Seed's yield in the year 2006 = $$\dfrac{135}{106}$$ = 1.273

Groundnut's yield in the year 2006 = $$\dfrac{491}{317}$$ = 1.55

Maize's yield in the year 2006 = $$\dfrac{1102}{1004}$$ = 1.097

Sunflower's yield in the year 2006 = $$\dfrac{880}{472}$$ = 1.864

Rice's yield in the year 2006 = $$\dfrac{153}{107}$$ = 1.429

Bazra's yield in the year 2006 = $$\dfrac{2172}{4992}$$ =0.435

Top 3 yields in 2006: Sunflower,Groundnut,Rice

Bottom 3 crops by yield in the year 2008 are:

Solution

Moth's yield in the year 2008 = $$\dfrac{250}{1199}$$ = 0.2083

Sesamum's yield in the year 2008 = $$\dfrac{70}{280}$$ = 0.25

Millets's yield in the year 2008 = $$\dfrac{4}{15}$$ = 0.266

Moong's yield in the year 2008 = $$\dfrac{260}{725}$$ = 0.358

Arhar's yield in the year 2008 = $$\dfrac{9}{19}$$ = 0.474

Urd's yield in the year 2008 = $$\dfrac{35}{102}$$ = 0.343

Chaula's yield in the year 2008 = $$\dfrac{30}{101}$$ = 0.297

Bottom 3 yields in 2008: Moth, Sesamum, Millets

Examine the following statements:

I. Total productivity of pulses has gone down over the years

II. Maize is the most stable cereal in terms of productivity over the years

III. Percentage growth in area and quantity of production is highest in the case of Jowar during the entrie period.

Select the best option:

Solution

Productivity is defined as total production per hectare.

Total productivity of pulses in the year 2006 = $$\frac{130+31+149+13+26+2}{799+124+1228+20+126+5}$$ = $$0.1524$$

Total productivity of pulses in the year 2007 = $$\frac{270+30+191+9+45+3}{751+101+1151+19+110+5}$$ = $$0.2564$$

Total productivity of pulses in the year 2008 = $$\frac{260+35+250+9+30+2}{725+102+1199+19+101+5}$$ = $$0.2724$$

We can see that clearly, Total productivity of pulses in the year 2008 > Total productivity of pulses in the year 2007 >Total productivity of pulses in the year 2006. Hence, statement I is incorrect. Hence, we can reject option A and B.

Productivity of Maize in the year 2006 = $$\dfrac{1102}{1004}$$ = 1.097

Productivity of Maize in the year 2007 = $$\dfrac{1116}{1020}$$ = 1.094

Productivity of Maize in the year 2008 = $$\dfrac{1182}{1101}$$ = 1.073

We can see that productivity is approximately same during the given period for Maize. Hence, statement II is correct. Therefore, we can reject option D.

Thus, we can say that option C is the correct answer.

Examine the following statements:

I. Over the period total cereal productivity has gone up

II. Area, Production and yield of the total oil seeds is on decline

III. Though there is a decline in the area under Urd production but the quantity of production and yield has gone up over the years.

Select the best option:

Solution

Productivity is defined as total production per hectare.

Total productivity of cereals in the year 2006 = $$\frac{153+173+2172+1102+5}{107+598+4992+1004+16}$$ = $$0.5366$$

Total productivity of cereals in the year 2008 = $$\frac{190+380+3350+1182+4}{110+720+4800+1101+15}$$ = $$0.756$$

We can see that clearly, Total productivity of cereals in the year 2008 > Total productivity of cereals in the year 2006. Hence, statement I is correct.

Now let us check statement II.

Total yield of oil seeds in the year 2006 = $$\frac{63+491+856+880+135}{422+317+744+472+106}$$ = $$1.1766$$

Total yield of oil seeds in the year 2008 = $$\frac{70+374+799+699+106}{280+298+650+325+80}$$ = $$1.254$$

We can see that yield of Oil seeds is not on decline. Hence, statement II is incorrect.

Now let us check statement III.

Area under Urd production in the year 2006 = 124

Area under Urd production in the year 2008 = 102

Total Urd production in the year 2006 = 31

Total Urd production in the year 2008 = 35

Urd's yield in the year 2006 = $$\frac{31}{124}$$ = 0.25

Urd's yield in the year 2008 = $$\frac{35}{102}$$ = 0.34

Hence, we can say that statement III is correct. Therefore, option A is the correct answer.

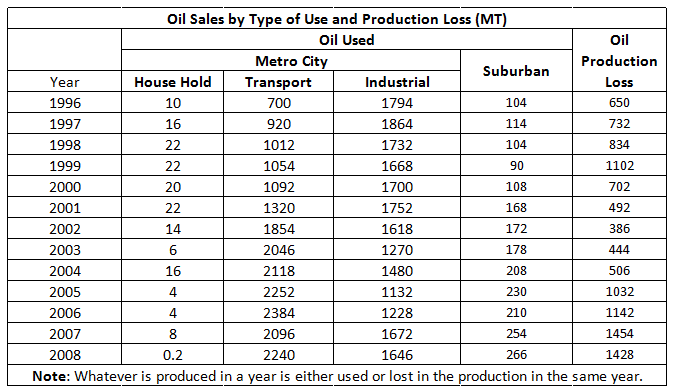

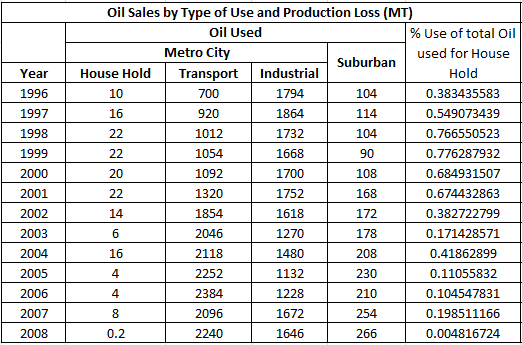

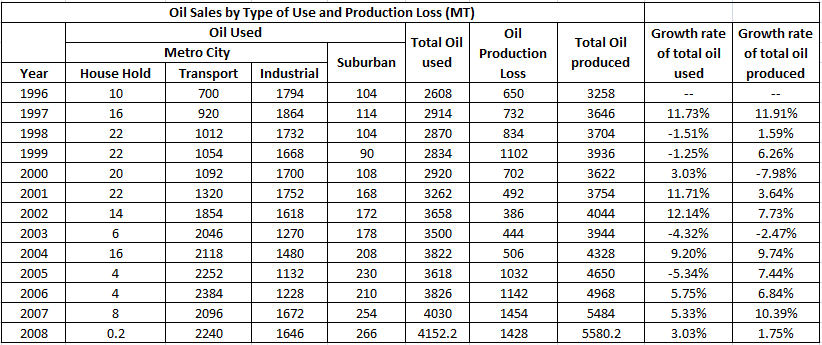

Study the following carefully and answer the questions.

During which year the Oil used for House Hold as a percentage of Total Oil Used is highest?

Solution

Total Oil used in the year 1998 = 22+1012+1732+104 = 2870.

Therefore, the percentage of total used that is used for House Hold = $$\frac{22}{2870}\times 100$$ = 0.766.

Similarly we can calculate for remaining year.

From the table we can see that, in the year 1999 the Oil used for House Hold as a percentage of total Oil Used is highest. Hence, option B is the correct answer.

