answer questions based on the following information:

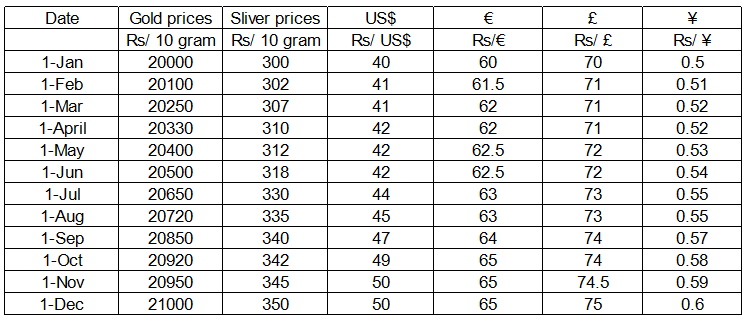

In the beginning of the year 2010, Mr. Sanyal had the option to invest Rs. 800000 in one or more of the following assets – gold, silver, US bonds, EU bonds, UK bonds and Japanese bonds. In order to invest in US bonds, one must first convert his investible fund into US Dollars at the ongoing exchange rate. Similarly, if one wants to invest in EU bonds or UK bonds or Japanese bonds one must first convert his investible fund into Euro, British Pounds and Japanese Yen respectively at the ongoing exchange rates. Transactions were allowed only in the beginning of every month. Bullion prices and exchange rates were fixed at the beginning of every

month and remained unchanged throughout the month. Refer to the table titled “Bullion Prices and Exchange Rates in 2010" for the relevant data.

Bullion Prices and Exchange Rates in 2010

Interest rates on US, EU, UK and Japanese bonds are 10%, 20%, 15% and 5% respectively.

Advisors were asked to prepare an investment strategy that involved US Bonds, EU Bonds and Japanese Bonds, keeping at least 20% of the initial fund in each of these assets for the entire year, and allowing exactly four additional transactions in the course of the year. On 2nd January 2011, while comparing five different recommendations that he had received from his financial advisors in the beginning of 2010, Mr. Sanyal referred to the table “Bullion Prices and Exchange Rates in 20

10”. One transaction is defined as the buying or selling of an asset. Which of the recommendation out of the following was the best one?

Solution

To determine the best investment strategy for Mr. Sanyal, we must identify the timing that maximizes returns from two sources: the annual interest rates of the bonds (EU at 20%, US at 10%, and Japan at 5%) and the exchange rate appreciation of the respective currencies against the Rupee (Rs.). Since the rules require at least 20% of the initial Rs. 800,000 to remain in each asset for the entire year, the goal is to move the "flexible" remainder of the funds into the asset that is about to experience the steepest growth in value.

The most significant variable in this scenario is the US Dollar (US$), which starts the year at Rs. 40 and ends at Rs. 50, representing a 25% appreciation. However, this growth is not linear. Between April and June, the exchange rate is completely stagnant at Rs. 42. It then begins a sharp climb starting in July, hitting Rs. 44, and continues rising until it peaks and stabilizes at Rs. 50 in November and December.

By choosing Option A (June and November), the investor perfectly brackets this growth period. Shifting the flexible capital in June allows the investor to buy into US bonds just before the currency begins its rapid ascent from 42 to 50. Conversely, performing transactions in March or May would be premature, as the capital would sit in a stagnant currency while missing out on the superior 20% interest rate offered by the EU bonds during those months.

Finally, the November transaction allows the investor to "lock in" the gains from the US Dollar's peak. Since the exchange rate remains at 50 through December, there is no further currency gain to be had in the final month. By moving funds in November, the investor can shift back into the higher-interest EU bonds for the final month of the year, ensuring the highest possible closing balance for the portfolio.

Thus, the correct answer is Option A.

Get AI Help

Create a FREE account and get:

- All Quant Formulas and shortcuts PDF

- 15 XAT previous papers with solutions PDF

- XAT Trial Classes for FREE

XAT Quant Questions | XAT Quantitative Ability

XAT DILR Questions | LRDI Questions For XAT

XAT Verbal Ability Questions | VARC Questions For XAT

Free XAT DILR Questions

Book Free CAT Mentorship

Get personalized CAT strategy from a 99%iler

500+ students mentored

OTP Verification

Enter the 6-digit code sent to your phone

Booking Summary

Enter OTP

Didn't receive the OTP?