Find the sum of the following series;

$$\frac{2}{1!}+\frac{3}{2!}+\frac{6}{3!}+\frac{11}{4!}+\frac{18}{5!}+...$$

IIFT 2010 Question Paper

For the following questions answer them individually

Solution

$$\frac{2}{1!}+\frac{3}{2!}+\frac{6}{3!}+\frac{11}{4!}+\frac{18}{5!}+...$$ = 2 + 1.5 + 1 + 0.5 + 0.15 + smaller insignificant values $$\approx$$ 5.2

Option 'A' = 3e - 1 = 3*2.718-1 = 7.15 therefore cannot be our answer

Option 'B' = 3(e - 1) = 3*(2.718-1) = 5.154 therefore can be our answer

Option 'C' = 3(e + 1) = 3*(2.718+1) = 11.15 therefore cannot be our answer

Option 'D' = 3e + 1 = 9.15 therefore cannot be our answer

Therefore option 'B' is our answer

How many positive integers ‘n’ can we form using the digits 3, 4, 4, 5, 6, 6, 7 if we want ‘n’ to exceed 6,000,000?

Solution

We are given exactly 7 digits - 3, 4, 4, 5, 6, 6, 7. The millions digit can be either 6 or 7.

Case 1: When the millions digit is 6.

6 _ _ _ _ _ _ We are left with six digits {3, 4, 4, 5, 6, 7}.

These six digits can be arranged in six places in $$\dfrac{6!}{2!}$$ ways.

Case 1: When the millions digit is 7.

7 _ _ _ _ _ _ We are left with six digits {3, 4, 4, 5, 6, 6}.

These six digits can be arranged in six places in $$\dfrac{6!}{2!*2!}$$ ways.

Therefore, total number of numbers 'n' = $$\dfrac{6!}{2!}$$ + $$\dfrac{6!}{2!*2!}$$ = 360 + 180 = 540. Hence, option C is the correct answer.

A Techno company has 14 machines of equal efficiency in its factory. The annual manufacturing costs are Rs. 42,000 and establishment charges are Rs. 12,000. The annual output of the company is Rs. 70,000. The annual output and manufacturing costs are directly proportional to the no. of machines. The shareholders get 12.5% of the total profit which is equal to the total output minus the total cost. If 7.14% of machines remain closed throughout the year, then the percentage decrease in the amount of profit of the shareholders would be:

Solution

Manufacturing cost (MC) of 14 machines = Rs. 42000

Output of 14 machines = Rs. 70000

Establishment cost (EC) = Rs. 12000

Profit = Rs.(70000 - 42000 - 12000) = Rs. 16000

Shareholder's profit = 12.5% of Rs. 16000 = Rs. 2000

It is given that 7.14% of the machines were non functional which means only 13 machines were functional.

MC of 13 machines = Rs. (42000 * $$\frac{13}{14}$$) = Rs. 39000 [As it is directly proportional to the number of functional machines]

Output of 13 machines = Rs. (70000 * $$\frac{13}{14}$$) = Rs. 65000 [As it is directly proportional to the number of functional machines]

EC of 13 machines = Rs. 12000 [As it does not depend on the number of functional machines]

Profit = Rs.(65000 - 39000 - 12000) = Rs. 14000

Shareholder's profit = 12.5% of Rs. 14000 = Rs. 1750

Reduction in Shareholder's profit = Rs.(2000 - 1750) = Rs. 250

Reduction % = $$\frac{250}{2000}$$*100% = 12.5%

Hence, option B is the correct answer.

Sun Life Insurance Company issues standard,preferred, and ultra-preferred policies. Amongthe company’s policy holders of a certain age,50% are standard with a probability of 0.01 ofdying in the next year, 30% are preferred with aprobability 0.008 of dying in the next year, and20% are ultra-preferred with a probability of0.007 of dying in the next year. If a policy holderof that age dies in the next year, what is theprobability of the deceased being a preferredpolicy holder?

Solution

If there are 10000 policy holders then 5000 are of standard, 3000 are of preferred and 2000 are of ultra-preferred

0.01 of standard policy holders may die next year i.e. 50 of standard policy holder may die next year

0.008 of preferred policy holders may die next year i.e. 24 of preferred policy holders may die next year

0.007 of ultra-preferred policy holders may die next year i.e. 14 of ultra-preferred policy holders may die next year

Total number of people that may die next year = 50+24+14 = 88

Probability that the person died is a preferred policy holder is $$\frac{24}{88}$$ = 0.2727

Therefore our answer is option 'B'

A metro train from Mehrauli to Gurgoan has capacity to board 900 people. The fare charged (in RS.) is defined by the function $$f=(54-\frac{x}{32})^{2}$$ where ‘x’ is the number of the people per trip.How many people per trip will make the marginal revenue equal to zero?

Solution

It is given that the fare charged (in RS.) is defined by the function $$f=(54-\dfrac{x}{32})^{2}$$ where ‘x’ is the number of the people per trip.

Let 'x' be the number of people per trip that will make the marginal revenue equal to zero.

Total revenue generated per trip, g(x) = $$x*(54-\dfrac{x}{32})^{2}$$

When total revenue is maximum, then the marginal revenue will be zero. Therefore, we have to find out the value of 'x' for which g'(x) = 0

$$\Rightarrow$$ $$(54-\dfrac{x}{32})^{2}-\dfrac{2x}{32}*(54-\dfrac{x}{32})=0$$

$$\Rightarrow$$ $$(54-\dfrac{x}{32})^{2}-\dfrac{2x}{32}*(54-\dfrac{x}{32})=0$$

$$\Rightarrow$$ $$(54-\dfrac{x}{32})*(54-\dfrac{3x}{32})=0$$

$$\Rightarrow$$ $$x = 1728, 576$$

It is given that the train has a capacity of 900 only. Hence, x $$\neq$$ 1728 i.e. $$x = 576$$. Therefore, option B is the correct answer.

If each $$\alpha,\beta$$ and $$\gamma$$ is a positive acute angle such that $$Sin(\alpha+\beta-\gamma)=\frac{1}{\sqrt{2}},Cosec(\beta+\gamma-\alpha)=\frac{2}{\sqrt{3}}$$ and $$tan(\gamma+\alpha-\beta)=\frac{1}{\sqrt{3}}$$. What are the values of $$\alpha,\beta,\gamma$$?

Solution

if $$Sin(\alpha+\beta-\gamma)=\frac{1}{\sqrt{2}} $$then $$\alpha+\beta-\gamma$$ = 45° ...(1)

if $$Cosec(\beta+\gamma-\alpha)=\frac{2}{\sqrt{3}}$$ then $$\beta+\gamma-\alpha$$ = 60° ...(2)

if $$tan(\gamma+\alpha-\beta)=\frac{1}{\sqrt{3}}$$ then $$\gamma+\alpha-\beta$$ = 30° ...(3)

Adding we get $$\alpha+\beta+\gamma$$ = 135° ...(4)

from 1,2,3 and 4 we get $$\alpha$$ = 37.5° therefore answer is option 'A'

Shyam, Gopal and Madhur are three partners in a business. Their capitals are respectively Rs 4000,Rs 8000 and Rs 6000. Shyam gets 20% of total profit for managing the business. The remaining profit is divided among the three in the ratio of their capitals. At the end of the year, the profit of Shyam is Rs 2200 less than the sum of the profit of Gopal and Madhur. How much profit, Madhur will get?

Solution

Let the total profit be P. Shyam will get 0.2P for managing the business rest 0.8 P will be divided in the ratio of 2:4:3

i.e. shyam will get 0.2P+0.8P*$$\frac{2}{9}$$ and Gopal and Madhur will together get 0.8P*$$\frac{7}{9}$$

Given that 0.8P*$$\frac{7}{9}$$ - (0.2P+0.8P*$$\frac{2}{9}$$) = 2200

Solving we get P = 9000 therefore profit madhur will get is $$0.8*9000*\frac{1}{3}$$ = 2400

Therefore our answer is option 'B'

In how many ways can four letters of the word ‘SERIES’ be arranged?

Solution

We can see that letters are S, S, E, E, I, R.

Case 1: When all 4 letters are different. There is only one way where we select one each S, E, I, R.

Total number of 4 letter words which can be formed using these letters = $$4!$$ = 24.

Case 2: When all 2 letters are of 1 type and 2 letters are different.

Total number of ways in which 4 letter can be chosen = 2C1*3C2 = 6

Total number of 4 letter words which can be formed using these letters = $$6*\dfrac{4!}{2!}$$ = 72

Case 3: When all 2 letters are of 1 type and remaining 2 letters are of different another same type. There is only one way when we select S, S, E, E.

Total number of 4 letter words which can be formed using these letters = $$\dfrac{4!}{2!*2!}$$ = 6

We have considered all possible cases. Hence, total number of four letters of the word can be made = 24 + 72 + 6 = 102. Hence, option D is the correct answer.

The area of a triangle is 6, two of its vertices are (1, 1) and (4, -1), the third vertex lies on y = x + 5. Find the third vertex.

Solution

Let us assume that X co-ordinate of the 3rd vertex is a. Then y = a + 5. So the co-ordinates of the vertex = (a, a+5)

Ttherefore, 6 = $$\dfrac{1}{2}\times \begin{vmatrix}1 & 1 & 1\\4 & -1 & 1\\a & a+5 & 1 \end{vmatrix}$$

$$\Rightarrow$$ $$\pm12$$ = 1(-1-a-5) -1(4 - a) + 1(4a+20+a)

$$\Rightarrow$$ $$\pm12$$ = 5a + 10

$$\Rightarrow$$ a = $$\dfrac{2}{5}$$, $$\dfrac{-22}{5}$$

Hence, the third vertex can be out of the two values ($$\dfrac{2}{5}$$, $$\dfrac{27}{5}$$) or ($$\dfrac{-22}{5}$$, $$\dfrac{3}{5}$$).

Therefore, option A is the correct answer.

A small confectioner bought a certain number of pastries flavoured pineapple, mango and black-forest from the bakery, giving for each pastry as many rupees as there were pastry of that kind;altogether he bought 23 pastries and spent Rs.211; find the number of each kind of pastry that he bought, if mango pastry are cheaper than pineapple pastry and dearer than black-forest pastry.