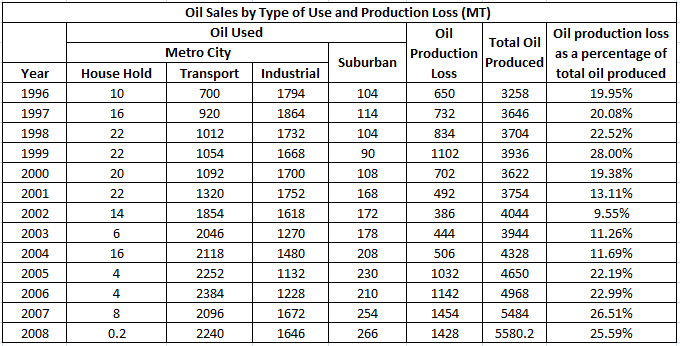

During which year the ‘Oil Production Loss’ as a proportion of ‘Total Oil Produced’ is the lowest?

Solution

Total oil produced in the year 1996 = 10+700+1794+104+650 = 3258.

Therefore, oil production loss as a percentage of total oil produced in the year = $$\dfrac{650}{3258}\times 100$$ = 19.95%.

Similarly, we can calculate for the remaining year. Tabulating the same data,

From the table, we can see that the oil production loss as a percentage of total oil produced is the lowest for the year 2002. Hence, option A is the correct answer.

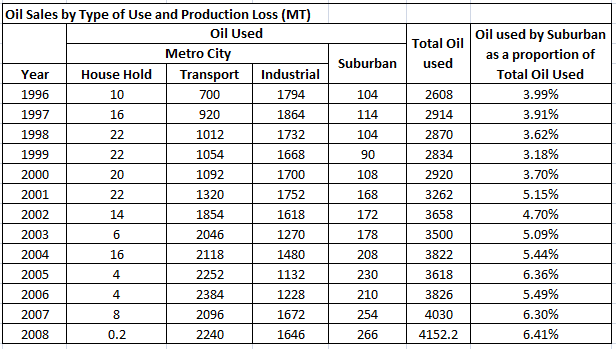

During which year use of oil by ‘Suburban’ as a proportion of ‘Total Oil Used’ was the highest?

Solution

Total oil used in the year 1996 = 10+700+1794+104 = 2608.

Therefore, Oil used by Suburban as a proportion of Total Oil Used = $$\dfrac{104}{2608}\times 100$$ = 3.99 percent.

Similarly, we can calculate for the remaining years.

From the table, we can see that oil used by suburban as a proportion of total oil used is the highest for the year 2008. Hence, option D is the correct answer.

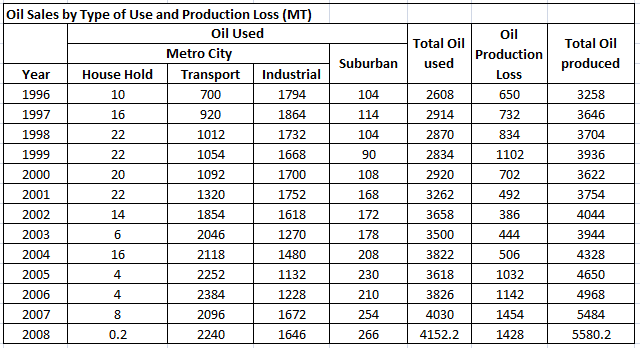

For how many number of years the growth rate in ‘Production of Oil’ is more than the growth rate in ‘Total Oil Used’?

Solution

Total oil used in the year 1996 = 10+700+1794+104 = 2608.

Total oil produced in the year 1996 = 10+700+1794+104+650 = 3258.

Similarly, we can calculate for the remaining quantities for both the years. Tabulating the same data,

Therefore, growth rate of total oil used in the year 1997 as compared to 1996 = $$\dfrac{2914-2608}{2608}\times 100$$ = 11.73%

Therefore, growth rate of total oil produced in the year 1997 as compared to 1996 = $$\dfrac{3646-3258}{3258}\times 100$$ = 11.91%

Similarly, we can calculate for the remaining year. Tabulating the same data,

From the table we can see that, the growth rate in ‘Production of Oil’ is more than the growth rate in ‘Total Oil Used’ in eight years.

{Year 1996, 1997, 1998, 2003, 2004, 2005, 2006, 2007}. Hence, option D is the correct answer.

Which of the below statements are true, based on the data in the above table?

Solution

Total oil used in the year 1996 = 10+700+1794+104 = 2608.

Total oil produced in the year 1996 = 10+700+1794+104+650 = 3258.

Similarly, we can calculate for the remaining quantities for both the years. Tabulating the same data,

From the table, we can see that quantity of 'total oil Produced’ is increasing every year since 2003. Hence, option D is the correct answer.

Study the following information carefully and answer the questions.

Four houses Blue, Green, Red and Yellow are located in a row in the given order. Each of the houses is occupied by a person earning a fixed amount of salary. The four persons are Paul, Krishna, Laxman, and Som.

Read the following instruction carefully:

I. Paul lives between Som and Krishna

II. Laxman does not stay in Blue house

III. The person living in Red house earns more than that of person living in Blue

IV. Salary of Som is more than that of Paul but lesser than that of Krishna

V. One of the person earns Rs. 80, 000

VI. The person earning Rs. 110,000 is not Laxman

VII. The salary difference between Laxman and Som is Rs. 30,000

VIII. The House in which Krishna lives is located between houses with persons earning salaries of Rs. 30,000 and Rs. 50,000

IX. Krishna does not live in the Yellow House, and the person living in the Yellow House is not earning the lowest salary among the four persons.

Who lives in Red house?

Solution

The first point tells us that "Paul lives between Som and Krishna".

This gives us an initial thought that these three can occupy the houses 1, 2, 3 in the row with Paul occupying the 2nd house and Som and Krishna sharing houses 1 and 3 in no particular order. In this case Laxman has to occupy the 4th house, i.e. the Yellow house. OR they can occupy the houses 2,3,4 with Paul occupying the 3rd house and Som and Krishna sharing houses 2 and 4 in no particular order. In this case Laxman has to occupy the 1st house, i.e. the Blue house.

However, since we know from point (II) that Laxman does not stay in the Blue house we reject this possibility.

Consequently, we can fix the position of Paul and Laxman in the Green and Yellow houses respectively.

At this point if we use point (VIII), we see that since ԋrishna lives in between two houses he cannot be in the first house. Hence, Krishna takes the third house and Som takes the 1st one.

Thus, the grid converts to:

From this point we need to focus on fixing the values of the salaries of the 4 individuals.

The values of the four salaries can first be identified as 30000, 50000 (from point VIII), 80000 ( point ) and 110000 (point VI). We also know from Point VIII that Krishna lives between the people

earning 30000 and 50000 which means that 30000 and 50000 could be Laxman and Paul's salary.

Further, the salary difference between Laxman and Som being 30000, their salaries would have to be 50000 and 80000, with Laxman getting 50000 and Som getting 80000. Consequently Paul gets 30000 and Krishna would earn 110000. The solution grid would then look like below:

So Krishna lives in Red house

Which house is occupied by person earning highest salary?

Solution

The first point tells us that "Paul lives between Som and Krishna".

This

gives us an initial thought that these three can occupy the houses 1,

2, 3 in the row with Paul occupying the 2nd house and Som and Krishna

sharing houses 1 and 3 in no particular order. In this case Laxman has

to occupy the 4th house, i.e. the Yellow house. OR they can occupy the

houses 2,3,4 with Paul occupying the 3rd house and Som and Krishna

sharing houses 2 and 4 in no particular order. In this case Laxman has

to occupy the 1st house, i.e. the Blue house.

However, since we know from point (II) that Laxman does not stay in the Blue house we reject this possibility.

Consequently, we can fix the position of Paul and Laxman in the Green and Yellow houses respectively.

At this point if we use point (VIII), we see that since ԋrishna lives in between two houses he cannot be in the first house. Hence, Krishna takes the third house and Som takes the 1st one.

Thus, the grid converts to:

From this point we need to focus on fixing the values of the salaries of the 4 individuals.

The

values of the four salaries can first be identified as 30000, 50000

(from point VIII), 80000 ( point ) and 110000 (point VI). We also know

from Point VIII that Krishna lives between the people

earning 30000 and 50000 which means that 30000 and 50000 could be Laxman and Paul's salary.

Further,

the salary difference between Laxman and Som being 30000, their

salaries would have to be 50000 and 80000, with Laxman getting 50000 and

Som getting 80000. Consequently Paul gets 30000 and Krishna would earn

110000. The solution grid would then look like below:

Red house is occupied by person earning highest salary

What is the salary earned by person living in Green house?

Solution

The first point tells us that "Paul lives between Som and Krishna".

This

gives us an initial thought that these three can occupy the houses 1,

2, 3 in the row with Paul occupying the 2nd house and Som and Krishna

sharing houses 1 and 3 in no particular order. In this case Laxman has

to occupy the 4th house, i.e. the Yellow house. OR they can occupy the

houses 2,3,4 with Paul occupying the 3rd house and Som and Krishna

sharing houses 2 and 4 in no particular order. In this case Laxman has

to occupy the 1st house, i.e. the Blue house.

However, since we know from point (II) that Laxman does not stay in the Blue house we reject this possibility.

Consequently, we can fix the position of Paul and Laxman in the Green and Yellow houses respectively.

At this point if we use point (VIII), we see that since ԋrishna lives in between two houses he cannot be in the first house. Hence, Krishna takes the third house and Som takes the 1st one.

Thus, the grid converts to:

From this point we need to focus on fixing the values of the salaries of the 4 individuals.

The

values of the four salaries can first be identified as 30000, 50000

(from point VIII), 80000 ( point ) and 110000 (point VI). We also know

from Point VIII that Krishna lives between the people

earning 30000 and 50000 which means that 30000 and 50000 could be Laxman and Paul's salary.

Further,

the salary difference between Laxman and Som being 30000, their

salaries would have to be 50000 and 80000, with Laxman getting 50000 and

Som getting 80000. Consequently Paul gets 30000 and Krishna would earn

110000. The solution grid would then look like below:

Rs. 30,000 is earned by person living in green house .

For the following questions answer them individually

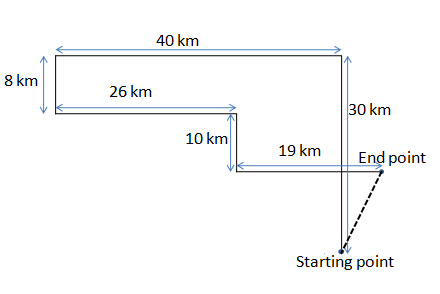

Mr Raghav went in his car to meet his friends John. He Drove 30 kms towards north and then 40 kms towards west. He then turned to south and covered 8 kms. Further he turned to east and moved 26 kms. Finally he turned right and drove 10 kms and then turned left to travel 19 kms. How far and in which direction is he from the starting point?

Solution

We can draw a direction diagram according to the problem statement.

Net displacement in the east direction = 26 + 19 - 40 = 5 km.

Net displacement in the north direction = 30 - 8 - 10 = 12 km.

Hence, net distance from the starting point = $$\sqrt{12^2+5^2}$$ = 13 km.

Therefore, option C is the correct answer.

Mr. Raju took the members of his family for a picnic. His father’s mother and mother’s father including each of their child were in one car. His father’s son and sister’s husband, brother’s wife were in second car. He along with his wife, wife’s sister, wife’s brother and son’s wife with a kid was in the third car. How many members of Mr. Raju’s family were there in the picnic and how many were left behind (assuming all members of the third generation are married and Raju had 2 grandparents in the family)?

Solution

In the first car - Raju's father, grandmother, mother and maternal grandfather - 4 members

In the second car - Raju's brother, sister-in-law, and brother-in-law - 3 members

In the third car - Raju, Raju's wife, sister-in-law, brother-in-law, daughter-in-law, grandson - 6 members

Total = (4 + 3 + 6) = 13

Members not present - Raju's sister, sister-in-law's husband, brother-in-law's wife, son - 4 members.

Hence, option A is the correct answer.

ABCDE play a game of cards. ‘A’ tells ‘B’ that if ‘B’ gives him five cards ‘A’ will have as many cards as ‘E’ has. However if A gives five cards to ‘B’ then ‘B’ will have as many cards as ‘D’. A and B together has 20 cards more than what D and E have together. B has four cards more than what C has and total number of cards are 201. How many cards B have?

Solution

Let 'a' be the number of cards with B. If A gives five cards to ‘B’ then ‘B’ will have as many cards as ‘D’.

Hence, the number of cards with D = 'a+5'.

B has four cards more than what C has. Hence, the number of cards with c = 'a-4'.

Let us assume that number of cards with A = 'x'. It is given that if ‘B’ gives 'A' five cards the A will have as many cards as ‘E’ has.

Hence, the number of cards with 'E' = x+5.

It is also given that A and B together has 20 cards more than what D and E have together.

Hence, (a+x) - (a+5+x+5) = 20.

Data given in the question contradicts with th information. Hence, this question can't be answer. Therefore, option D is the correct answer.

Ganesh Cultural Centre for promoting arts has appointed 3 instructors for music, dance, and painting. Music instructor takes session from 12 noon to 4:00 pm on Monday, Thursday and Sunday. The sessions of dance instructor are scheduled on Tuesday, Thursday, Wednesday and Sunday between 10:00 a to 2:00 pm. The 9:00 am to 12:00 noon slot on Tuesday, Friday and Thursday and also 2:00 pm to 4:00 pm slot on Wednesday, Saturday and Sunday is filled up by Painting Instructor. On which day(s) of a week the dance and painting sessions are simultaneously held?

Solution

According to the given information we can classify the working of instructors as :-

Music Instructor works from 12-4 pm on - Monday, Thursday and Sunday.

Dance Instructor works from 10 am-2 pm on - Tuesday, Wednesday, Thursday and Sunday

Painting Instructor works from -9 am - 12 noon on - Tuesday, Thursday and Friday

2 - 4 pm on - Wednesday, Saturday and Sunday

After this classification it is clear that Tuesday and Thursday are the days of the week the dance and painting sessions are simultaneously held.

Study the information given below and answer the questions.

The following table contains the pre and post revision pay structure of a Government department

The revision has been done based on the following terms:

-In pre-revised pay scale, the basic pay is the sum of the minimum pay in the appropriate pay scale and the admissible increment. After revision, the basic pay is the sum of minimum pay in the appropriate pay scale and the respective grade pay and the admissible increments.

-Annual increment of 3% of the basic pay (on a compounded basic) is paid under the revised pay rules.

-Monthly Dearness Allowance (DA) is calculated as percentage of basic pay.