Solution

Given that cost of a type of pastry is equal to the quantity bought

if x,y,z are the no. of pastries bought of each type then $$x^2+y^2+z^2$$ = 211 and x+y+z = 23

Using options,

option A = 10,9,4 i.e. 100+81+16 = 197 therefore cannot be the answer

option B= 11, 9, 3 i.e. 121+81+9 = 211 Therefore is our answer

option C = 10, 8 , 5 i.e. 100+64+25 = 189 therefore cannot be the answer

option D = 11, 8, 4 i.e. 121+64+16 = 201 therefore cannot be the answer

Therefore our answer is option 'B'

Find the roots of the quadratic equation $$bx^{2}-2ax+a=0$$

Solution

If the quadratic equation is of type $$Ax^+Bx+C=0$$ then the roots of the quadratic equation are given by

$$x = \dfrac{-B\pm\sqrt{B^2 - 4AC}}{2A}$$

Comparing $$Ax^+Bx+C=0$$ with $$bx^{2}-2ax+a=0$$, A = b, B = -2a, C = a

Hence, the roots = $$\dfrac{2a\pm\sqrt{4a^2 - 4ba}}{2b}$$

x = $$\dfrac{a\pm\sqrt{a^2 - ba}}{b}$$

Let $$x_{1}$$ = $$\dfrac{a-\sqrt{a^2 - ba}}{b}$$, $$x_{2}$$ = $$\dfrac{a+\sqrt{a^2 - ba}}{b}$$

Rationalizing $$x_{1}$$ = $$\dfrac{a-\sqrt{a^2 - ba}}{b}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{a-\sqrt{a^2 - ba}}{b}*\dfrac{a+\sqrt{a^2 - ba}}{a+\sqrt{a^2 - ba}}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{a^2-(a^2 - ba)}{b*(a+\sqrt{a^2 - ba})}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{ab}{b*(a+\sqrt{a^2 - ba})}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{a}{a+\sqrt{a^2 - ba}}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{a}{a+\sqrt{a}*\sqrt{a - b}}$$

$$\Rightarrow$$ $$x_{1}$$ = $$\dfrac{\sqrt{a}}{\sqrt{a}+\sqrt{a - b}}$$

Similarly, $$x_{2}$$ = $$\dfrac{\sqrt{a}}{\sqrt{a}-\sqrt{a - b}}$$

Therefore, x = $$\dfrac{\sqrt{a}}{\sqrt{a}\pm\sqrt{a - b}}$$. Hence, option C is the correct answer.

Three Professors Dr. Gupta, Dr. Sharma and Dr. Singh are evaluating answer scripts of a subject. Dr. Gupta is 40% more efficient than Dr. Sharma, who is 20% more efficient than Dr. Singh. Dr. Gupta takes 10 days less than Dr. Sharma to complete the evaluation work. Dr. Gupta starts the evaluation work and works for 10 days and then Dr. Sharma takes over. Dr. Sharma evaluates for next 15 days and then stops. In how man days, Dr. Singh can complete the remaining evaluation work.

Solution

let G be number of days in which Dr. gupta can complete the evaluation of answer sheet , let Sh be number of days in which Dr. Sharma can complete the evaluation of answer sheet , let Si be number of days in which Dr. Singh can complete the evaluation of answer sheet

Given Dr. Gupta is 40% more efficient than Dr. Sharma therefore number of days required by Dr. Sharma to complete the evaluation of answer sheet = 1.4*G

Dr. Gupta takes 10 days less than Dr. Sharma to complete the evaluation work i.e. 1.4G-G = 10 therefore G = 25 and hence Sh = 35

Also given that Dr. Sharma is 20% more efficient than Dr. Singh therefore number of days required by Dr. Singh to complete the evaluation of answer sheet = $$\frac{35}{1.2}$$ = 42 i.e. Si = 42

Dr. Gupta starts the evaluation work and works for 10 days therefore he completes $$\frac{10}{25}$$ of work then Dr. Sharma takes over. Dr. Sharma evaluates for next 15 days therefore he completes $$\frac{15}{35}$$ of work. Fraction of work left is 1 - $$\frac{10}{25}$$ - $$\frac{15}{35}$$ = $$\frac{6}{35}$$ now time required by Dr. Singh to complete this amount of work is $$\frac{6*42}{35}$$ = 7.2 days

Therefore our answer is option 'A'

If [x] is the greater integer less than or equal to ‘x’, then find the value of the following series $$[\sqrt{1}]+[\sqrt{2}]+[\sqrt{3}]+[\sqrt{4}]+....+[\sqrt{360}]$$

Solution

$$[\sqrt{1}]+[\sqrt{2}]+[\sqrt{3}]+[\sqrt{4}]+....+[\sqrt{360}]$$ = 1 + 1 + 1 + 2 + 2 + 2 + 2 + 2 + 3 + 3 + 3.. 7 times + 4 + 4 +......9 times +.........+ 18 + 18 + ......37 times

= 1*3 + 2*5 + 3*7 + 4*9+............+18*37

= $$\sum_1^{18}$$ n(2n+1)

= $$\sum_1^{18}$$ $$2n^2+n$$

= $$\frac{2n*(n+1)*(2n+1)}{6}$$ + $$\frac{n*(n+1)}{2}$$

= $$\frac{2*18*(19)*(37)}{6}$$ + $$\frac{18*19}{2}$$

= 4389

Therefore our answer is option 'A'

What is the value of $$\sqrt{\frac{a}{b}}$$, If $$\log_{4}\log_{4}4^{a-b}=2\log_{4}(\sqrt{a}-\sqrt{b})+1$$

Solution

$$\sqrt{\frac{a}{b}}$$, If $$\log_{4}\log_{4}4^{a-b}=2\log_{4}(\sqrt{a}-\sqrt{b})+\log_{4}{4}$$

i.e. $$\log_{4}\log_{4}4^{a-b}=\log_{4}((\sqrt{a}-\sqrt{b})^2)*4$$

i.e. $$\log_{4}4^{a-b}=((\sqrt{a}-\sqrt{b})^2)*4$$

i.e. (a-b)*$$\log_{4}4=((\sqrt{a}-\sqrt{b})^2)*4$$

i.e. a-b = 4a+4b-8$$\sqrt{ab}$$

i.e. 3a + 5b - 8$$\sqrt{ab}$$ = 0

i.e. $$3\sqrt\frac{a}{b}^2$$ - 8$$\sqrt\frac{a}{b}$$+5 = 0

put $$\sqrt\frac{a}{b}$$ = t

therefore 3$$t^2$$ - 8t + 5 = 0

solving we get t = 1 or t = $$\frac{5}{3}$$

i.e. $$\sqrt\frac{a}{b}$$ = 1 or $$\frac{5}{3}$$

but if $$\sqrt\frac{a}{b}$$ = 1 then a=b then $$\log_{4}(\sqrt{a}-\sqrt{b})$$ will become indefinite

Therefore $$\sqrt\frac{a}{b}$$ = $$\frac{5}{3}$$

Therefore our answer is option 'C'

Three pipes A, B and C are connected to a tank. These pipes can fill the tank separately in 5 hours, 10 hours and 15 hours respectively. When all the three pipes were opened simultaneously, it was observed that pipes A and B were supplying water at 3/4th of their normal rates for the first hour after which they supplied water at the normal rate. Pipe C supplied water at 2/3rd of its normal rate for first 2 hours, after which it supplied at its normal rate. In how much time, tank would be filled.

Solution

Let the capacity of the tank be 60 litres.

Capacity of the first pipe = 12 l/hr

Capacity of the second pipe = 6 l/hr

Capacity of the third pipe = 4 l/hr

In 2 hrs, first pipe fills (9 + 12) l = 21 l

In 2 hrs, second pipe fills (4.5 + 6) = 10.5 l

In 2 hrs, third pipe fills (16/3) l

In 2 hrs, tank filled = (21 + 10.5 + 5.33) l = 36.83 l

Tank left to be filled = (60 - 36.83) l = 23.17 l

Time required = (23.17/22) hr = 1.05 hrs

Total time = 3.05 hrs

Hence, option C is the correct answer.

The minimum value of $$3^{sinx}+3^{cosx}$$ is

Solution

Using AM $$\geq$$ GM, We can say that

$$\dfrac{3^{sinx}+3^{cosx}}{2}$$ $$\geq$$ $$\sqrt{3^{sinx}*3^{cosx}}$$

$$\Rightarrow$$ $$3^{sinx}+3^{cosx}$$ $$\geq$$ $$2*3^\frac{sinx+cosx}{2}$$ ... (1)

We know that -$$\sqrt{A^2+B^2}$$ $$\leq$$ Asinx+Bcosx $$\leq$$ $$\sqrt{A^2+B^2}$$

Therefore, -$$\sqrt{1^2+1^2}$$ $$\leq$$ sinx+cosx $$\leq$$ $$\sqrt{1^2+1^2}$$

$$\Rightarrow$$ -$$\sqrt{2}$$ $$\leq$$ sinx+cosx $$\leq$$ $$\sqrt{2}$$

Hence, we can say that the minimum value of sinx+cosx = -$$\sqrt{2}$$ ... (2)

From equation (1) and (2) we can say that,

$$\Rightarrow$$ $$3^{sinx}+3^{cosx}$$ $$\geq$$ $$2*3^\frac{-\sqrt{2}}{2}$$

$$\Rightarrow$$ $$3^{sinx}+3^{cosx}$$ $$\geq$$ $$2*3^\frac{-1}{\sqrt{2}}$$

Therefore, option B is the correct answer.

In a B-School there are three levels of faculty positions i.e. Professor, Associate Professor and Assistant Professor. It is found that the sum of the ages of all faculty present is 2160, their average age is 36; the average age of the Professor and Associate Professor is 39; of the Associate Professor and Assistant Professor is $$32\frac{8}{11}$$; of the Professor and Assistant Professor is $$36\frac{2}{3}$$; Had each professor been 1 year older, each Associate Professor 6 years older, and each Assistant Professor 7 years older, then their average age would increase by 5 years. What will be the number of faculty at each level and their average ages?