-In pre-revised pay scales, the increment was given after the completion of each year of service, but, after revision annual increments are given only in the month of July every year and there should be a gap of six months between the increments.

The employees who had joined the department in the month of September, October, November and December are given an increment at the time of revised pay fixation in September, 2008.

The revised pay is applicable from 1st September, 2008.

Abhijit joins the department on November 10, 2006 in the pay scale of Rs. 18,400-500-22,400 with the pay of Rs. 18,400 plus 2 increments. What is his basic salary, after revision, on August 1, 2009?

Solution

Abhijit's revised minimum pay will be Rs. $$37400$$ and his grade pay will be Rs. $$10000$$.

Abhijit already had 2 increments and by 2009 will have 3 more. Thus, a total of 5 increments.

Thus his salary in 2009 = $$(37400+10000)\times (1.03)^5=54949.6\approx 54950$$

Hence, the answer is option C.

Nitin joined the department on November 24, 2004 in the pay scale of Rs. 8,000-275-13,500, at the minimum pay. At the time of pay revision, due to some error, his pay was fixed at the base (minimum) of the corresponding revised pay scale. The loss in his total emoluments for September 2008, due to this error, will be:

Solution

The new basic pay would have been = $$(15600+5400)(1.03)^4=23636$$

Due to the error, the pay is = $$15600+5400=21000$$

DA + HRA = $$28\% + 30\% = 58\%$$ of the basic pay

Thus, total loss in pay = $$1.58\times (23636-21000)=4164$$

Hence, the answer is option C.

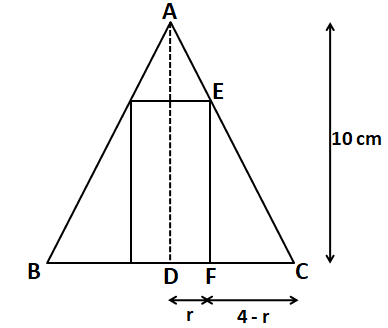

Sunitha joined the department at the basic pay of Rs. 13,500 in the pay scale of Rs. 12,000-16,500. On completion of her four years of service in December, 2008, she was promoted to the next higher pay scale, the percentage increase in her gross salary is:

Dinesh joined on July 1, 2008 in the pay scale of Rs. 16,400-20,000 at the basic pay of Rs. 16,850. On August 10, 2009, the department revised the rates of DA to 31% with effect from January, 2009 and further to 36% effective from July 2009. How much arrear will Dinesh get in August, 2009 because of these revisions?

Study the information given below and answer the questions.

A word arrangement machine, when given a particular input, rearranges it using a particular rule. The following is the illustration and the steps of the arrangement

INPUT: Smile Nile Style Mile Shine Wine Mine Swine Bovine Feline

STEP 1: Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

STEP 2: Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

STEP 3: Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

STEP 4: Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

STEP 5: Nile Smile Mile Style Wine Shine Swine Mine Feline Bovine

STEP 6: Nile Smile Mile Style Wine Shine Feline Bovine Swine Mine

STEP 7: Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

Which of the following will be step 14 for the given input:

Solution

Divide the whole sequence into group of words of 4, 2 and 4 so in the input the-

First group will be- Smile Nile Style Mile

Second group will be - Shine Wine

Third group will be - Mine Swine Bovine Feline

In step 1 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Mine Swine are exchanging their position with Bovine Feline respectively with everything else constant

therefore step 1 is- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

In step 2 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Smile Nile are exchanging their position with Style Mile respectively with everything else constant

therefore step 2 is- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

In step 3 the 1 and 2 of Second group are exchanging their position i.e. Shine is exchanging it's position with Wine with everything else constant

therefore step 3 is- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

In step 4 the 1 and 2 of First group are exchanging their position i.e. Style is exchanging it's position with Mile , 3 and 4 of First group are exchanging their position i.e. Smile is exchanging it's position with Nile and Similarly the 1 and 2 of Third group are exchanging their position i.e. Bovine is exchanging it's position with Feline , 3 and 4 of Third group are exchanging their position i.e. Mine is exchanging it's position with Swine with the positions of Shine and Wine remaining same

therefor step 4 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

In step 5 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Mile Style are exchanging their position with Nile Smile respectively and the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Feline Bovine are exchanging their position with Swine Mine respectively with everything else constant

therefor step 5 is- Nile Smile Mile Style Wine Shine Swine Mine Feline Bovine

In step 6 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Swine Mine are exchanging their position with Feline Bovine respectively with everything else constant

therefor step 6 is- Nile Smile Mile Style Wine Shine Feline Bovine Swine Mine

In step 7 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Nile Smile are exchanging their position with Mile Style respectively with everything else constant

therefor step 7 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

As can be observed the pattern is repeating

therefore step 8 will be Mile Style Nile Smile Shine Wine Feline Bovine Swine Mine

step 9- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 10- Smile Nile Style Mile Shine Wine Mine Swine Bovine Feline

step 11- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

step 12- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 13- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

step 14- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

Therefore the answer is option 'C'

Mark the arrangement that does not fall between step numbers 12 and 14.

Solution

Divide the whole sequence into group of words of 4, 2 and 4 so in the input the-

First group will be- Smile Nile Style Mile

Second group will be - Shine Wine

Third group will be - Mine Swine Bovine Feline

In step 1 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Mine Swine are exchanging their position with Bovine Feline respectively with everything else constant

therefore step 1 is- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

In step 2 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Smile Nile are exchanging their position with Style Mile respectively with everything else constant

therefore step 2 is- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

In step 3 the 1 and 2 of Second group are exchanging their position i.e. Shine is exchanging it's position with Wine with everything else constant

therefore step 3 is- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

In step 4 the 1 and 2 of First group are exchanging their position i.e. Style is exchanging it's position with Mile , 3 and 4 of First group are exchanging their position i.e. Smile is exchanging it's position with Nile and Similarly the 1 and 2 of Third group are exchanging their position i.e. Bovine is exchanging it's position with Feline , 3 and 4 of Third group are exchanging their position i.e. Mine is exchanging it's position with Swine with the positions of Shine and Wine remaining same

therefor step 4 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

In step 5 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Mile Style are exchanging their position with Nile Smile respectively and the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Feline Bovine are exchanging their position with Swine Mine respectively with everything else constant

therefor step 5 is- Nile Smile Mile Style Wine Shine Swine Mine Feline Bovine

In step 6 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Swine Mine are exchanging their position with Feline Bovine respectively with everything else constant

therefor step 6 is- Nile Smile Mile Style Wine Shine Feline Bovine Swine Mine

In step 7 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Nile Smile are exchanging their position with Mile Style respectively with everything else constant

therefor step 7 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

As can be observed the pattern is repeating

therefore step 8 will be Mile Style Nile Smile Shine Wine Feline Bovine Swine Mine

step 9- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 10- Smile Nile Style Mile Shine Wine Mine Swine Bovine Feline

step 11- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

step 12- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 13- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

step 14- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

As can be observed from steps 12-14 option D is not present

Therefore the answer is option 'D'

If the arrangement is repeated which of the steps given below is same as the INPUT row?

Solution

Divide the whole sequence into group of words of 4, 2 and 4 so in the input the-

First group will be- Smile Nile Style Mile

Second group will be - Shine Wine

Third group will be - Mine Swine Bovine Feline

In step 1 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Mine Swine are exchanging their position with Bovine Feline respectively with everything else constant

therefore step 1 is- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

In step 2 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Smile Nile are exchanging their position with Style Mile respectively with everything else constant

therefore step 2 is- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

In step 3 the 1 and 2 of Second group are exchanging their position i.e. Shine is exchanging it's position with Wine with everything else constant

therefore step 3 is- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

In step 4 the 1 and 2 of First group are exchanging their position i.e. Style is exchanging it's position with Mile , 3 and 4 of First group are exchanging their position i.e. Smile is exchanging it's position with Nile and Similarly the 1 and 2 of Third group are exchanging their position i.e. Bovine is exchanging it's position with Feline , 3 and 4 of Third group are exchanging their position i.e. Mine is exchanging it's position with Swine with the positions of Shine and Wine remaining same

therefor step 4 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

In step 5 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Mile Style are exchanging their position with Nile Smile respectively and the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Feline Bovine are exchanging their position with Swine Mine respectively with everything else constant

therefor step 5 is- Nile Smile Mile Style Wine Shine Swine Mine Feline Bovine

In step 6 the 1 and 2 of Third group are exchanging their position with the 3 and 4 respectively i.e. Swine Mine are exchanging their position with Feline Bovine respectively with everything else constant

therefor step 6 is- Nile Smile Mile Style Wine Shine Feline Bovine Swine Mine

In step 7 the 1 and 2 of First group are exchanging their position with the 3 and 4 respectively i.e. Nile Smile are exchanging their position with Mile Style respectively with everything else constant

therefor step 7 is- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

As can be observed the pattern is repeating

therefore step 8 will be Mile Style Nile Smile Shine Wine Feline Bovine Swine Mine

step 9- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 10- Smile Nile Style Mile Shine Wine Mine Swine Bovine Feline

step 11- Smile Nile Style Mile Shine Wine Bovine Feline Mine Swine

step 12- Style Mile Smile Nile Shine Wine Bovine Feline Mine Swine

step 13- Style Mile Smile Nile Wine Shine Bovine Feline Mine Swine

step 14- Mile Style Nile Smile Wine Shine Feline Bovine Swine Mine

As can be seen the answer cannot be step 9/11/14 therefore by eliminating the options we get the answer as step 20

Therefore the answer is option 'C'

For the following questions answer them individually

Study the information given below and answer the questions.

A Prime Minister is contemplating the expansion of his cabinet. There are four ministerial berths and there are eight probable candidates (C1-C8) to choose from. The selection should be in a manner that each selected person shares a liking with at least one of the other three selected members. Also, the selected must also hate at least one of the likings of any of the other three persons selected.

I. C1 likes travelling and sightseeing, but hates river rafting.

II. C2 likes sightseeing and squash, but hates travelling.

III. C3 likes river rafting, but hates sightseeing.

IV. C4 likes trekking, but hates squash.

V. C5 likes squash, but hates sightseeing and trekking.

VI. C6 likes travelling, but hates sightseeing and trekking.

VII. C7 likes river rafting and trekking, but hates travelling.

VIII. C8 likes sightseeing and river rafting, but hates trekking.

Who are the four people selected by the Prime Minister?

Solution

Option A:- C1, C2, C5, C6

therefore according to the given conditions if C1 is selected and since he hates river rafting then at least one of the C2, C5, C6 must like river rafting but C2 likes sightseeing and squash, C5 likes squash and C6 likes travelling i.e. none of C2, C5, C6 likes river rafting, therefore conditions are not getting satisfied therefore option A cannot be the answer

Option B:-C3, C4, C5, C6

therefore according to the given conditions if C3 is selected and since he hates sightseeing then at least one of the C4, C5, C6 must like sightseeingbut C4 likes trekking, C5 likes squash and C6 likes travelling i.e. none of C4, C5, C6 likes sightseeing, therefore conditions are not getting satisfied therefore option B cannot be the answer

Option C:-C1, C2, C4, C7

Here C1 hates river rafting and C7 likes river rafting also C1 likes sightseeing and so does C2 therefore C1 can be on the team, C2 hates travelling and C1 likes travelling also C2 likes sightseeing and so does C1 therefore C2 can be on the team, C4 hates squash and C2 likes squash also C4 likes trekking and so does C7 therefore C4 can be on the team and finally C7 hates travelling and C1 likes travelling also C7 likes trekking and so does C4 therefore C7 can be on the team.

Since all the conditions are getting satisfied option 'C' is the answer.

Arcelor, acquired by Mittal steel, was formed by merger of which of the following three steel companies?

Solution

Arcelor was created in February 2002 through the merger of Arbed (Luxembourg) founded in 1911, Aceralia (Spain) and Usinor (France).

Hence, option C is the correct answer.

Select the correct author - book match.

Solution

Imagining India is written by Nandan Nilekani.

Remaking India is written by Arun Maira.

A Better India A Better World is written by Narayan Murthy.

A Vision for the New Millennium is written by A P J Abdul Kalam.

Hence, option A is the correct answer.

There is a mistake in the question. Arun Maira is replaced by Ratan Tata.

The company Fem Care Pharma Limited, the manufacturer of Fem Bleach, was acquired by?

Solution

The company Fem Care Pharma Limited, the manufacturer of Fem Bleach, was acquired by Dabur India Limited.

Hence, option D is the correct answer.

Which is the correct Stock Index - Country Match?

Solution

HANG SENG is the Stock Index of Hong Kong.

NASDAQ is the Stock index of USA.

FTSE is the Stock index of United Kingdom.

KOSPI is the Stock index of South Korea.

Hence, option B is the correct answer.

Which is the correct Legal Act and Jurisdiction Match?

Solution

Companies Act 1956 is related to the formation and regulation of companies.

Competition Act 2002 is related to prohibition of anti-competitive agreements.

SEBI Act 1992 was enacted to protect the interests of the investors.

FEMA Act 1999 was enacted to facilitate external trade and payments.

Therefore, option A is the right answer.

Match the President, Country and Currency.

Solution

Nicolas Sarkozy is from France.

Dmitry Medvedev is from Russia.

Yoweri Museveni if from Uganda.

Horst Kohler is from Germany.

Hence, option C is the correct answer.

The abbreviations given in the first column are explained in the second column. Select the option which has all wrong explanations of the abbreviations.

Solution

UNCTAD : United Nations Conference on Trade and Development

UNCED : United Nations Conference on Environment and Development

PFRDA : Pension Fund Regulatory and Development Authority

ASSOCHAM : Associated Chambers of Commerce and Industry of India.

There is no such acronym as TAFTA.

Hence, option A is the correct answer.

Who amongst the following was not nominated by the Government of India on the board of Satyam Computers Services?

Solution

T N Manoharan, Suryakant Balakrishnan Mainak, Kiran Karnik were nominated by the Government of India on the board of Satyam Computers Services.

Hence, option B is the correct answer.

CDS which has been in news recently stands for?

Solution

CDS stands for Credit Default Swap.

Hence, option C is the correct answer.

The table given below matches the company with its auto brand. Choose the correct match.

Solution

Land Rover is of TATA, Jetta is of Volkswagen, Lexus is of Toyota and Xylo is of Mahindra.

Hence, option C is the correct answer.

The slogans in the table given below have been matched with the company they relate to. Choose the correct match.

Solution

HP's slogan is Technology you can trust.

Philips' slogan is Let's make things better.

Microsoft's slogan is You potential our passion.