Solution

Let the number of professors, associate professors and assistant professors be x, y and z respectively and their average ages be a, b and c respectively.

xa + yb + zc = 2160 -------------------(1)

Average age =36

$$\therefore$$ x+y+z=60

xa + yb = 39 (x + y)

11(yb + zc) = 360(y + z)

3(xa + zc) = 110(x + z)

x(a + 1) + y(b + 6) + z(c + 7) = 2160 + 5*(60) -------(2) [$$\because$$ Average increases by 5]

Eq 2- Eq 1

We get x+6y+7z=300

Lets solve the options one by one

Option A: x = 16 , y = 24, z = 20

16+6*24+7*20=300 which satisfies the equations.

So either A or C can be the answer.

Now check for the values of a, b, c

a=45, b=35, c=30

ax+by+cz = 45*16+35*24+30*20

=2160

Hence, option A is the correct answer.

$$\log_{5}{2}$$ is

Solution

Let $$\log_{5}{2}$$ = y

Let us assume $$\log_{5}{2}$$ is a rational number.

$$\log_{5}{2}$$ = p/q, where p and q are co primes.

5^(p/q)=2 => 5^p=2^q.

5^p=5*5*5*5*5*5*5..................p times

2^p=2*2*2*2*2*2*2..................q times

No value of p and q can satisfy the equation. Hence y is an irrational number.

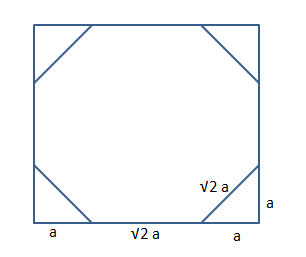

In a square of side 2 meters, isosceles triangles of equal area are cut from the corners to form a regular octagon. Find the perimeter and area of the rectangular octagon.

Solution

Let us assume that 'a' is the length of the side of equal sides of the isosceles triangle.

We can see that $$a+\sqrt{2}*a+a=2$$

$$\Rightarrow$$ a = $$\dfrac{2}{2+\sqrt{2}}$$

Therefore, the perimeter of the regular octagon = $$8*a*\sqrt{2}$$

$$\Rightarrow$$ $$\dfrac{8\sqrt{2}*2}{2+\sqrt{2}}$$

$$\Rightarrow$$ $$\dfrac{16}{1+\sqrt{2}}$$ ... (1)

Area of regular octagon = $$2x^2(1+\sqrt{2})$$ where 'x' is the length of each side.

Here, x = $$a\sqrt{2}$$ = $$\dfrac{2\sqrt{2}}{2+\sqrt{2}}$$ = $$\dfrac{2}{1+\sqrt{2}}$$

Therefore, area of the regular octagon = $$2*(\dfrac{2}{1+\sqrt{2}})^2(1+\sqrt{2})$$ = $$\dfrac{8}{1+\sqrt{2}}$$ =$$\dfrac{8}{1+\sqrt{2}}*\dfrac{1+\sqrt{2}}{1+\sqrt{2}}$$ = $$\dfrac{8*(1+\sqrt{2})}{3+2\sqrt{2}}$$

Hence, we can say that none of the given answer is correct.

The smallest perfect square that is divisible by 7!

Solution

7! can be broken into prime factors.

7! = 1*2*3*4*5*6*7 = $$2^4*3^2*5*7$$

Hence, the smallest perfect square which is divisible by 7! will $$2^4*3^2*5^2*7^2$$ = 5040*5*7 = 176400

A survey shows that 61%, 46% and 29% of the people watched “3 idiots”, “Rajneeti” and “Avatar” respectively. 25% people watched exactly two of the three movies and 3% watched none. What percentage of people watched all the three movies?

Solution

Let the number of people who watched exactly one movie be 'a', the number of people who watched exactly two movies be 'b' and the number of people who watched exactly three movies be 'c'

Then, a + b + c = 100 - 3 = 97 ...............(i)

also, a + 2b + 3c = 61 + 46 + 29 = 136.......................(ii)

On subtracting (i) from (ii), we get

b + 2c = 39

It is given that, b = 25

So, c = 7

Therefore, 7% people watched all the three movies.

Hence, option D is the correct answer.

In a triangle ABC the length of side BC is 295. If the length of side AB is a perfect square, then the length of side AC is a power of 2, and the length of side AC is twice the length of side AB. Determine the perimeter of the triangle.

Solution

Let AC = $$2^k$$

AC = 2 * AB

So, AB = $$2^{k - 1}$$

Only 256 and 512 satisfy this condition as the third side is 295 and we have to ensure that sum of the two sides of the triangle is greater than the third side.

Thus, the perimeter = (256 + 512 + 295) = 1063.

Hence, option C is the correct answer.

In a Green view apartment, the houses of a row are numbered consecutively from 1 to 49. Assuming that there is a value of ‘x’ such that the sum of the numbers of the houses preceding the house numbered ‘x’ is equal to the sum of the numbers of the houses following it. Then what will be the value of ‘x’?

Solution

It is given that sum of the first $$(x - 1)$$ numbers is equal to sum of the numbers from $$(x + 1)$$ to 49

or, sum of $$(x - 1)$$ numbers = sum of first 49 numbers - sum of first $$x$$ numbers

$$\dfrac{x(x - 1)}{2} = \dfrac{49 * 50}{2} - \dfrac{x(x + 1)}{2}$$

On solving, we get $$x$$ = 35

Hence, option C is the correct answer.

To start a new enterprise, Mr. Yogesh has borrowed a total of Rs. 60,000 from two money lenders with the interest being compounded annually, to be repaid at the end of two years. Mr. Yogesh repaid Rs.38, 800 more to the first money lender compared to the second money lender at the end of two years. The first money lender charged an interest rate, which was 10% more than what was charged by the second money lender. If Mr. Yogesh had instead borrowed Rs. 30,000 from each at their respective initial rates for two years, he would have paid Rs.7, 500 more to the first money lender compared to the second. Then money borrowed by Mr. Yogesh from first money lender is?

Solution

Let the interest on the second part be $$r$$ %

Then, the rate on the first part = ($$r$$ + 10)%It is given that,

$$30000(1 + \dfrac{r + 10}{100})^2 - 30000(1 + \dfrac{r}{100})^2 = 7500$$

On solving, we get $$r$$ = 20%

Let the first part be Rs. $$a$$

Then, the second part = Rs. (60000 - $$a$$)

$$a(1 + \dfrac{20 + 10}{100})^2 - (60000 - a)(1 + \dfrac{20}{100})^2$$ = 38800

On solving, we get $$a$$ = Rs. 40000

Hence, option C is the correct answer.

Find the coefficient of $$x^{12}$$ in the expansion of $$(1 - x^{6})^{4}(1 - x)^{-4}$$

Solution

We can write $$(1 - x^{6})^{4}$$ = $$4C0(1)^4(x^6)^0$$ - $$4C1(1)^3(x^6)^1$$ + $$4C2(1)^2(x^6)^2$$ - $$4C3(1)^1(x^6)^3$$+ $$4C4(1)^0(x^6)^4$$

$$\Rightarrow$$ $$(1 - x^{6})^{4}= (1-4x^6+6x^{12}-4x^{18}+x^{24})$$

Therefore, we can say

$$(1 - x^{6})^{4}(1 - x)^{-4}=(1-4x^6+6x^{12}-4x^{18}+x^{24})*(1 - x)^{-4}$$

We have to find out coefficient of $$x^{12}$$, $$x^6$$, $$x^0$$ in $$(1 - x)^{-4}$$.

We can use binomial expansion for negative coefficients. Therefore, coefficient of $$x^{12}$$ in $$(1 - x)^{-4}$$

$$\Rightarrow$$ $$\dfrac{(-4)*(-4-1)*(-4-2)* ... *(-4-11)}{12!}$$

$$\Rightarrow$$ $$\dfrac{15!}{12!*3!}$$

$$\Rightarrow$$ $$\dfrac{15*14*13}{3*2*1}$$

$$\Rightarrow$$ $$455$$

Similarly, coefficient of $$x^6$$ in $$(1 - x)^{-4}$$

$$\Rightarrow$$ $$\dfrac{(-4)*(-4-1)*(-4-2)* ... *(-4-5)}{6!}$$

$$\Rightarrow$$ $$\dfrac{9!}{6!*3!}$$

$$\Rightarrow$$ $$\dfrac{7*8*9}{3*2*1}$$

$$\Rightarrow$$ $$84$$

Coefficient of $$x^0$$ in $$(1 - x)^{-4}$$ is 1.

Therefore, we can say that the coefficient of $$x^{12}$$ in the expansion of $$(1 - x^{6})^{4}(1 - x)^{-4}$$ = 455+(-4*84)+(1*6) = 125. Hence, option C is the correct answer.

Alternative Solution:

$$(1-x^6)^4 = (1-x)^4(1+x+x^2+x^3+x^4+x^5)^4$$

$$\Rightarrow (1-x^6)^4(1-x)^{-4} = (1+x+x^2+x^3+x^4+x^5)^4$$

Hence we need to find coeff of $$x^{12}$$ in $$(1+x+x^2+x^3+x^4+x^5)^4$$

= $$(1+x+x^2+x^3+x^4+x^5)\times$$

$$(1+x+x^2+x^3+x^4+x^5)\times$$

$$(1+x+x^2+x^3+x^4+x^5)\times$$

$$(1+x+x^2+x^3+x^4+x^5)$$

This will be equal to number of integral solutions for a + b + c + d = 12, 0<=a,b,c,d<=4

a is the power of x from the first expression, b is the power of x

Lets find the set of values for (a,b,c,d)

(5,5,2,0) => Number of ways of arranging = 4!/2! = 12

(5,5,1,1) => Number of ways of arranging = 4!/(2!*2!) = 6

(5,4,3,0) => Number of ways of arranging = 4! = 24

(5,4,2,1) => Number of ways of arranging = 4! = 24

(5,3,2,2) => Number of ways of arranging = 4!/2! = 12

(5,3,3,1) => Number of ways of arranging = 4!/2! = 12

(4,4,4,0) => Number of ways of arranging = 4!/3! = 4

(4,4,3,1) => Number of ways of arranging = 4!/2! = 12

(4,4,2,2) => Number of ways of arranging = 4!/(2!*2!) = 6

(4,3,3,2) => Number of ways of arranging = 4!/2! = 12

(3,3,3,3) => Number of ways of arranging = 4!/4! = 1

Hence the coeff of $$x^{12}$$ = 24*2 + 12*5 + 6*2 + 4 + 1 = 125

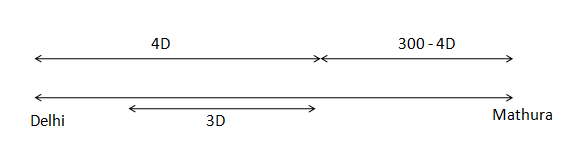

Mukesh, Suresh and Dinesh travel from Delhi to Mathura to attend Janmasthmi Utsav. They have a bike which can carry only two riders at a time as per traffic rules. Bike can be driven only by Mukesh. Mathura is 300Km from Delhi. All of them can walk at 15Km/Hrs. All of them start their journey from Delhi simultaneously and are required to reach Mathura at the same time. If the speed of bike is 60Km/Hrs then what is the shortest possible time in which all three can reach Mathura at the same time.