Intel's slogan is Sponsors of tomorrow.

Hence, option C is the correct answer.

In the financial year 2008-09, the top three investing countries in terms of FDI inflows were:

Solution

In the financial year 2008-09, the top three investing countries in terms of FDI inflows were Mauritius, Singapore, USA.

Hence, option B is the correct answer.

Negative inflation is also called:

Solution

Negative inflation is also called deflation.

Deflation is when consumer and asset prices decrease over time, and purchasing power increases. Essentially, you can buy more goods or services tomorrow with the same amount of money you have today.

Hence, option B is the correct answer.

The co-founders of Google are:

Solution

The co-founders of Google are Sergey Brin & Larry Page.

Hence, option C is the correct answer.

Which of the following Public Sector Units does not fall in the category of ‘Navratna’ PSUs:

Which one of the following statements does not relate to the concept of carbon credits?

Solution

Except option D, all other statements are related to carbon credits.

Hence, option D is correct answer.

India signed the Kyoto Protocol in the year:

Solution

India signed the Kyoto Protocol on 26 August 2002.

Hence, option C is the correct answer.

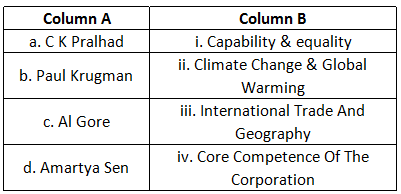

Match Column A with Column B.

Solution

C. K Prahlad wrote the book Core Competence of the Corporation.

Paul Krugman wrote International Trade and New Economic Geography.

Al gore is related to Climate Change and Global Warming.

Amartya Sen is related to Capability and Equality.

Hence, option B is the correct answer.

Match the women CEOs with the company.

Solution

Ms Sikha Sharma is the CEO of Axis Bank.

Ms. Naina Lal Kidwaiekani was the CEO of HSBC.

Ms Indra Nooyi is the CEO of PepsiCo.

Ms. kiran Mazumdar Shaw is the CEO of Biocon India.

Hence, option C is the correct answer.

Match the company and the place where it originates from

Solution

Section III

Read carefully the four passages that follow and answer the questions given at the end of each passage:

PASSAGE I

The most important task is revitalizing the institution of independent directors. The independent directors of a company should be faithful fiduciaries protecting, the long-term interests of shareholders while ensuring fairness to employees, investor, customer, regulators, the government of the land and society. Unfortunately, very often, directors are chosen based of friendship and, sadly, pliability. Today, unfortunately, in the majority of cases, independence is only true on paper.

The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors. The board should adopt global standards for director-independence, and should disclose how each independent director meets these standards. It is desirable to have a comprehensive report showing the names of the company employees of fellow board members who are related to each director on the board. This report should accompany the annual report of all listed companies.

Another important step is to regularly assess the board members for performance. The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. Underperforming directors should be allowed to leave at the end of their term in a gentle manner so that they do not lose face. Rather than being the rubber stamp of a company’s management policies, the board should become a true active partner of the management. For this, independent directors should be trained in their in their in roles and responsibilities. Independent directors should be trained on the business model and risk model of the company, on the governance practices, and the responsibilities of various committees of the board of the company. The board members should interact frequently with executives to understand operational issues. As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present.

The independent board members should periodically review the performance of the company’s CEO, the internal directors and the senior management. This has to be based on clearly defined objective criteria, and these criteria should be known to the CEO and other executive directors well before the start of the evolution period. Moreover, there should be a clearly laid down procedure for communicating the board’s review to the CEO and his/her team of executive directors. Managerial remuneration should be based on such reviews. Additionally, senior management compensation should be determined by the board in a manner that is fair to all stakeholders. We have to look at three important criteria in deciding managerial remuneration-fairness accountability and transparency. Fairness of compensation is determined by how employees and investors react to the compensation of the CEO. Accountability is enhanced by splitting the total compensation into a small fixed component and a large variable component. In other words, the CEO, other executive directors and the senior management should rise or fall with the fortunes of the company. The variable component should be linked to achieving the long-term objectives of the firm. Senior management compensation should be reviewed by the compensation committee of the board consisting of only the independent directors. This should be approved by the shareholders. It is important that no member of the internal management has a say in the compensation of the CEO, the internal board members or the senior management.

The SEBI regulations and the CII code of conduct have been very helpful in enhancing the level of accountability of independent directors. The independent directors should decide voluntarily how they want to contribute to the company. Their performance should decide voluntarily how they want to contribute to the company. Their performance should be appraised through a peer evaluation process. Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal.

Auditing is another major area that needs reforms for effective corporate governance. An audit is the Independent examination of financial transactions of any entity to provide assurance to shareholder and other stakeholders that the financial statements are free of material misstatement. Auditors are qualified professionals appointed by the shareholders to report on the reliability of financial statements prepared by the management. Financial markets look to the auditor’s report for an independent opinion on the financial and risk situation of a company. We have to separate such auditing form other services. For a truly independent opinion, the auditing firm should not provide services that are perceived to be materially in conflict with the role of the auditor. These include investigations, consulting advice, sub contraction of operational activities normally undertaken by the management, due diligence on potential acquisitions or investments, advice on deal structuring, designing/implementing IT systems, bookkeeping, valuations and executive recruitment. Any departure from this practice should be approved by the audit committee in advance. Further, information on any such exceptions must be disclosed in the company’s quarterly and annual reports. To ensure the integrity of the audit team, it is desirable to rotate auditor partners. The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This eliminates the possibility of the lead auditor and the company management getting into the kind of close, cozy relationship that results in lower objectivity in audit opinions. Further, a registered auditor should not audit a chief accounting office was associated with the auditing firm. It is best that members of the audit teams are prohibited from taking up employment in the audited corporations for at least a year after they have stopped being members of the audit team.

A competent audit committee is essential to effectively oversee the financial accounting and reporting process. Hence, each member of the audit committee must be ‘financially literate’, further, at least one member of the audit committee, preferably the chairman, should be a financial expert-a person who has an understanding of financial statements and accounting rules, and has experience in auditing. The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistleblowers. These complaints may be regarding questionable accounting or auditing issues, any harassment to an employee or any unethical practice in the company. The whistleblowers must be protected.

Any related-party transaction should require prior approval by the audit committee, the full board and the shareholders if it is material. Related parties are those that are able to control or exercise significant influence. These include; parent- subsidiary relationships; entities under common control; individuals who, through ownership, have significant influence over the enterprise and close members of their families; and dey management personnel.

Accounting standards provide a framework for preparation and presentation of financial statements and assist auditors in forming an opinion on the financial statements. However, today, accounting standards are issued by bodies comprising primarily of accountants. Therefore, accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies. This body should be independently funded.

Currently, an independent oversight of the accounting profession does not exist. Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence. This body should comprise a "majority of non- practicing accountants to ensure independent oversight. To avoid any bias, the chairman of this body should not have practiced as an accountant during the preceding five years. Auditors of all public companies must register with this body. It should enforce compliance with the laws by auditors and should mandate that auditors must maintain audit working papers for at least seven years.