Solution

Let us assume that Mukesh and Suresh started on bike from Delhi to Mathura and Dinesh started walking at the same time. Mukesh drops Suresh in a mid-way such that Suresh will take same time to reach Mathura with Mukesh and Dinesh. In the same time Mukesh will turn back and will pick up Dinesh.

Let us assume that '4D' is the distance covered by by Mukesh and Suresh. Then Suresh must have covered remaining 300 - 4D kms by walking at 15 km/hr. When Mukesh dropped Suresh by that time Dinesh have already covered D kms and now Mukesh and Dinesh and would have 3D kms apart. Since Mukesh is 4 times faster than Dinesh, Mukesh would have covered (4/5) of 3D kms.

In addition to this, Mukesh and Dinesh have to cover 2.4D+300-4D kms to reach Mathura at 60 km/hr.

By equating the time taken by Mukesh and Suresh to reach Mathura after the point when Mukesh dropped Suresh,

$$\dfrac{300-4D}{15}=\dfrac{2.4D+2.4D+300-4D}{60}$$

$$\Rightarrow$$ 16.8*D = 900

$$\Rightarrow$$ D = $$\dfrac{375}{7}$$ kms

Therefore, minimum time taken by them to finish the journey = $$\dfrac{4D}{60}+\dfrac{300-4D}{15}$$

$$\Rightarrow$$ $$20 - \dfrac{D}{5}$$

$$\Rightarrow$$ $$20 - \dfrac{375}{7*5}$$

$$\Rightarrow$$ $$20 - \dfrac{75}{7}$$

$$\Rightarrow$$ $$\dfrac{65}{7}$$ or $$9\dfrac{2}{7}$$ hours. Hence, option B is the correct answer.

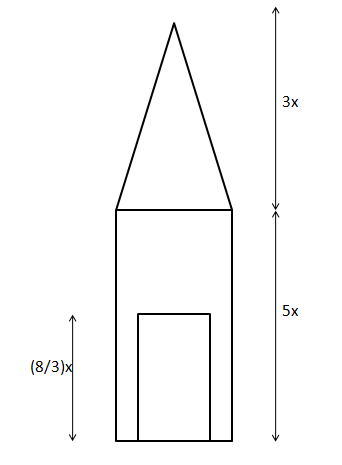

In a rocket shape firecracker, explosive powder is to be filled up inside the metallic enclosure. The metallic enclosure is made up of a cylindrical base and conical top with the base of radius 8 centimeter. The ratio of height of cylinder and cone is 5:3. A cylindrical hole is drilled through the metal solid with height one third the height of the metal solid. What should be the radius of the hole, so that volume of the hole (in which gun powder is to be filled up) is half of the volume of metal solid after drilling?

Solution

Let us draw an appropriate diagram. Let us assume that 'R' is the radius of the hole.

$$\dfrac{1}{2}$$*(Total volume - Volume of the hole) = Volume of the hole

Volume of the hole = $$\dfrac{1}{3}*\text{Total volume of the rocket}$$

$$\pi*R^2*(8/3)x$$ = $$\dfrac{1}{3}*(\pi*8^2*5x+\dfrac{1}{3}*\pi*8^2*3x)$$

$$R^2*(8/3)$$ = $$\dfrac{1}{3}*(8^2*5+\dfrac{1}{3}*8^2*3)$$

$$R^2 = 48$$

$$R$$ = $$4\sqrt{3}$$ cm. Hence, option A is the correct answer.

A small and medium enterprise imports two components A and B from Taiwan and China respectively and assembles them with other components to form a toy. Component A contributes to 10% of production cost. Component B contributes to 20% of the production cost. Usually the company sells this toy at 20% above the production cost. Due to increase in the raw material and labour cost in both the countries, component A became 20% costlier and component B became 40% costlier. Owing to these reasons the company increased its selling price by 15%. Considering that cost of other components does not change, what will be the profit percentage, if the toy is sold at the new price?

Solution

Let the production cost be Rs. 100

The, Selling Price = Rs. 120

Price of component A = Rs. 10

Price of component B = Rs. 20

Price of other components = Rs. (100 - 10 - 20) = Rs. 70

After increase in prices,

Price of component A = Rs. 12

Price of component B = Rs. 28

Price of other components = Rs. 70

Total Cost of production = Rs. (12 + 28 + 70) = Rs. 110

Selling price = Rs. (1.15 * 120) = Rs. 138

Profit = Rs. 28

Profit % = 25.45%

Hence, option B is the correct answer.

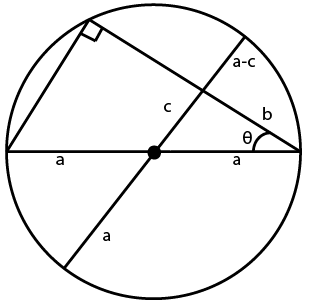

What is the value of $$c^{2} $$ in the given figure, where the radius of the circle is ‘a’ unit.

Solution

Applying the cosine rule , we get $$c^{2} = a^{2} + b^{2} - 2ab cos θ$$

Hence, option A is the correct answer.

How many subsets of {1, 2, 3 ... 11} contain at least one even integer?

Solution

Total number of subsets that can be formed with the left of 11 elements = $$2^{11}$$ = 2048

The number of subsets which contain only odd numbers(1, 3, 5, 7, 9, 11} = $$2^{6}$$ = 64

Number of subsets which contain at least one even integer = Total number of subsets - the number of subsets which contain only odd numbers

$$\Rightarrow$$ 2048 - 64 = 1984. Hence, option C is the correct answer.

Read the following information and choose the right alternative in the questions that follow.

During the cultural week of an institute six competitions were conducted. The cultural week was inaugurated in the morning of 19th October, Wednesday and continued till 26th October. In the span of 8 days six competitions namely debate, folk dance, fash-p, street play, rock band, and group song, were organized along with various other cultural programs. The information available from the institute is:

i. Only one competition was held in a day

ii. Rock band competition was not conducted on the closing day.

iii. Fash-p was conducted on the day prior to debate competition

iv. Group song competition was conducted neither on Wednesday nor on Saturday

v. None of the competition was conducted on Thursday and Sunday

vi. Street Play competition was held on Monday

vii. There was gap of two days between debate competition and group song competition

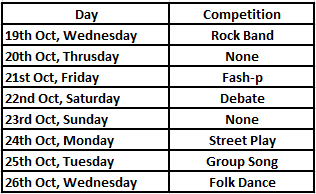

The cultural week started with which competition?

Solution

Let us draw a table consisting the day and competition.

In statement 5, it is given that none of the competition was conducted on Thursday and Sunday. Also, Street Play competition was held on Monday.

It is given that Group Song competition was conducted neither on Wednesday nor on Saturday. Hence, the Group Song competition can take place on either Tuesday or Friday. We are also given that there was gap of two days between Debate competition and Group Song competition.

If the Group Song competition is on Friday, then Debate competition should take place in 24th Oct, Monday but that slot is already filled. Hence, this case is not possible. Therefore, we can say that Group Song competition was on Tuesday. Consecutively, we can say that the Debate competition was on Saturday.

Rock band competition was not conducted on the closing day. Hence, we can say that Rock Band competition took place on either 19th Oct or 21st Oct.

It is also given that Fash-p was conducted on the day prior to debate competition. Hence, we can say that Fash-P was conducted on 21st Oct Friday. Consequently, we can say that Rock Band competition took place on 19th Oct Wednesday.

Also, we can say that folk dance competition held on 26th Oct.

From the table, we can see that the cultural week started with Rock Band. Hence, option D is the correct answer.

How many days gap is there between rock band competition and group song competition?

Solution

Let us draw a table consisting the day and competition.

In statement 5, it is given that none of the competition was conducted on Thursday and Sunday. Also, Street Play competition was held on Monday.

It is given that Group Song competition was conducted neither on Wednesday nor on Saturday. Hence, the Group Song competition can take place on either Tuesday or Friday. We are also given that there was gap of two days between Debate competition and Group Song competition.

If the Group Song competition is on Friday, then Debate competition should take place in 24th Oct, Monday but that slot is already filled. Hence, this case is not possible. Therefore, we can say that Group Song competition was on Tuesday. Consecutively, we can say that the Debate competition was on Saturday.

Rock band competition was not conducted on the closing day. Hence, we can say that Rock Band competition took place on either 19th Oct or 21st Oct.

It is also given that Fash-p was conducted on the day prior to debate competition. Hence, we can say that Fash-P was conducted on 21st Oct Friday. Consequently, we can say that Rock Band competition took place on 19th Oct Wednesday.

Also, we can say that folk dance competition held on 26th Oct.

From the table, we can see that there is a gap of 5 days between rock band competition and group song competition. Hence, option D is the correct answer.

Which pair of competition was conducted on Wednesday?

Solution

Let us draw a table consisting the day and competition.

In statement 5, it is given that none of the competition was conducted on Thursday and Sunday. Also, Street Play competition was held on Monday.

It is given that Group Song competition was conducted neither on Wednesday nor on Saturday. Hence, the Group Song competition can take place on either Tuesday or Friday. We are also given that there was gap of two days between Debate competition and Group Song competition.

If the Group Song competition is on Friday, then Debate competition should take place in 24th Oct, Monday but that slot is already filled. Hence, this case is not possible. Therefore, we can say that Group Song competition was on Tuesday. Consecutively, we can say that the Debate competition was on Saturday.

Rock band competition was not conducted on the closing day. Hence, we can say that Rock Band competition took place on either 19th Oct or 21st Oct.

It is also given that Fash-p was conducted on the day prior to debate competition. Hence, we can say that Fash-P was conducted on 21st Oct Friday. Consequently, we can say that Rock Band competition took place on 19th Oct Wednesday.