To ensure the materiality of information, the CEO and CFO of the company should certify annual and quarterly reports. They should certify that the information in the reports fairly presents the financial condition and results of operations of the company, and that all material facts have been disclosed. Further, CEOs and CFOs should certify that they have established internal controls to ensure that all information relating to the operations of the company is freely available to the auditors and the audit committee. They should also certify that they have evaluated the effectiveness of these controls within ninety days prior to the report. False certifications by the CEO and CFO should be subject to significant criminal penalties (fines and imprisonment, if willful and knowing). If a company is required to restate its reports due to material non-compliance with the laws, the CEO and CFO must face severe punishment including loss of job and forfeiting bonuses or equity-based compensation received during the twelve months following the filing.

The problem with the independent directors has been that:

I. Their selection has been based upon their compatibility with the company management

II. There has been lack of proper training and development to improve their skill set

III. Their independent views have often come in conflict with the views of company management. This has hindered the company’s decision-making process

IV. Stringent standards for independent directors have been lacking

Solution

Statement (I) can be inferred from the first paragraph: "directors are chosen based of friendship and, sadly, pliability"

Statement (II) can directly be inferred from the third paragraph: "For this, independent directors should be trained in their in their in roles and responsibilities."

Statement (IV) can be inferred from the second paragraph: "The need of the hour is to strengthen the independence of the board. We have to put in place stringent standards for the independence of directors."

Statement (III) is incorrect.

Hence, the answer is option D.

Which of the following, according to author, does not have an impact on effective corporate governance?

Solution

The author says, "Ideally, the compensation committee should decide on the compensation of each independent director based on such a performance appraisal.", i.e., the compensation should depend upon the performance of independent directors and not the other way round.

Hence, the answer is option B.

To improve the quality and reliability of the information reported in the financial statements:

I. Accounting standards should keep pace with the dynamic business environment

II. There should be a body of internal auditors to oversee the functioning of external auditors

III. Reports should be certified by key company officials

IV. Accounting standards should be set by a body comprising of practicing accountants only and this body should be funded from a corpus built up from the contributions made by the companies

Solution

Statement I can be inferred from the eleventh paragraph

Internal auditors have not been mentioned in the passage. Statement II is incorrect.

Statement III can be inferred from the last paragraph.

It is given in the passage that the body should comprise a "majority of non- practicing accountants to ensure independent oversight. Statement IV is wrong.

Hence, option C is the correct answer.

Which of the following may not help in improving in the accountability of management to the shareholders?

Solution

Option A : Consider the sentence:- The assessment should focus on issues like competence, preparation, participation and contribution. Ideally, this evaluation should be performed by a third party. This option surely improves accountability. Hence it is incorrect

Option B : The lead audit partner and the audit partner responsible for reviewing a company’s audit must be rotated at least once every three to five years. This option is also incorrect

Option D : The audit committee should establish procedures for the treatment of complaints received through anonymous submission by employees and whistle-blowers. This option also improves the accountability of the management to the shareholders. Hence this option is also incorrect.

Option C is not mentioned anywhere in the passage. Hence it is the most suitable option.

The author of the passage does not advocate:

Solution

Option A : Consider the sentence "As part of the board meeting agenda, the independent directors should have a meeting among themselves without the management being present." The author definitely advocates increased activism by the independent directors.

Option B : Consider the sentence "Hence, an independent body should be constituted to oversee the functioning of auditors for Independence, the quality of audit and professional competence." The author calls for measures to improve the independence of auditors.

Option C : Consider the sentence "Accounting standards do not always keep pace with changes in the business environment. Hence, the accounting standards-setting body should include members drawn from the industry, the profession and regulatory bodies." The author says that the accounting standards should be modified based on the changing business conditions.

Hence all these options are advocated by the author.

The author does not advocate option D. Hence option D is the correct answer.

I suggest that the essential character of the Trade Cycle and, especially, the regularity of time-sequence and of duration which justifies us in calling it a cycle, is mainly due to the way in which the marginal efficiency of capital fluctuates. The Trade Cycle is best regarded, I think, as being occasioned by a cyclical change in the marginal efficiency of capital, though complicated and often aggravated by associated changes in the other significant short period variables of the economic system.

By a cyclical movement we mean that as the system progresses in, e.g. the upward direction, the forces propelling it upwards at first gather force and have a cumulative effect on one another but gradually lose their strength until at a certain point they tend to be replaced by forces operating in the opposite direction; which in turn gather force for a time and accentuate one another, until they too, having reached their maximum development, wane and give place to their opposite. We do not, however, merely mean by a cyclical movement that upward and downward tendencies, once started, do not persist for ever in the same direction but are ultimately reversed. We mean also that there is some recognizable degree of regularity in the time-sequence and duration of the upward and downward movements. There is, however, another characteristic of what we call the Trade Cycle which our explanation must cover if it is to be adequate; namely, the phenomenon of the ‘crisis’ the fact that the substitution of a downward for an upward tendency often takes place suddenly and violently, whereas there is, as a rule, no such sharp turning-point when an upward is substituted for a downward tendency. Any fluctuation in investment not offset by a corresponding change in the propensity to consume will, of course, result in a fluctuation in employment. Since, therefore, the volume of investment is subject to highly complex influences, it is highly improbable that all fluctuations either in investment itself or in the marginal efficiency of capital will be of a cyclical character.

We have seen above that the marginal efficiency of capital depends, not only on the existing abundance or scarcity of capital-goods and the current cost of production of capital- goods, but also on current expectations as to the future yield of capital-goods. In the case of durable assets it is, therefore, natural and reasonable that expectations of the future should play a dominant part in determining the scale on which new investment is deemed advisable. But, as we have seen, the basis for such expectations is very precarious. Being based on shifting and unreliable evidence, they are subject to sudden and violent changes. Now, we have been accustomed in explaining the ‘crisis’ to lay stress on the rising tendency of the rate of interest under the influence of the increased demand for money both for trade and speculative purposes. At times this factor may certainly play an aggravating and, occasionally perhaps, an initiating part. But I suggest that a more typical, and often the predominant, explanation of the crisis is, not primarily a rise in the rate of interest, but a sudden collapse in the marginal efficiency of capital. The later stages of the boom are characterized by optimistic expectations as to the future yield of capital goods sufficiently strong to offset their growing abundance and their rising costs of production and, probably, a rise in the rate of interest also. It is of the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and of speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of the future yield of capital-assets, that, when disillusion falls upon an over-optimistic and over- bought market, it should fall with sudden and even catastrophic force. Moreover, the dismay and uncertainty as to the future which accompanies a collapse in the marginal efficiency of capital naturally precipitates a sharp increase in liquidity-preference and hence a rise in the rate of interest. Thus the fact that a collapse in the marginal efficiency of capital tends to be associated with a rise in the rate of interest may seriously aggravate the decline in investment. But the essence of the situation is to be found, nevertheless, in the collapse in the marginal efficiency of capital, particularly in the case of those types of capital which have been contributing most to the previous phase of heavy new investment. Liquidity preference, except those manifestations of it which are associated with increasing trade and speculation, does not increase until after the collapse in the marginal efficiency of capital. It is this, indeed, which renders the slump so intractable.

Which of the following does not describe the features of cyclical movement?

Solution

From the second paragraph, we can infer that the cycle can be reversed. So, option B is factually wrong.

Hence, option B is the correct answer.

Marginal efficiency of the capital does not depend on which of following factors?

Solution

We have seen above that the marginal efficiency of capital depends, not only on the existing abundance or scarcity of capital-goods and the current cost of production of capital- goods, but also on current expectations as to the future yield of capital-goods - From these lines, options A, B and C can be inferred.

Availability of capital is nowhere mentioned as a factor on which marginal efficiency depends.