Also, we can say that folk dance competition held on 26th Oct.

From the table, we can see that Rock Band and Folk Dance were conducted on Wednesdays.

Hence, option C is the correct answer.

Which competition exactly precedes the street play competition?

Solution

Let us draw a table consisting the day and competition.

In statement 5, it is given that none of the competition was conducted on Thursday and Sunday. Also, Street Play competition was held on Monday.

It is given that Group Song competition was conducted neither on Wednesday nor on Saturday. Hence, the Group Song competition can take place on either Tuesday or Friday. We are also given that there was gap of two days between Debate competition and Group Song competition.

If the Group Song competition is on Friday, then Debate competition should take place in 24th Oct, Monday but that slot is already filled. Hence, this case is not possible. Therefore, we can say that Group Song competition was on Tuesday. Consecutively, we can say that the Debate competition was on Saturday.

Rock band competition was not conducted on the closing day. Hence, we can say that Rock Band competition took place on either 19th Oct or 21st Oct.

It is also given that Fash-p was conducted on the day prior to debate competition. Hence, we can say that Fash-P was conducted on 21st Oct Friday. Consequently, we can say that Rock Band competition took place on 19th Oct Wednesday.

Also, we can say that folk dance competition held on 26th Oct.

From the table, we can see that Debate competition precedes the street play competition. Hence, option C is the correct answer.

Fash-p competition follows which competition?

Solution

Let us draw a table consisting the day and competition.

In statement 5, it is given that none of the competition was conducted on Thursday and Sunday. Also, Street Play competition was held on Monday.

It is given that Group Song competition was conducted neither on Wednesday nor on Saturday. Hence, the Group Song competition can take place on either Tuesday or Friday. We are also given that there was gap of two days between Debate competition and Group Song competition.

If the Group Song competition is on Friday, then Debate competition should take place in 24th Oct, Monday but that slot is already filled. Hence, this case is not possible. Therefore, we can say that Group Song competition was on Tuesday. Consecutively, we can say that the Debate competition was on Saturday.

Rock band competition was not conducted on the closing day. Hence, we can say that Rock Band competition took place on either 19th Oct or 21st Oct.

It is also given that Fash-p was conducted on the day prior to debate competition. Hence, we can say that Fash-P was conducted on 21st Oct Friday. Consequently, we can say that Rock Band competition took place on 19th Oct Wednesday.

Also, we can say that folk dance competition held on 26th Oct.

From the table, we can see that Fash-p follows Rock Band. Hence, option C is the correct answer.

Read the information given below and answer the questions that follow the information.

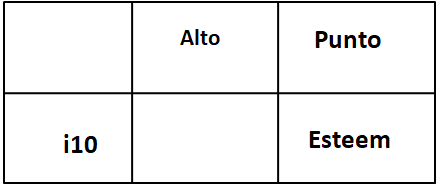

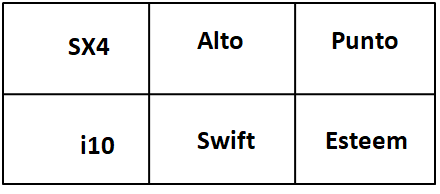

A parking lot can accommodate only six cars. The six cars are parked in two rows in such a way that the front of the three cars parked in one row is facing the other three cars in the other row.

i. Alto is not parked in the beginning of any row

ii. Esteem is second to the right of i10

iii. Punto, who is the neighbor of Alto is parked diagonally opposite to i10

iv. Swift is parked in front of Alto

v. SX4 is parked to the immediate right of Alto

If SX4 and Esteem exchange their positions mutually then car (s) adjacent to Esteem is (are)?

Solution

It is given that Esteem is second to the right of i10. Punto, who is the neighbor of Alto is parked diagonally opposite to i10. We can draw the diagram as shown in the figure below.

Swift is parked in front of Alto and SX4 is parked to the immediate right of Alto.

We have arranged all six cars according to the conditions given in the question.

Now we are asked to interchange SX4 and Esteem's positions mutually and then figure out the car(s) adjacent to Esteem. These cars should be same as SX4 in the original arrangement. From the diagram, we can see that only Alto will be adjacent to Esteem in new position. Therefore, option C is the correct answer.

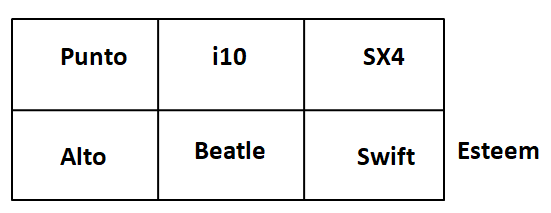

If Alto changes position with i10 and Punto changes position with SX4 and Swift shifts one position to the right to accommodate Beatle then the car (s) parked adjacent to Beatle is (are)?

Solution

It is given that Esteem is second to the right of i10. Punto, who is the neighbor of Alto is parked diagonally opposite to i10. We can draw the diagram as shown in the figure below.

Swift is parked in front of Alto and SX4 is parked to the immediate right of Alto.

We have arranged all six cars according to the conditions given in the question.

It is given that Alto changes position with i10 and Punto changes position with SX4 and Swift shifts one position to the right to accommodate Beatle.

From, the arrangement we can see that Alto and Swift are neighbors of Beatle. Hence, option D is the correct answer.

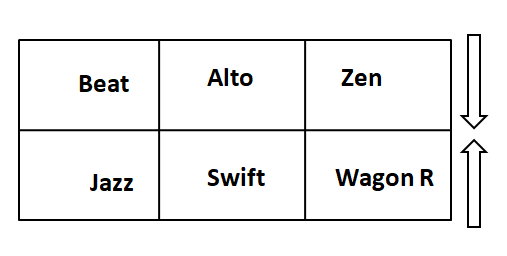

In the original parking scheme four new cars enter the parking lot such that Wagon-R is second to the right of i10 and Zen is second to the left of SX4. Jazz is parked second to the left to Wagon-R and Beat is parked to the right of Alto then the cars that moved out are?

Solution

It is given that Esteem is second to the right of i10. Punto, who is the neighbor of Alto is parked diagonally opposite to i10. We can draw the diagram as shown in the figure below.

Swift is parked in front of Alto and SX4 is parked to the immediate right of Alto.

We have arranged all six cars according to the conditions given in the question.

In the original parking scheme four new cars enter the parking lot such that Wagon-R is second to the right of i10 and Zen is second to the left of SX4. Jazz is parked second to the left to Wagon-R and Beat is parked to the right of Alto. Let us place 4 news cars - WagonR, Zen, Jazz and Beat.

Hence, we can say that i10, Punto, SX4 and Esteem are moved out. Therefore, option D is the correct answer.

Read the information given below and answer the next five questions that follow :

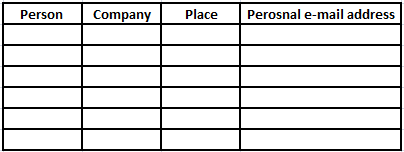

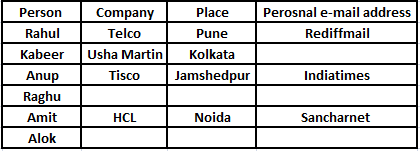

i. Six friends Rahul, Kabeer, Anup, Raghu, Amit and Alok were engineering graduates. All six of them were placed in six different companies and were posted in six different locations, namely Tisco- Jamshedpur, Telco-Pune, Wipro-Bangalore, HCL- Noida, Mecon-Ranchi and Usha Martin-Kolkata. Each of them has their personal e-mail id’s with different email providers i.e., Gmail, Indiatimes, Rediffmail, Yahoo, Hotmail, Sancharnet, though not necessarily in the same order.

ii. The one having e-mail account with Sancharnet works in Noida and the one having an e-mail account with Indiatimes works for Tisco.

iii. Amit does not stay in Bangalore and does not work for Mecon, the one who works for Mecon has an e-mail id with Gmail.

iv. Rahul has an e-mail id with Rediffmail and works at Pune.

v. Alok does not work for Mecon and the one who works for Wipro does not have an e-mail account with Yahoo.

vi. Kabeer is posted in Kolkata, and does not have an account with Hotmail.

vii. Neither Alok nor Raghu work in Noida.

viii. The one who is posted in Ranchi has an e-mail id which is not an account of Rediffmail or Hotmail.

ix. Anup is posted in Jamshedpur.

The man who works in Wipro has a e-mail account with?

Solution

Let us draw the table first.

It is given that Anup is posted in Jamshedpur and Kabir is posted in Kolkata. Also, Rahul has an e-mail id with Rediffmail and works at Pune.

It is given that neither Alok nor Raghu work in Noida. Hence, we can say that Amit work in HCL-Noida. Also, the one having e-mail account with Sancharnet works in Noida. Hence we can say that Amit has Sancharnet's email address.

Also, the one having an e-mail account with Indiatimes works for Tisco. Hence, we can say that Anup has Indiatimes's email account.

Alok does not work for Mecon. Hence, we can say that Raghu works in Mecon-Ranchi. Consequently, we can say that Alok work in Wipro-Bangalore.

Also, the one who works for Mecon has an e-mail id with Gmail.

The one who works for Wipro does not have an e-mail account with Yahoo. Hence, we can say that Kabeer has yahoo's email account and Alock has hotmail's email account.

From the table, we can see that the man who works in Wipro has a e-mail account with hotmail. Hence, option D is the correct answer.

Which of the following e-mail-place of posting- person combination is correct?

Solution

Let us draw the table first.

It is given that Anup is posted in Jamshedpur and Kabir is posted in Kolkata. Also, Rahul has an e-mail id with Rediffmail and works at Pune.

It is given that neither Alok nor Raghu work in Noida. Hence, we can say that Amit work in HCL-Noida. Also, the one having e-mail account with Sancharnet works in Noida. Hence we can say that Amit has Sancharnet's email address.

Also, the one having an e-mail account with Indiatimes works for Tisco. Hence, we can say that Anup has Indiatimes's email account.

Alok does not work for Mecon. Hence, we can say that Raghu works in Mecon-Ranchi. Consequently, we can say that Alok work in Wipro-Bangalore.

Also, the one who works for Mecon has an e-mail id with Gmail.

The one who works for Wipro does not have an e-mail account with Yahoo. Hence, we can say that Kabeer has yahoo's email account and Alock has hotmail's email account.

From the table, we can see that Raghu-Ranchi-Gmail is a correct combination. Hence, option D is the correct answer.

Which of the following is true?

Solution

Let us draw the table first.

It is given that Anup is posted in Jamshedpur and Kabir is posted in Kolkata. Also, Rahul has an e-mail id with Rediffmail and works at Pune.

It is given that neither Alok nor Raghu work in Noida. Hence, we can say that Amit work in HCL-Noida. Also, the one having e-mail account with Sancharnet works in Noida. Hence we can say that Amit has Sancharnet's email address.

Also, the one having an e-mail account with Indiatimes works for Tisco. Hence, we can say that Anup has Indiatimes's email account.

Alok does not work for Mecon. Hence, we can say that Raghu works in Mecon-Ranchi. Consequently, we can say that Alok work in Wipro-Bangalore.

Also, the one who works for Mecon has an e-mail id with Gmail.

The one who works for Wipro does not have an e-mail account with Yahoo. Hence, we can say that Kabeer has yahoo's email account and Alock has hotmail's email account.

From the table, we can see that Kabeer has an e-mail id with Yahoo. Hence, option C is the correct answer.

Which of the following sequences of location represent Alok, Kabeer, Anup, Rahul, Raghu, and Amit in the same order?

Solution

Let us draw the table first.

It is given that Anup is posted in Jamshedpur and Kabir is posted in Kolkata. Also, Rahul has an e-mail id with Rediffmail and works at Pune.

It is given that neither Alok nor Raghu work in Noida. Hence, we can say that Amit work in HCL-Noida. Also, the one having e-mail account with Sancharnet works in Noida. Hence we can say that Amit has Sancharnet's email address.

Also, the one having an e-mail account with Indiatimes works for Tisco. Hence, we can say that Anup has Indiatimes's email account.

Alok does not work for Mecon. Hence, we can say that Raghu works in Mecon-Ranchi. Consequently, we can say that Alok work in Wipro-Bangalore.

Also, the one who works for Mecon has an e-mail id with Gmail.

The one who works for Wipro does not have an e-mail account with Yahoo. Hence, we can say that Kabeer has yahoo's email account and Alock has hotmail's email account.

From the table, we can see that Alok, Kabeer, Anup, Rahul, Raghu, and Amit work in Bangalore, Kolkata, Jamshedpur, Pune, Ranchi and Noida in that order. None of the option represents the same sequence. Hence, option D is the correct answer.

People who have e-mail account with Indiatimes, Sancharnet and Yahoo work for which companies, in the same sequence as the e-mail accounts mentioned?

Solution

Let us draw the table first.

It is given that Anup is posted in Jamshedpur and Kabir is posted in Kolkata. Also, Rahul has an e-mail id with Rediffmail and works at Pune.

It is given that neither Alok nor Raghu work in Noida. Hence, we can say that Amit work in HCL-Noida. Also, the one having e-mail account with Sancharnet works in Noida. Hence we can say that Amit has Sancharnet's email address.

Also, the one having an e-mail account with Indiatimes works for Tisco. Hence, we can say that Anup has Indiatimes's email account.

Alok does not work for Mecon. Hence, we can say that Raghu works in Mecon-Ranchi. Consequently, we can say that Alok work in Wipro-Bangalore.

Also, the one who works for Mecon has an e-mail id with Gmail.

The one who works for Wipro does not have an e-mail account with Yahoo. Hence, we can say that Kabeer has yahoo's email account and Alock has hotmail's email account.

From the table, we can see that people who have e-mail account with Indiatimes, Sancharnet and Yahoo work Tisco, HCL and Usha Martin in that order. Hence, option D is the correct answer.

For the following questions answer them individually

How many ‘zeroes’ are there in the following sequence which are immediately preceded by a nine but not immediately followed by seven?

7090070890702030045703907

Solution

We can see that only one zero present in the number such that it is immediately preceded by a nine but not immediately followed by seven. It is shown in round braces. 4th from the left.

709(0)070890702030045703907

Therefore, option A is the correct answer.

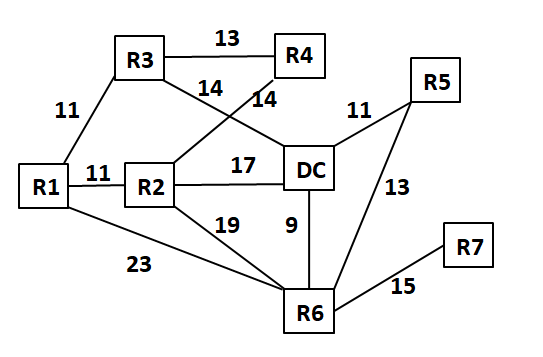

A Retail chain has seven branches in a city namely R1, R2, R3, R4, R5, R6, R7 and a central distribution center (DC). The nearest branch to the DC is R6 which is in the south of DC and is 9 Km away from DC. R2 is 17 Km away from DC in the west. The branch R1 is 11 Km away R2 further in the west. The branch R3 is 11 Km in the north east of R1. R4 is 13 Km from R3 in the east. R5 is 11 Km in the north east of the distribution center. In the north east of R6 is R7 and distance between them is 15 Km. The distance between R1 and R6, R2 and R6, R6 and R5 is 23 Km, 19 Km, 13 Km respectively. R3 is 14 Km away from the DC in the north west direction, while R2 is also 14 Km away from R4 in the north east direction of R2. A truck carrying some goods starts from the distribution center and has to cover at least four stores in a single trip. There is an essential good that has to be delivered in the store R7, but the delivery at R7 has to be done in the end, so what is the shortest distance the truck would travel?

Solution

Let us draw the network diagram according to the given info.

The shortest route for the truck would be DC-R3-R1-R6-R7.

Thus, the total distance traveled would be 14 + 11 + 23 + 15 = 63 km. Hence, option C is the correct answer.

Following graph represents the cost per square feet of four retailers from the financial year 2004 to 2012. The expected cost per square feet for year 2010, 2011 and 2012 are fore casted figures.

Which retailer shows the sharpest decline in cost per square feet and in which year?

Solution

Let us check the option one by one.

(A) For Westside, the decline in cost per square feet in the year 2005 = $$2411-1724$$ = 687

(B) For Pantaloon, the decline in cost per square feet in the year 2008 = $$2044-1656$$ = 388

(C) For S. Stop, the decline in cost per square feet in the year 2009 = $$2419-2197$$ = 222

(D) For Vishal, the decline in cost per square feet in the year 2010 = $$1659-1064$$ = 595

We can see that the sharpest decline is for Westside stores in the year 2005. Hence, option A is the correct answer.

Which retailer has shown the maximum increase in its cost per square feet and in which year?

Solution

Let us check the option one by one.

(A) For S. Stop, the increase in cost per square feet in the year 2006 = $$2135-1889$$ = 246

(B) For S. Stop, the increase in cost per square feet in the year 2007 = $$2464-2135$$ = 329

(C) For Pantaloon, the increase in cost per square feet in the year 2006 = $$1996-1729$$ = 267

(D) For Vishal, the increase in cost per square feet in the year 2006 = $$1802-1832$$ = -30

We can see that the maximum increase in its cost per square feet is for S.stop stores in the year 2007. Hence, option B is the correct answer.

What is the average rate of change in the cost per square feet of the retail sector, if the sector is represented by the above four retailers in the period FY07 to FY10E?

Solution

The cost per square feet of the retail sector, in the year 2007 = 2044+2464+1751+1525 = 7784

The cost per square feet of the retail sector, in the year 2010E = 1396+2230+1064+1051 = 5741

Therefore, What is the average rate of change in the cost per square feet of the retail sector for the given period = $$\dfrac{\dfrac{5741-7784}{7784}\times 100}{3}$$ = $$-8.74$$ percent. Hence, option D is the correct answer.

The table below represents the information collected by TRAI about the Service Area wise Access of (Wireless + Wire line) subscribers in India. On the basis of the information provided in the table answer the questions that follow.

Which service area has observed maximum rate of change from Dec 2009 to March 2010 (in percentage)?

Solution

The percentage change in number of subscribers in March 10 as compared to Dec 09 in U.P. (E) = $$\dfrac{45.53-39.68}{39.68}$$ = 14.74 percent

The percentage change in number of subscribers in March 10 as compared to Dec 09 in Bihar = $$\dfrac{38.36-33.17}{33.17}$$ = 15.64 percent

The percentage change in number of subscribers in March 10 as compared to Dec 09 in Orissa = $$\dfrac{15.89-13.57}{13.57}$$ = 17.09 percent

The percentage change in number of subscribers in March 10 as compared to Dec 09 in Haryana = $$\dfrac{14.96-13.59}{13.59}$$ = 10.08 percent

We can see that Orissa observed maximum rate of change from Dec 2009 to March 2010. Hence, option C is the correct answer.

As a result of a decisions to allow only two or three telecom operator in a particular service area, TRAI allocates R-Com and Vodafone to operate only in the east of India and Idea and Airtel operate only in south. R-Com has got 28% subscribers in the east while Vodafone has 72% subscribers; similarly Idea has 48% subscribers in the south while Airtel has 52% subscribers. How many subscribers do these four players have in 2010?

Solution

It is given that R-com has 28% subscribers in the east and Vodafone has 72% subscribers in the east, these two are the only operators in the east.

Similarly, Idea and Airtel are the only players in the south whose shares are 48% and 52% respectively.

We are not given that name of the states which need to be considered under southern part of the country. But the number of subscribers should be in the same ratio of shares.

Checking with the options

Option (A): R-Com's share = $$\dfrac{28.03}{28.03+73.22}\times 100$$ = 27.68 percent. We are given that Rcom has 28% shares. Hence, this option is incorrect.

Option (B): R-Com's share = $$\dfrac{30.03}{30.03+72.82}\times 100$$ = 29.19 percent. We are given that Rcom has 28% shares. Hence, this option is incorrect.

Option (C): R-Com's share = $$\dfrac{28.03}{28.03+76.24}\times 100$$ = 26.88 percent. We are given that Rcom has 28% shares. Hence, this option is incorrect.

Option (D): R-Com's share = $$\dfrac{30.03}{30.03+77.22}\times 100$$ = 28 percent. We are given that Rcom has 28% shares. Hence, this option is the correct.