Hence, option D is the correct answer.

Which of the following explains the phenomenon of crisis?

I. A sudden collapse in the marginal efficiency of capital

II. Increase in the rate of interest causing the decline in investments

III. A sudden and violent substitution of upward movement by a downward tendency

IV. Decline in the liquidity preference of the investors

Solution

In the 1st paragraph it is mentioned that "the phenomenon of the ‘crisis’ the fact that the substitution of a downward for an upward tendency often takes place suddenly", from this option III can be concluded.

In the 2nd paragraph it is mentioned that "explanation of the crisis is, not primarily a rise in the rate of interest, but a sudden collapse in the marginal efficiency of capital. The later stages of the boom are characterized by optimistic expectations as to the future yield of capital goods sufficiently strong to offset their growing abundance and their rising costs of production and, probably, a rise in the rate of interest also.

From this option I and II can be concluded.

Thus, option B is the correct answer.

The broad scientific understanding today is that our planet is experiencing a warming trend over and above natural and normal variations that is almost certainly due to human activities associated with large-scale manufacturing. The process began in the late 1700s with the Industrial Revolution, when manual labor, horsepower, and water power began to be replaced by or enhanced by machines. This revolution, over time, shifted Britain, Europe, and eventually North America from largely agricultural and trading societies to manufacturing ones, relying on machinery and engines rather than tools and animals.

The Industrial Revolution was at heart a revolution in the use of energy and power. Its beginning is usually dated to the advent of the steam engine, which was based on the conversion of chemical energy in wood or coal to thermal energy and then to mechanical work primarily the powering of industrial machinery and steam locomotives. Coal eventually supplanted wood because, pound for pound, coal contains twice as much energy as wood (measured in BTUs, or British thermal units, per pound) and because its use helped to save what was left of the world's temperate forests. Coal was used to produce heat that went directly into industrial processes, including metallurgy, and to warm buildings, as well as to power steam engines. When crude oil came along in the mid- 1800s, still a couple of decades before electricity, it was burned, in the form of kerosene, in lamps to make light replacing whale oil. It was also used to provide heat for buildings and in manufacturing processes, and as a fuel for engines used in industry and propulsion.

In short, one can say that the main forms in which humans need and use energy are for light, heat, mechanical work and motive power, and electricity which can be used to provide any of the other three, as well as to do things that none of those three can do, such as electronic communications and information processing. Since the Industrial Revolution, all these energy functions have been powered primarily, but not exclusively, by fossil fuels that emit carbon dioxide (CO2), To put it another way, the Industrial Revolution gave a whole new prominence to what Rochelle Lefkowitz, president of Pro-Media Communications and an energy buff, calls "fuels from hell" - coal, oil, and natural gas. All these fuels from hell come from underground, are exhaustible, and emit CO2 and other pollutants when they are burned for transportation, heating, and industrial use. These fuels are in contrast to what Lefkowitz calls "fuels from heaven" -wind, hydroelectric, tidal, biomass, and solar power. These all come from above ground, are endlessly renewable, and produce no harmful emissions.

Meanwhile, industrialization promoted urbanization, and urbanization eventually gave birth to suburbanization. This trend, which was repeated across America, nurtured the development of the American car culture, the building of a national highway system, and a mushrooming of suburbs around American cities, which rewove the fabric of American life. Many other developed and developing countries followed the American model, with all its upsides and downsides. The result is that today we have suburbs and ribbons of highways that run in, out, and around not only America s major cities, but China's, India's, and South America's as well. And as these urban areas attract more people, the sprawl extends in every direction.

All the coal, oil, and natural gas inputs for this new economic model seemed relatively cheap, relatively inexhaustible, and relatively harmless-or at least relatively easy to clean up afterward. So there wasn't much to stop the juggernaut of more people and more development and more concrete and more buildings and more cars and more coal, oil, and gas needed to build and power them. Summing it all up, Andy Karsner, the Department of Energy's assistant secretary for energy efficiency and renewable energy, once said to me: "We built a really inefficient environment with the greatest efficiency ever known to man."

Beginning in the second half of the twentieth century, a scientific understanding began to emerge that an excessive accumulation of largely invisible pollutants-called greenhouse gases - was affecting the climate. The buildup of these greenhouse gases had been under way since the start of the Industrial Revolution in a place we could not see and in a form we could not touch or smell. These greenhouse gases, primarily carbon dioxide emitted from human industrial, residential, and transportation sources, were not piling up along roadsides or in rivers, in cans or empty bottles, but, rather, above our heads, in the earth's atmosphere. If the earth's atmosphere was like a blanket that helped to regulate the planet's temperature, the CO2 buildup was having the effect of thickening that blanket and making the globe warmer.

Those bags of CO2 from our cars float up and stay in the atmosphere, along with bags of CO2 from power plants burning coal, oil, and gas, and bags of CO2 released from the burning and clearing of forests, which releases all the carbon stored in trees, plants, and soil. In fact, many people don't realize that deforestation in places like Indonesia and Brazil is responsible for more CO2 than all the world's cars, trucks, planes, ships, and trains combined - that is, about 20 percent of all global emissions. And when we're not tossing bags of carbon dioxide into the atmosphere, we're throwing up other greenhouse gases, like methane (CH4) released from rice farming, petroleum drilling, coal mining, animal defecation, solid waste landfill sites, and yes, even from cattle belching. Cattle belching? That's right-the striking thing about greenhouse gases is the diversity of sources that emit them. A herd of cattle belching can be worse than a highway full of Hummers. Livestock gas is very high in methane, which, like CO2, is colorless and odorless. And like CO2, methane is one of those greenhouse gases that, once released into the atmosphere, also absorb heat radiating from the earth's surface. "Molecule for molecule, methane's heat-trapping power in the atmosphere is twenty-one times stronger than carbon dioxide, the most abundant greenhouse gas.." reported Science World (January 21, 2002). “With 1.3 billion cows belching almost constantly around the world (100 million in the United States alone), it's no surprise that methane released by livestock is one of the chief global sources of the gas, according to the U.S. Environmental Protection Agency ... 'It's part of their normal digestion process,' says Tom Wirth of the EPA. 'When they chew their cud, they regurgitate [spit up] some food to rechew it, and all this gas comes out.' The average cow expels 600 liters of methane a day, climate researchers report."

What is the precise scientific relationship between these expanded greenhouse gas emissions and global warming? Experts at the Pew Center on Climate Change offer a handy summary in their report "Climate Change 101. " Global average temperatures, notes the Pew study, "have experienced natural shifts throughout human history. For example; the climate of the Northern Hemisphere varied from a relatively warm period between the eleventh and fifteenth centuries to a period of cooler temperatures between the seventeenth century and the middle of the nineteenth century. However, scientists studying the rapid rise in global temperatures during the late twentieth century say that natural variability cannot account for what is happening now." The new factor is the human factor-our vastly increased emissions of carbon dioxide and other greenhouse gases from the burning of fossil fuels such as coal and oil as well as from deforestation, large-scale cattle-grazing, agriculture, and industrialization.

“Scientists refer to what has been happening in the earth’s atmosphere over the past century as the ‘enhanced greenhouse effect’”, notes the Pew study. By pumping man- made greenhouse gases into the atmosphere, humans are altering the process by which naturally occurring greenhouse gases, because of their unique molecular structure, trap the sun’s heat near the earth’s surface before that heat radiates back into space.