Due to operability issues early in 2010 Madhya Pradesh and entire UP was added to the eastern telecom circle. The telecom operators in Madhya Pradesh and entire UP namely R-Com, Vodafone and Idea had 28%, 40% and 32% subscribers respectively. What is the percentage of subscribers that each player has in the newly formed eastern circle in March 2010?

Solution

This question does not state explicitly that data from the previous question can be used, the percentage break up given in the previous question

cannot be assumed in this question. Hence, the given data is insufficient to solve the given problem. Therefore, option D is the correct answer.

The all India rate of change in number of subscribers from December 2009 to March 2010 is?

Solution

The number of subscribers in Dec 2009 = 562.18 millions.

The number of subscribers in March 2010 = 621.30 millions.

Therefore, the required percentage = $$\dfrac{621.30-562.18}{562.18}\times 100$$ = 10.51 percent. Hence, option B is the correct answer.

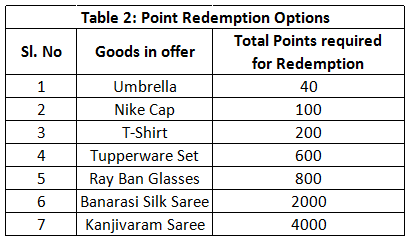

In order to quantify the intangibles and incentives to the multi brand dealers (dealers who stock multiple goods as well as competing brands) and the associated channel members, a Company(X) formulates a point score card, which is called as brand building points. This brand building point is added to the sales target achieved points for redemption. The sales target achieved point is allotted as per the table 3 of this question. The sum of brand building point and sales achieved points is the total point that can be redeemed by the dealer against certain goods, as shown in the second table.

The detail of the system is shown in the tables below

There are 10 multi brand dealers in Nasik and the sales that they have achieved in the end of a quarter are:

Maheshwari & Co has Company X signage along with other brand signage in the main entrance of the store, the exterior walls of the store have the painting of only company X, the side wall in the interior has the painting of Company X. The POP display of Company X is above the eye level with other brands while the stacking of goods of Company X is in the back row of the shelves. The brand building points when combined with the sales achieved points amounts to the total points that a dealer can accumulate in a quarter. The number of Tupperware Sets that Maheshwari & Co can redeem after the quarter (July to September) is?

Solution

In brand building points earned by Maheshwari & Co:

Points earned for having signage board = 10

Points earned for exterior walls of the store = 20

Points earned for Company X painting in the interior of the store = 2.5

Points earned for POP display of company X = 5

Points earned for stacking of company X goods in the shelves = 0

Hence, total brand building points earned by Maheshwari & Co. = 10+20+2.5+5 = 37.50

Also, Maheshwari & Co achieved a tageter more than 100%. Therefore, the sales target points earned by Maheshwari & Co = 15 + (56241-50000)*0.25 = 1575.25.

Therefore, total redeemable points acquired by Maheshwari & Co in Jul-Sep quarter = 1575.25+37.50 = 1612.75.

A tupperware set can be availed by redeeming 600 points. Hence, we can say that Maheshwari & Co can avail 2 Tupperware set by the end of the quarter.

Hence, option A is the correct answer.

Bhowmik Brothers has only other brands signage in the front of the store, and company X painting on the side wall in the exterior of the store, Company X painting on the side wall in the interior of the store, no POP display of any Company and the goods of Company X is stacked in the front row with other brands. What is the total point Bhowmik Brothers need to accumulate to make them eligible for minimum redemption?

Solution

In brand building points earned by Bhowmik Brothers:

Bhowmik Brothers has only other brands signage in the front of the store, and company X painting on the side wall in the exterior of the store, Company X painting on the side wall in the interior of the store, no POP display of any Company and the goods of Company X is stacked in the front row with other brands. What is the total point Bhowmik Brothers need to accumulate to make them eligible for minimum redemption?

Points earned for having signage board of company X = -20

Points earned for painting on the side wall in the exterior of the store = 2.5

Points earned for painting on the side wall in the interior of the store = 2.5

Points earned for POP display of company X = 0

Points earned for stacking of company X goods in the front row with other brands = 10

Hence, total brand building points earned by Bhowmik Brothers = -20+2.5+2.5+10 = -5

Also, Bhowmik Brothers achieved a target in 75% to 99% range. Therefore, the sales target points earned by Bhowmik Brothers = 12

Therefore, total redeemable points acquired by Bhowmik Brothers in Jul-Sep quarter = -5 + 12 = 7.

For minimum redemption they should have at least 40 points. Hence, we can say that Bhowmik Brothers need to accumulate 33 points to make them eligible for minimum redemption. Therefore, option D is the correct answer.

The Brand building points of Saha H/W is 85, and Mr. Saha the proprietor of the store wants to redeem a Kanjivaram Saree the next quarter by carrying forward the points accumulated this quarter to the next quarter. The sales target of Saha H/W is 25,000 units in the next quarter. It is assumed the brand building points for the next quarter is also going to be 85. How many extra units Saha H/W has to sell in order to get the Kanjivaram Saree?

Solution

Total redeemable points earned by Saha H/W in this quarter = 85 + 15 + (24512-24000)*0.25 = 228.

Points earned by Saha H/W through brand building and completing 100% sales target = 85+15 = 100.

For a Kanjivaram Saree, Saha H/W needs 4000 points. Rest of the points should be earned by selling extra units. Each extra units will garner 0.25 points for Mr. Saha.

Therefore, the number of extra units that Mr. Saha must sell in order to collect points for Kanjivaram Saree = $$\dfrac{4000-228-100}{0.25}$$ = 14688.

Hence, option A is the correct answer.

Malling Enterprise exhausted all its points while redeeming three Nike Caps and an Umbrella, what is its brand building points?

Solution

Total point earned by Malling Enterprise through sells alone = 15+(24000-23000)*0.25 = 265.

Points required to avail three Nike Caps and an Umbrella = 3*100+40 = 340.

Hence, Malling Enterprise must have earned through brand building activities = 340 - 265 = 75.

If Srikrishna Trader has 80 brand building points then the goods that it can redeem are _________?

Solution

Total point earned by Srikrishna Trader through sells alone = 15+(42000-40000)*0.25 = 515.

Total point earned by Srikrishna Trader through brand building activities = 80.

Therefore, total redeemable points with Srikrishna Trader = 515+80 = 595.

The tupperware set alone costs 600 points. Hence, option A, B and C can be ruled out. Therefore, option D is the correct answer.

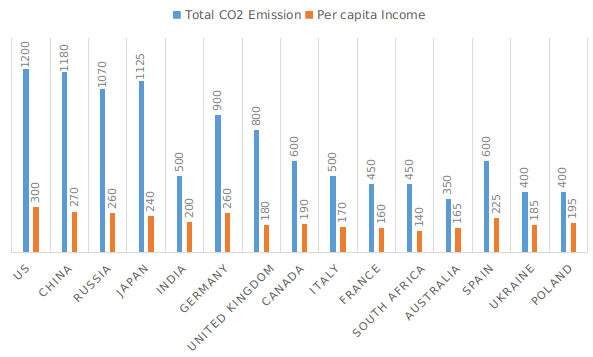

If the world energy council formulates a norm for high emission countries to reduce their emission each year by 12.5% for the next two years then what would be the ratio of $$CO_2$$ emission to per capita income of US, China and Japan after two years. The per capita income of China, Japan and US is expected to increase every year by 4%, 3% and 2% respectively.

Solution

$$CO_2$$ emission by the US after 2 years = $${(1-\dfrac{12.5}{100})}^2\times 1200$$ = 918.75 million tons.

The per capita income in US after 2 years = $${(1+\dfrac{2}{100})}^2\times 300$$ = 312.12

Similarly, we can calculate the $$CO_2$$ emission and per capita income for remaining countries after two years from now.

$$CO_2$$ emission by the China after 2 years = 903.44 million tons.

The per capita income in China after 2 years = $${(1+\dfrac{4}{100})}^2\times 270$$ = 292.032

$$CO_2$$ emission by the Japan after 2 years = 861.33 million tons.

The per capita income in Japan after 2 years = $${(1+\dfrac{3}{100})}^2\times 240$$ = 254.616

Hence, the required ratio = $$\dfrac{918.75}{312.12}$$, $$\dfrac{903.44}{292.032}$$, $$\dfrac{861.33}{254.616}$$, = 2.9, 3.1, 3.4.

Therefore, we can say option C is the correct answer.

If US and China, decide to buy carbon credits, from Spain and Ukraine to make up for their high emissions, then in how many years US, and China would be able to bring down its ratio of $$CO_2$$ emission (million ton) to per capita income to world standard benchmark of 0.75. (per capita income of the given countries remain same, 0.5 $$CO_2$$ emissions [million ton] is compensated by purchase of 1.25 units of carbon credit, and a country can buy carbon credit units in three lots of 15, 20 and 30 units in a single year.)

Solution

CO2 emission required for USA = 225 million tonnes

CO2 emission required for China = 202.5 million tonnes

Required reduction for USA = 975 million tonnes

Required reduction for China = 977.5

O.5 million tone of CO2 ----> 1.25 carbon credits

In one year, a country can purchase 65 carbon credit

In one year, 26 million tonnes of CO2is compensated.

Required time = 977.5 / 26 = 37.59 years

Hence, option B is the correct answer.

France, South Africa, Australia, Ukraine and Poland form an energy consortium which declares $$CO_2$$ emission of 350 million ton per annum as standard benchmark. The energy consortium decides to sell their carbon emission savings against the standard benchmark to high carbon emission countries. It is expected that the per capita income of each country of the energy consortium increases by 2%, 2.5% and 3.5% p.a. for the next three years respectively. The ratio of $$CO_2$$ emission to per capita income of the each energy consortium country reduces by 50% and remains constant for the next three years. By selling 0.5 $$CO_2$$ emissions [million ton] the energy consortium earns 1.25 carbon credits, then determine the total carbon credits earned by energy consortium in three years.

Solution

Total emission in three years combined = 2000 million tonnes.

Thus, total credit = 5000 credits (approx)

Hence, option C is the correct answer.

Select the wrong statement in reference to the position of India vis-à-vis other countries in the graph in terms of the ratio of $$CO_2$$ emission to per capita income (increasing order).

Solution

India stands at 6th position if 200 million ton CO2 emission is deducted from the given CO2 emission figures of each country and 50 is added to the given per capita income of each country.

Hence, option D is the correct answer.

For the following questions answer them individually

Refer to the following pie chart and answer the question that follows. The chart shows the number of units produced in degrees, by Company X in different States of India for the quarter July-Sep 2010.

By how many units does the number of units produced in Bihar exceed the number of units produced in Madhya Pradesh, if the total production in the quarter is 72, 000 units?

Solution

The number of units produced in Bihar exceed the number of units produced in Madhya Pradesh = $$\dfrac{45 - 32.4}{360}\times 72000$$ = 2520.

Therefore, option B is the correct answer.

The following graph shows population data (males and females), educated people data (males and females) and number of male in the population for a given period of 1995 to 2010. All data is in million.

From the information given in the graph answer the questions that follow

In which year the percentage increase in the number of females over the previous year is highest?

Solution

We know that, female population = Total population - Male population.

Therefore, the percentage increase in Female population in 1996 = $$\dfrac{(650-320) - (600-300)}{(600-300)}\times 100$$ = 10%

The percentage increase in Female population in 1999 = $$\dfrac{(750-400) - (700-380)}{(700-380)}\times 100$$ = 9.37%

The percentage increase in Female population in 2004 = $$\dfrac{(845-475) - (800-450)}{(800-450)}\times 100$$ = 5.71%

The percentage increase in Female population in 2005 = $$\dfrac{(900-480) - (845-475)}{(845-475)}\times 100$$ = 13.51%

Hence, option D is the correct answer.

In 2002 if the ratio of number of educated male to professionally educated female was 5:4. If the number of educated males increased by 25% in 2003. What is the percentage change in number of uneducated females in 2003?

Solution

Number of female in the year 2002 = 790 - 440 = 350 million.

Number of educated females in the year 2002 = $$\dfrac{4}{9}\times 545$$ $$\approx$$ 242 millions

Hence, total number of uneducated females in the year 2002 = 350 - 242 = 108 millions ... (1)

Number of educated males in the year 2002 = $$\dfrac{5}{9}\times 545$$ $$\approx$$ 303 millions.

Therefore, the number of educated males in the year 2003 = 1.25*303 = 378.75 millions.

Hence, the number of educated females in the year 2003 = Total educated population - the number of educated males = 560 - 378.75 $$\approx$$ 181.25 millions.

Total number of uneducated females in the year 2003 = Total number of females - the number of educated females = (800-450) - 181 = 169 millions. ... (2)

From equation (2) and (1), we can say that the percentage change in number of uneducated females in 2003 = $$\dfrac{169-108}{108}\times 100$$ $$\approx$$ 56 percent. Hence, we can say that option D is the correct answer.

In year 2005 total population living in urban area is equal to sixty eight percent of educated population. The ratio of number of people living in urban area to people living in rural area is 43:12 in 2010. What is the ratio of the rural population in 2005 to that in 2010?

Solution

In year 2005 total population living in urban area is equal to sixty eight percent of educated population. The ratio of number of people living in urban area to people living in rural area is 43:12 in 2010. What is the ratio of the rural population in 2005 to that in 2010?.

Total population living in urban area in the year 2005 = 0.68*600 = 408 millions.

Therefore, the population living in rural area in the year 2005 = 900 - 408 = 492 millions.

It is given the the ratio of number of people living in urban area to people living in rural area is 43:12 in 2010.

Hence, the number of people living in rural area in the year 2010 = $$\dfrac{12}{55}\times 1100$$ = 240 millions.

Therefore, the required ratio = 492/240 = 2.05.

Kodak decided that traditional film and prints would continue to dominate through the 1980s and that photo finishers, film retailers, and, of course, Kodak itself could expect to continue to occupy their long- held positions until l990. Kodak was right and wrong. The quality of digital cameras greatly improved. Prices plunged because the cameras generally followed Moore's Law, the famous prediction by Intel co-founder Gordon Moore in the l960s that the cost of a unit of computing power would fall by 50 percent every eighteen to twenty-four months. Cameras began to be equipped with what the industry called removable media - those little cards that hold the pictures - so pictures were easier to print or to move to other devices, such as computers. Printers improved. Their costs dropped, too. The Internet caught the popular imagination, and people began e-mailing each other pictures rather than print them.Kodak did little to ready itself for the onslaught of digital technology because it consistently tried to hold on to the profits from its old technology and underestimated the speed with which the new would take hold. Kodak decided it could use digital technology to enhance film, rather than replace it.Instead of preparing for the digital world, Kodak headed off in a direction that cost it dearly. ln 1988, Kodak bought Sterling Drug for $5.1 billion. Kodak had decided it was really a chemicals business, not a photography company. So, Kodak reasoned, it should move into adjacent chemical markets, such as drugs.Well, chemically treated photo paper really isn’t that similar to hormonal agents and cardiovascular drugs.The customers are different. The delivery channels are different. Kodak lost its shirt. lt sold Sterling in pieces in 1994 for about half the original purchase price. George M. C. Fisher was the new CEO of Kodak in 1993. Fisher’s solution was to hold on to the film business as long as possible, while adding a technological veneer to it. For instance, he introduced the Advantix Preview camera, a hybrid of digital and film technology. Users took pictures the way they always had, and the images were captured on film.Kodak spent more than $500 million developing Advantix, which flopped.

Fisher also tried to move Kodak’s traditional retail photo-processing systems into digital world and in this regard installed tens of thousands of image magic kiosks. These kiosks came just as numerous companies introduced inexpensive, high-quality photo printers that people could use at home, which, in fact, is where customers preferred to view their images and fiddle with them. Fisher also tried to insert Kodak as an intermediary in the process of sharing images electronically. He formed partnerships that let customers receive electronic versions of their photos by e-mail and gave them access to kiosks that let them manipulate and reproduce old photographs. You don't need Kodak to upload photos to your computer and e-mail them. Fisher also formed a partnership with AOL called "You've Got Pictures." Customers would have their film developed and posted online, where friends and family could view them. Customers would pay AOL $7 for this privilege, on top of the $9 paid for photo processing. However sites like Snapfish were allowing pictures to be posted online free. Fisher promised early on, that Kodak's digital-photography business would be profitable by 1997. lt wasn't. ln 1997 Philippe Kahn lead the advent of cell phone camera. With the cell phone camera market growth Kodak didn't just lose out on more prints. The whole industry lost out on sales of digital cameras, because they became just a feature that was given away free on cell phones. Soon cameras became a free feature on many personal computers, too. What had been so profitable for Kodak for so long- capturing images and displaying them- was going to become essentially free.

In 1999 Fisher resigned and Carp became the new CEO. In 2000, Carp‘s first year as CEO, profit was about flat, at $l.4l billion. Carp, too, retired early, at age fifty-seven. Carp had pursued Fisher's basic strategy of "enhancing" the film business to make it last as long as possible, while trying to figure out some way to get recurring revenue from the filmless, digital world. But the temporizing didn't work any better for Carp than it had for Fisher. Kodak talked, for instance, about getting customers to digitize and upload to the Internet more of the 300 million rolls of film that Kodak processed annually, as of 2000. Instead, customers increasingly skipped the film part. ln 2002, sales of digital cameras in the United States passed those of traditional cameras-even though Kodak in the mid-I990s had projected that it would take twenty years for digital technology to eclipse film. The move to digital in the 2000s happened so fast that, in 2004, Kodak introduced a film camera that won a "camera of the year" award, yet was discontinued by the time Kodak collected the award. Kodak staked out a position as one of the major sellers of digital cameras, but being "one of" is a lot different from owning 70 percent to 80 percent of a market, as Kodak had with film, chemicals, and processing. In 2002 competition in the digital market was so intense that Kodak lost 75 percent of its stock- market value over the past decade, falling to a level about half of what it was when the reporter suggested to Carp that he might sell the company. As of 2005, Kodak employed less than a third of the number who worked for it twenty years earlier. To see what might have been, look at Kodak’s principal competitors in the film and paper markets. Agfa temporized on digital technology, then sold its film and paper business to private-equity investors in 2004. The business went into bankruptcy proceedings the following year, but that wasn't Agfa's problem. lt had cashed out at a halfway reasonable price.

As per the passage which of the following statements truly reflects the real theme of' the passage?

Solution

Throughout the passage, the author's ideas revolve around the fact that Kodak did not embrace new technology which led to its downfall.

Hence, option D is the correct answer.

Which of the following statements is not true?

I. Kodak bought sterling drug as a strategic choice for a chemical business as it was already in the business of chemically treated photo paper.

II. The chemical business was in sync with the existing business of Kodak running across the customer segment, delivery channels and the regulatory environment.

III. Kodak committed a mistake by selling sterling in pieces at a loss of 50%.

IV. Kodak’s diversification attempt with purchase of sterling to strengthen its core business and shift to digital world was a shift from its strategic focus.

Solution

From the first paragraph, we can infer that statements I and IV are true.

Hence, option B is the correct answer.

Kodak lost a big piece of its market share to its competitors because of the following best explained reasons.

I. When Carp became the CEO the digital Technology eclipsed film technology business and further Carp had been with the company for twenty nine years and had no background in technology.

II. Carp in 2004 introduced a film camera that won camera of the year award, yet it was discontinued by the time Kodak collected the award.

III. Kodak moved from traditional retail photo processing systems into digital world installing several thousands of image magic kiosks that failed to deliver real benefits to the customers.

IV. Phillipe Kahn led the advent of cell phone camera and Kodak lost out on the print business and ability to share images became a free feature with no additional charge.

Solution

"Fisher also tried to move Kodak’s traditional retail photo-processing systems into digital world and in this regard installed tens of thousands of image magic kiosks. These kiosks came just as numerous companies introduced inexpensive, high-quality photo printers that people could use at home, which, in fact, is where customers preferred to view their images and fiddle with them." - from these lines, statement III can be inferred.

"ln 1997 Philippe Kahn lead the advent of cell phone camera. With the cell phone camera market growth Kodak didn't just lose out on more prints. The whole industry lost out on sales of digital cameras, because they became just a feature that was given away free on cell phones. Soon cameras became a free feature on many personal computers, too. What had been so profitable for Kodak for so long- capturing images and displaying them- was going to become essentially free" - from these lines, statement IV can be inferred.

Hence, option D is the correct answer.

Arrange the given statements in the correct sequence as they appear in the passage.